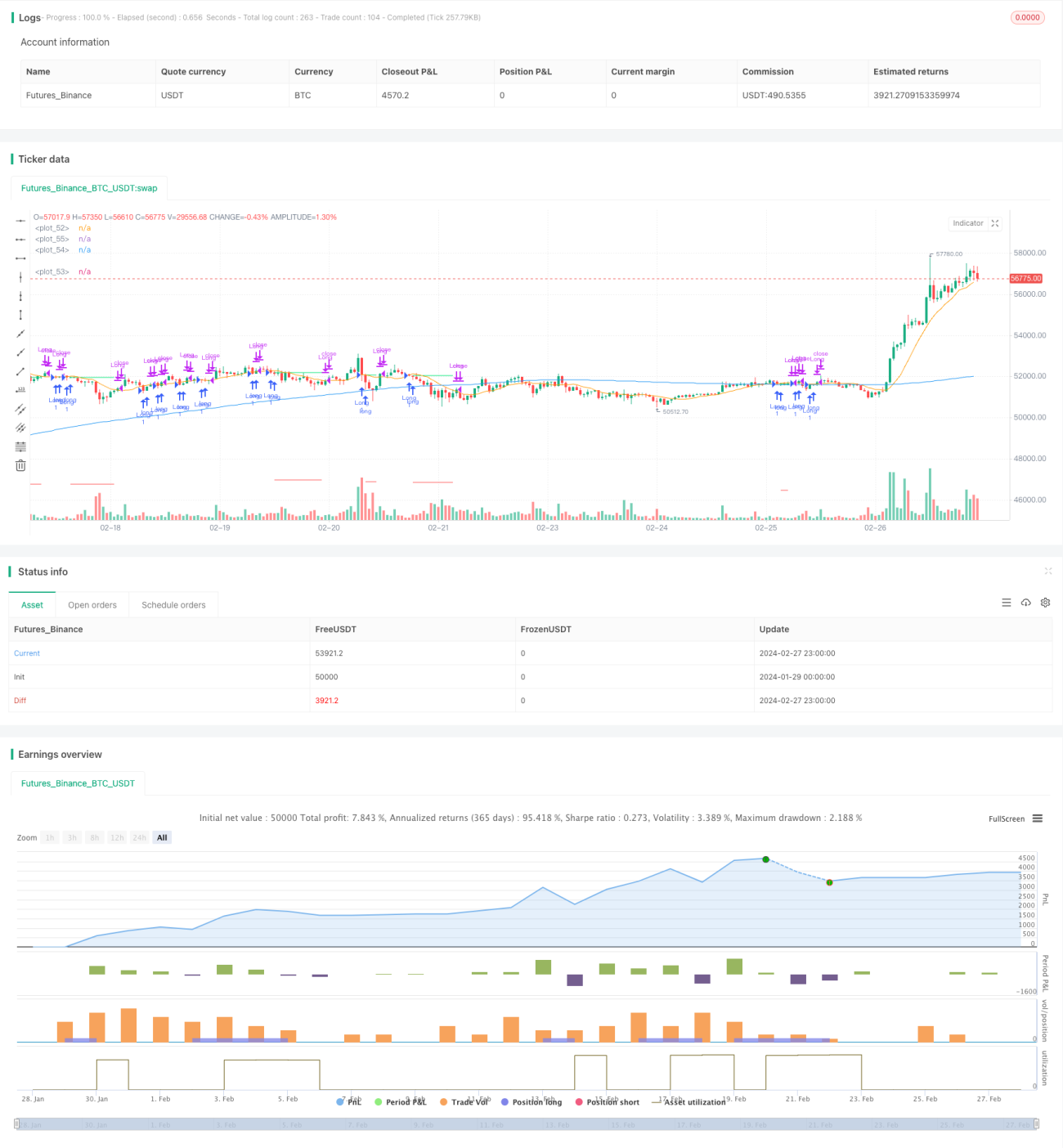

概述

该策略采用多时间框架均线的方法,利用长期均线判断大趋势方向,短期均线判断短期趋势方向,在长线和短线确认趋势一致时,进场做多/空;当短线回调到长线附近时,判断形成短期调整进入机会,此时做反向操作。该策略主要适用于中长线趋势性股票。

策略原理

该策略使用200日简单移动均线判断长期趋势方向,使用10日简单移动均线判断短期趋势方向。当股价高于200日均线且低于10日均线时,说明目前处于长线上升和短线回调阶段,此时做多;当股价低于200日均线且高于10日均线时,说明目前处于长线下降和短线反弹阶段,此时做空。

具体来说,当满足如下条件时,做多入场:收盘价>200日均线 且 收盘价<10日均线;当满足如下条件时,做空入场:收盘价<200日均线 且 收盘价>10日均线。

入场后设置止损机制,如果从买入价回撤超过10%,则止损出场。同时,如果设置了i_lowerClose选项,则会等待较低的收盘价出现后再出场,这可以避免止损过于敏感。

优势分析

该策略结合多时间框架均线,可以在较大概率上捕捉中长线趋势的方向。当短期均线回调到长期均线时,utsch策略提供较好的入场时机。与单一均线系统相比,可以减少因短期调整而被套的概率。

该策略风险可控。设置了10%的止损比例以控制亏损;同时设置了时间过滤条件,可以避免在特定时间段交易。

风险分析

该策略依然存在被套的风险。当短线调整的时间过长或调整幅度过大时,可能触发止损而被套出场。这时就面临亏损的风险。

该策略对交易品种的适配性较差。对于波动性大,调整时间长的股票,该策略容易被止损出场,效果不佳。

在市场整体发生重大调整时,该策略也会面临较大亏损。例如金融危机期间,该策略可能难以获利。

优化方向

可以引入更多均线系统,形成多重筛选机制。例如加入50日均线,只有当收盘价处于50日均线与200日均线之间时才考虑入场。这可以进一步筛选出趋势性较好的品种。

可以设置浮动止损。具体来说,入场后,可以根据股票的波动范围,设置可变化的止损幅度,而不是固定的10%止损。这可以减少不必要的止损被触发的概率。

可以结合其他指标判断市场状况。例如MACD,在MACD显示市场脱离时,可以暂停该策略,避免亏损。这可以根据大市场判断来控制策略的启动与关闭。

总结

该策略整体来说是一种典型的多时间框架均线策略。它结合长短期均线,在大概率捕捉中长线趋势的同时,抓住短线回调机会入场。策略风险也在可控范围内。通过引入更多指标、优化止损方式等,可以进一步增强该策略的稳定性。

- 1