The Dual Reversal Strategy

Overview

The dual reversal strategy is a quantitative strategy that combines the 123 reversal and three-bar reversal pattern to improve signal quality and reduce risk. It adopts a trading approach using a combination of price differential indicators and candlestick pattern indicators, opening positions only when both indicate a signal, thereby increasing signal accuracy.

Strategy Principle

The dual reversal strategy brings together two different types of trading strategies. First is the 123 reversal strategy, which employs price differential indicators and triggers when prices reverse over two consecutive days and stochastic indicators cross threshold values. The second is the three-bar reversal pattern strategy, which looks at a three-day candlestick chart and triggers when the middle day posts the lowest low and the last day closes above the prior day's high. The strategy enters a long or short position when both strategies concurrently issue a signal in the same direction.

Specifically, the 123 reversal strategy uses a 9-day stochastic oscillator to identify overbought and oversold conditions. It generates a buy signal when prices fall for two straight days and the stochastic readings dip below 50, and a sell signal when prices rise for two straight days and stochastic tops 50. The three-bar reversal pattern strategy detects if prices have formed a high-low-high pattern over three days, indicating a short-term oversold reversed by momentum.

The dual reversal strategy requires concordant signals from both strategies before taking any positions. This greatly reduces false signals, ensuring the system only trades at high-probability opportunities.

Advantage Analysis

Compared to single-strategy systems, the dual reversal strategy has the following advantages:

- Improved signal quality, fewer false signals

- Dual indicator confirmation, lower drawdown risk

- Captures both short-term and medium-term reversal opportunities

- Simple to understand and implement

Risks and Solutions

The main risk of the dual reversal strategy is missing some profitable opportunities. Due to its strict signal requirements, some trading opportunities identified by individual indicators will be skipped. This can be mitigated by adjusting parameters to relax the conditions of one indicator and increase trade frequency.

Another risk is both indicators concurrently failing in extreme market conditions, yielding a higher rate of false signals. For such cases, stop-loss mechanisms can be added to quickly unwind positions and limit losses. Alternatively, disable trade signals during historically proven unfavorable extreme market conditions to avoid taking positions.

Optimization Suggestions

Further optimizations for the dual reversal strategy include:

- Adjust stochastic indicator parameters to improve overbought/oversold assessment accuracy

- Test effectiveness across different trading instruments to find best asset fit

- Incorporate machine learning models to aid signal validation and improve accuracy

- Combine more market statistics like volume changes, intraday volatility to determine optimal entry timing.

Conclusion

The dual reversal strategy successfully combines mean-reversion principles with candlestick pattern analysis, fully capturing the cyclicality in prices. Compared to simple trend-following methods, it strikes a balance between risk and reward. With continual enhancements, the strategy's value will be validated over time.

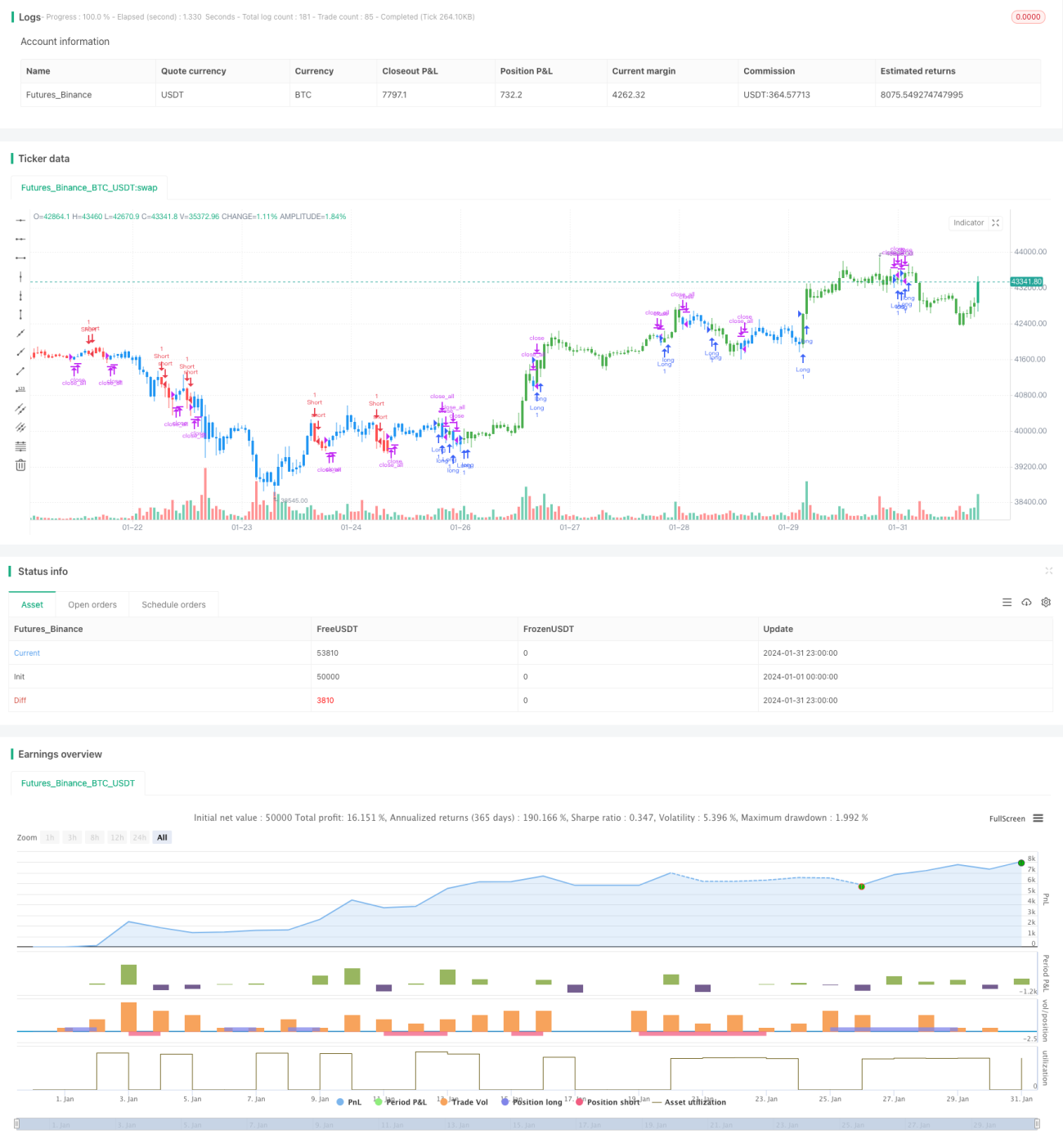

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 17/04/2019

// This is combo strategies for get - 1