Multi-Timeframe Trend Trading Strategy Based on Compressed Indicators

Overview

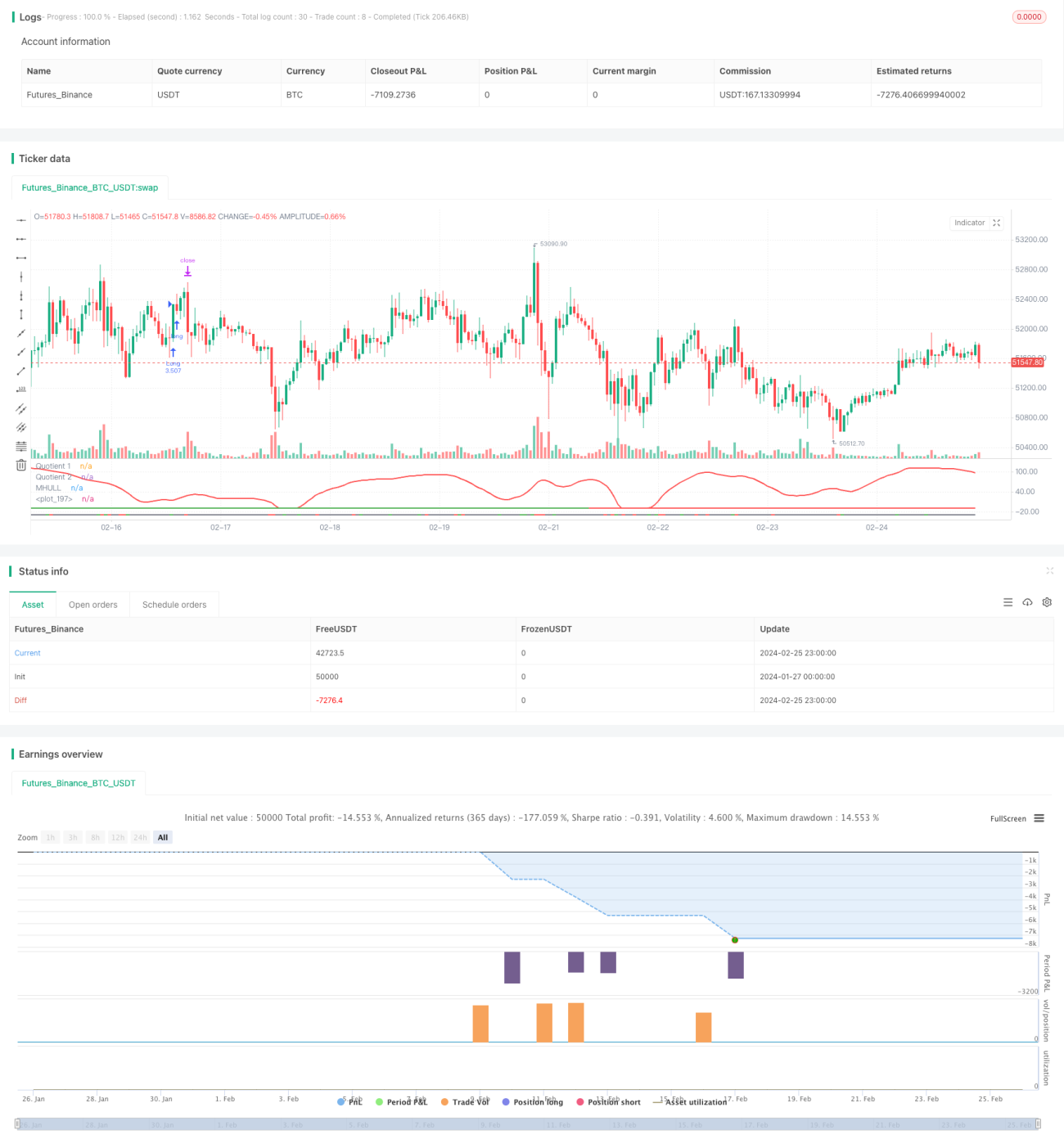

This strategy combines the Boom Hunter, Hull Suite, and Volatility Oscillator indicators to implement a quantitative strategy for trend tracking and breakout trading across multiple timeframes. It is suitable for digital assets with high volatility and abrupt price moves like Bitcoin.

Principles

The core logic of this strategy is based on the following three indicators:

-

Boom Hunter: An oscillator that uses indicator compression techniques to generate trading signals from crossovers between two quotients (Quotient1 and Quotient2).

-

Hull Suite: A set of smoothed moving average lines that determine trend direction based on the relationship between the midline and upper/lower bands.

-

Volatility Oscillator: An oscillator indicator that quantifies price volatility.

The entry logic of this strategy is when the two Quotient indicators of the Boom Hunter cross up or down, the price breaks through the Hull midline and diverges from the upper or lower band, meanwhile the Volatility Oscillator is in overbought/oversold area. This filters out some false breakout signals and improves entry accuracy.

The stop loss is set by finding the lowest valley or highest peak over a certain period (default 20 bars), and take profit is obtained by multiplying the stop loss percentage by a configured profit factor (default 3x). Position sizing is calculated based on a percentage of total account equity (default 3%) and the specific stop loss range of the instrument.

Pros

- Extracts key trading signals from price using indicator compression techniques, improving profitability

- Combination of multiple indicators prevents false breakouts and accurately determines trend direction

- Dynamic stop loss and take profit setting allows risk-controlled trend following

- Ensures trading in high volatility environments using the Volatility Oscillator

- Enhanced strategy stability through multi-timeframe analysis

Risks

- Boom Hunter indicators can have compression distortions, generating incorrect signals

- Hull midline may lag and unable to track price changes in real time

- Missing trading opportunities or forced liquidations during volatility contraction

Solutions:

- Adjust compression indicator parameters to balance sensitivity

- Try exponential moving averages instead of the midline

- Add other judgment indicators to avoid volatility misdirection

Optimization

This strategy can be optimized in the following aspects:

-

Parameter Optimization: Obtain best parameter combinations by tweaking indicator settings like period and compression coefficient

-

Timeframe Optimization: Test different periods (1min, 5min, 30min etc.) to find the optimal trading timeframe

-

Position Sizing Optimization: Change per trade position size and ratio to find the ideal capital utilization plan

-

Stop Loss Optimization: Adjust stop loss placement based on different trading instruments to achieve optimal risk-reward ratio

-

Condition Optimization: Add/reduce indicator filters to obtain more accurate entry signals

Conclusion

This strategy combines Boom Hunter, Hull Suite and Volatility Oscillator to implement multi-timeframe trend tracking trading, effectively identifying abrupt price behaviors suitable for highly volatile digital assets. With controllable risks, strong practicality and extensibility through parameter tuning, filter conditions and stop loss optimization, it is an exemplary quantitative model.

- 1