Trend Following Strategy Based on EMA Crossover

Overview

This strategy identifies market trend direction through the crossover of fast and slow EMA lines, and trades along the trend. It goes long when the fast EMA crosses above the slow EMA, and closes position when price breaks below the fast EMA.

Strategy Logic

The strategy calculates fast EMA (i_shortTerm) and slow EMA (i_longTerm) based on input parameters. When the short term EMA crosses above the long term EMA (goLongCondition1) and price is above the short term EMA (goLongCondition2), it enters long position. When price breaks below the short term EMA (exitCondition2), it closes position.

The strategy is based on the golden cross of EMA lines to determine the major market trend, and trade along the trend. When short term EMA crosses above long term EMA, it signals an uptrend; when price is above short term EMA, it indicates the uptrend is underway, so go long. When price drops below short term EMA, it signals a trend reversal, so close position immediately.

Advantage Analysis

The main advantages of this strategy are:

-

Utilize EMA crossover to identify major market trend, avoid short-term fluctuations.

-

Adjustable sensitivity in trend detection via fast and slow EMA parameters.

-

Simple and clear logic, easy to understand and implement, suitable for quant trading beginners.

-

Customizable EMA period parameters for different products and markets.

-

Effective risk control by stop loss when price breaks EMA line.

Risk Analysis

There are also some risks:

-

Delayed EMA crossover signals may cause losses during trend reversal.

-

False breakout above short term EMA may cause failed entries.

-

Improper paramedic parameter settings may undermine strategy performance.

-

Performance relies heavily on market condition, not suitable for all products and periods.

The corresponding risk management measurements:

-

Optimize EMA parameters for better sensitivity on reversals.

-

Add other technical indicators to filter entry signals.

-

Continuously debug and optimize parameters for different markets.

-

Fully understand applicable market conditions before applying strategy.

Optimization Directions

The strategy can be further optimized in the following aspects:

-

Add other indicators like MACD and KD to filter entry signals.

-

Implement trailing stop loss to lock profit and better risk control.

-

Optimize stop loss placement with volatility indicator ATR.

-

Test and find better scientific methods for EMA parameter tuning.

-

Validate signals on multiple timeframes to improve accuracy.

-

Try BREAKOUT modifications to catch larger moves during trend acceleration stages.

Conclusion

This strategy effectively tracks market trend by trading on EMA crossover signals. With clear logic and controllable risks, it is suitable for quant trading beginners to practice on. Further optimizations on parameter tuning, entry filtering, stop loss placement can improve strategy performance. But all strategies have limitations, users should apply cautiously based on market conditions when live trading.

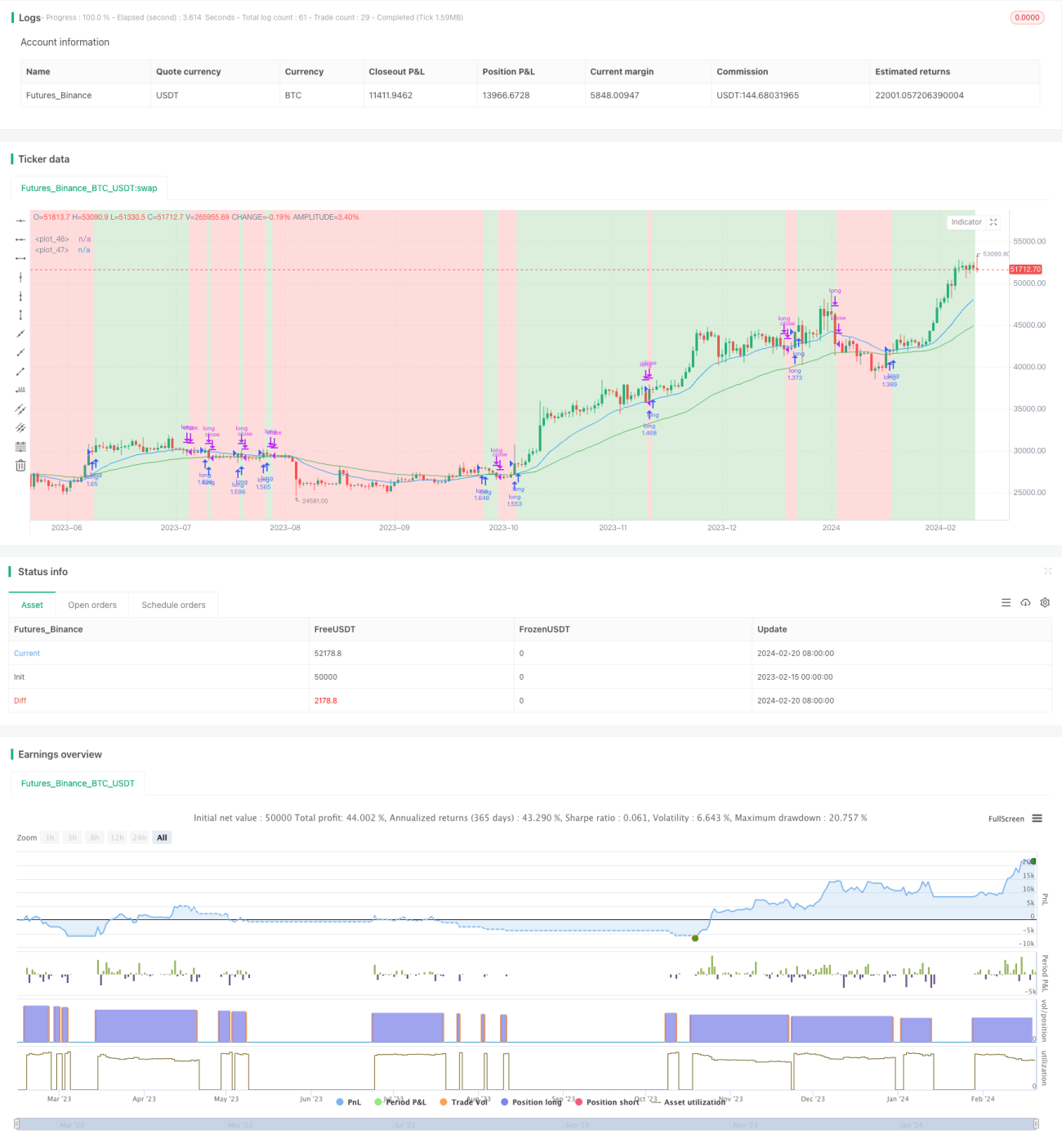

/*backtest

start: 2023-02-15 00:00:00

end: 2024-02-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © pradhan_abhishek

//@version=5- 1