Trend Tracking Strategy Based on Moving Average Crossover

Overview

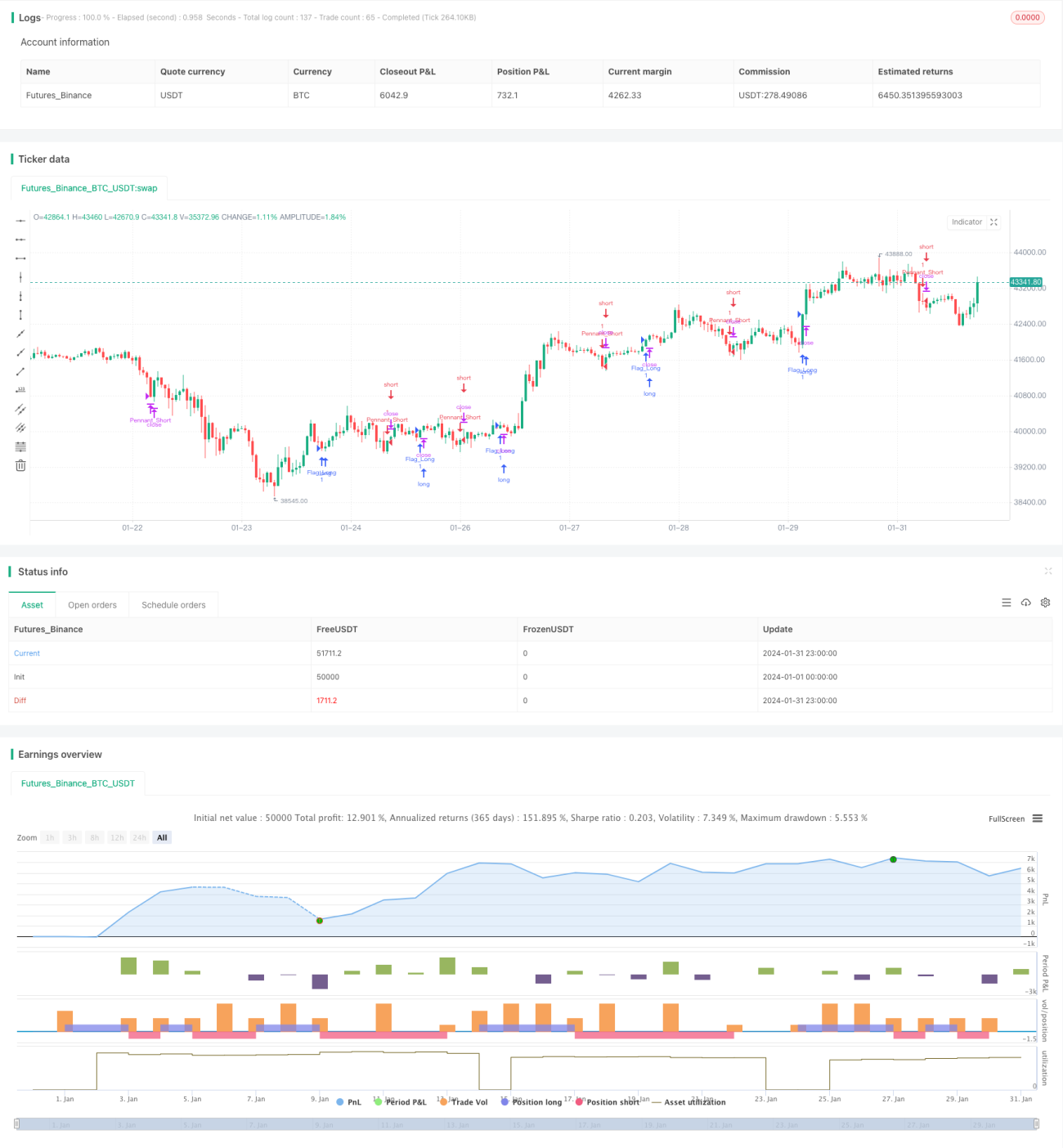

This strategy is a quantitative trading strategy that judges market trend direction based on moving average crossover and tracks the trend. It uses the crossovers of simple moving averages with different parameters to determine the entry and exit points.

Strategy Principle

The main judgment rules of this strategy are:

-

When the short-term moving average crosses above the long-term moving average from the bottom, it indicates that the market may be entering an uptrend, then go long;

-

When the short-term moving average crosses below the long-term moving average from the top, it indicates that the market may be entering a downtrend, then go short;

-

Use moving averages with different parameters to judge trends at different timescales and track trends at different levels.

Specifically, the strategy uses 5 moving averages - 20-day, 30-day, 50-day, 60-day and 200-day. When 20-day MA crosses above 50-day MA, it is a buy signal; When 10-day MA crosses below 30-day MA, it is a sell signal. Using MAs of different parameters can tell trends in both longer and shorter timescales.

Advantages

This trend tracking strategy based on MA crossover has the following advantages:

- Simple to understand and implement;

- Can effectively determine market trend direction and strength;

- Different parameter settings allow tracking trends at different timescales;

- Highly customizable based on needs by adjusting MA parameters.

Risks

There are also some risks with this strategy:

- MAs have lagging nature, which may cause certain delays;

- Wrong MA parameter settings may lead to excessive trading signals and unnecessary losses;

- Avoid using this strategy during market consolidation, use it only during obvious trending markets.

To reduce risks, we can adjust MA parameters, optimize parameter settings, and use other indicators to aid decision making.

Improvement Areas

We can optimize this strategy in the following areas:

- Optimize MA parameters to find the optimal parameter combination, reduce trading frequency while improving profit rate;

- Incorporate other technical indicators like RSI, KD to improve decision accuracy;

- Add stop loss strategies to control risks effectively;

- Combine complex machine learning models for parameter optimization and strategy evaluation, continuously iterate and upgrade.

Conclusion

This is a very basic trend tracking strategy. It uses MA crossover principle to determine market trend direction, simple and effective, easy to understand and implement. We can make lots of expansions and optimizations to make it suitable for more complex quantitative trading. Overall this is a great strategy framework to build upon.

- 1