Bull Flag Breakout Strategy

Overview

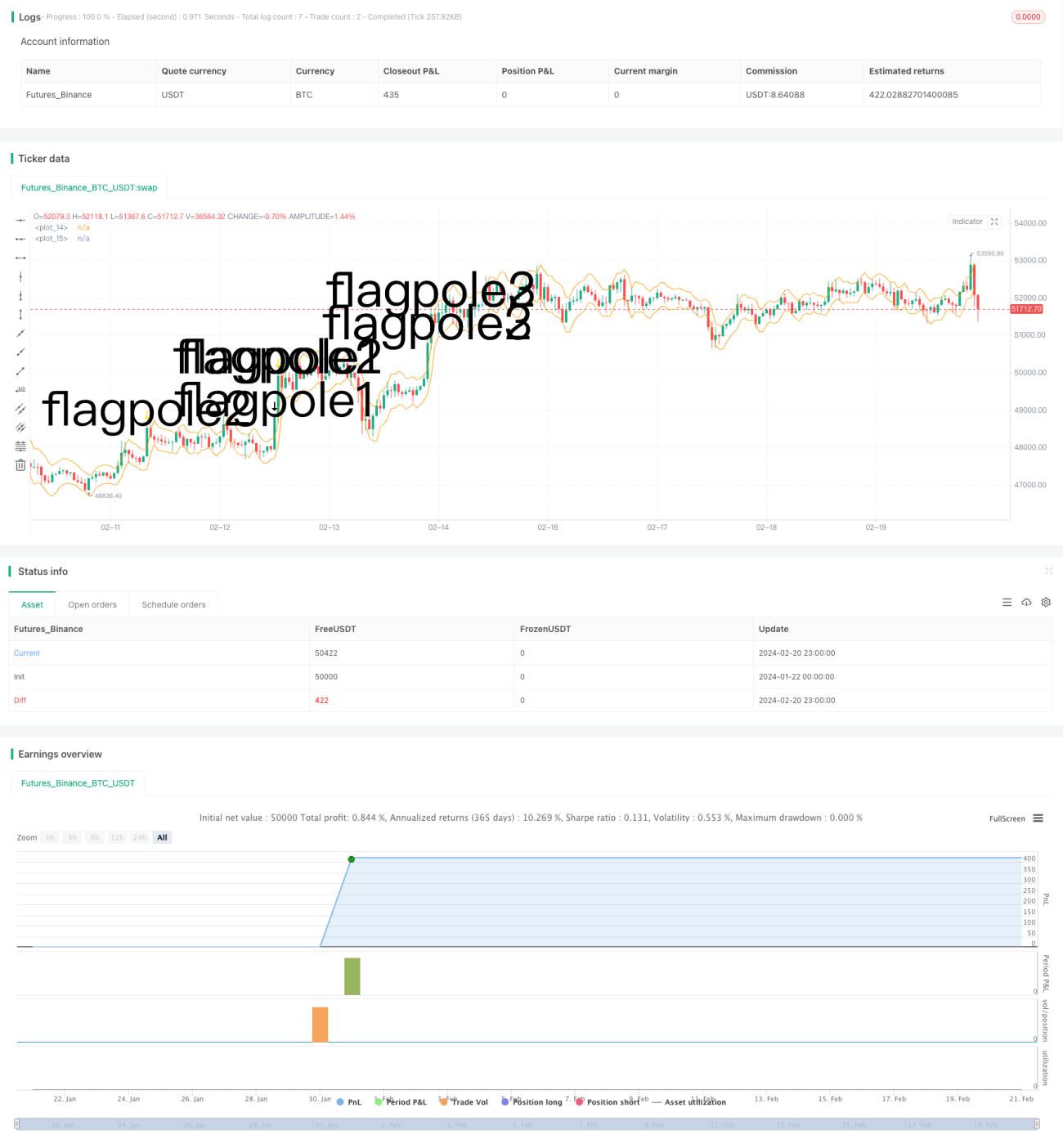

The bull flag breakout strategy is a technical analysis strategy that identifies bull flag chart patterns and enters at the breakout point, aiming to capture the start of a trend. The strategy uses the Average True Range (ATR) indicator to assist in determining the flag range after a clear flagpole, filtering entry opportunities.

Strategy Logic

The main steps of this strategy are:

- Determine the flagpole: Requires new high in price and breakout of ATR channel.

- Determine pole height: Measure distance between pole top and previous SMA.

- Determine flag range: Flag bottom is 33% of pole height as minimum range.

- Identify flag pattern: Judge if last 3 bars all within flag range.

- Entry: Go long when flag pattern emerges.

- Exit: Close position after fixed 6 bars.

When judging the flagpole and flag, the strategy cleverly uses the ATR indicator to determine significant breakouts and strictly limits the flag height within 33% of the pole height to avoid excessive false signals. In addition, requiring 3 consecutive bars to form the flag improves reliability. Overall, the strategy rules are rigorously designed and has some advantage in capturing early trend breakouts.

Advantage Analysis

The main advantages of this strategy include:

- Using flag patterns to determine trend starts is a classic technical analysis method with high success rate.

- ATR and strict range limitations avoid lots of false signals and improve entry accuracy.

- Fixed 6 bar exit locks in some profits and avoids reversal risks.

- Clear rules easy to implement, grasp and follow.

- Can find opportunities in various market conditions, flexible.

Risk Analysis

The major risks of this strategy are:

- Flags cannot fully determine trends, failures still exist.

- 6 bar exit may be premature and exit too early.

- Choppy markets can produce false flags easily.

- Unable to effectively control single loss amount.

To address the above risks, we can set stop losses, optimize exit mechanisms to lock profits when reaching certain profit ratio. We can also filter with other indicators to avoid false signals in choppy markets.

Optimization Directions

Some directions to optimize the strategy:

- Combine indicators like MACD, KD to avoid false signals in choppy markets.

- Parameterize ATR multiplier, exit period based on market regime to improve adaptivity.

- Set trailing stop loss or consider profit drawdown ratio for dynamic exits.

- Try machine learning approaches to find better features determining flag height.

- Evaluate actual win rate and profit ratio, dynamically adjust position sizing.

Conclusion

In conclusion, the bull flag breakout strategy utilizes technical pattern to determine trend starts, a rather classical method, and the entry rules are indeed rigorously designed to filter out many false signals. But there is room for improving risk control and exits holistically so that the strategy can operate steadily across different markets after sufficient verification and optimization. It can become a valuable component in a quantitative trading system.

/*backtest

start: 2024-01-22 00:00:00

end: 2024-02-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © smith26

//This strategy enters on a bull flag and closes position 6 bars later. Average true range is used instead of a moving average.

//The reason for ATR instead of MA is because with volatile securities, the flagpole must stand up a noticable "distance" above the trading range---which you can't determine with a MA alone.

//This is broken up into multiple parts: Defining a flagpole, defining the pole height, and defining the flag, which will be constrained to the top third (33%) of the pole height to be considered a flag.- 1