Momentum Average Directional Movement Index Moving Average Crossover Strategy

Overview

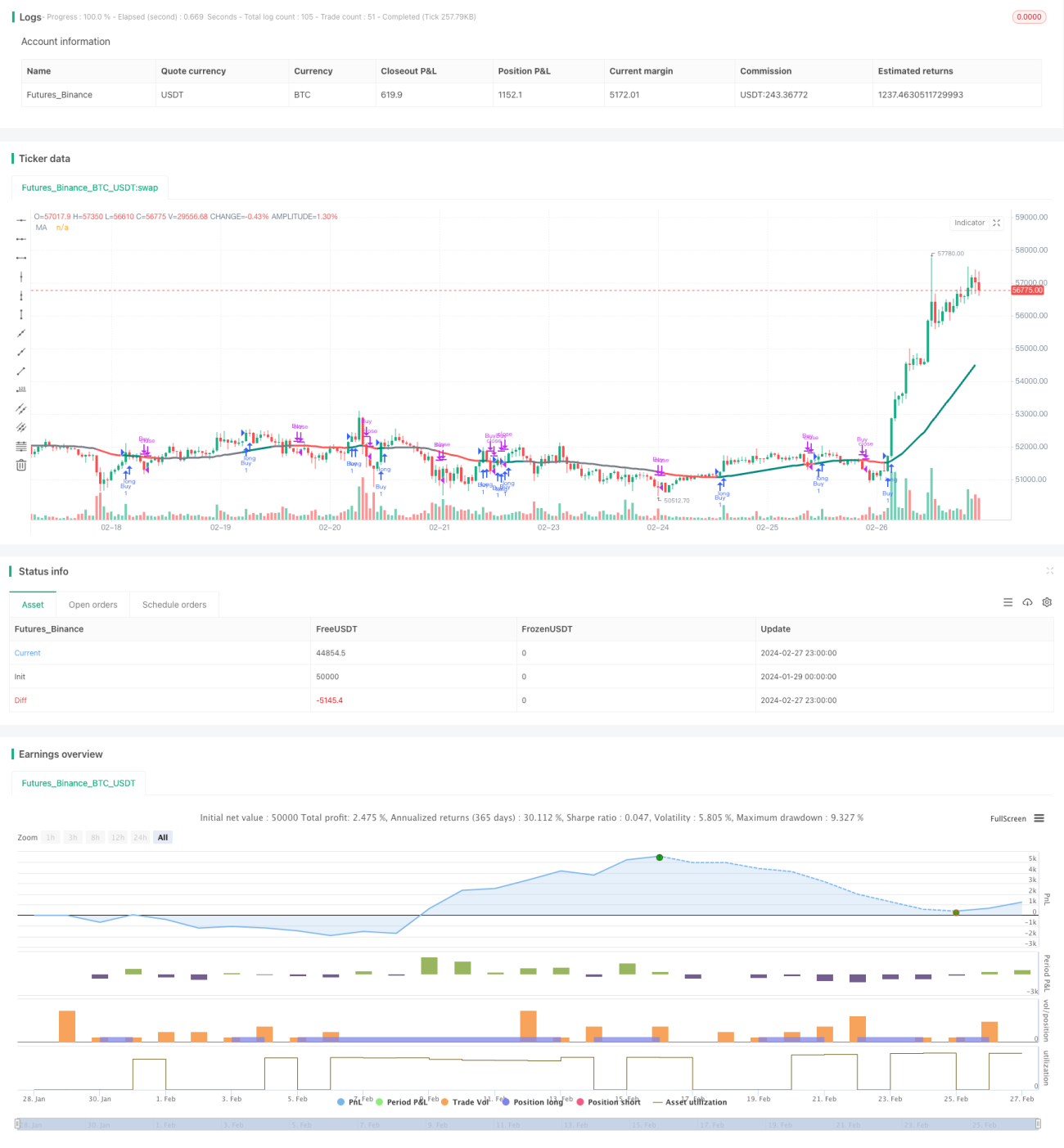

The Momentum Average Directional Movement Index Moving Average Crossover Strategy combines two powerful technical indicators, Moving Average (MA) and Average Directional Index (ADX), to provide traders with enhanced technical precision. Designed for dynamic market analysis, this strategy offers clear trading signals.

Strategy Logic

The strategy calculates a Weighted Moving Average (WMA) to track price momentum and smooth out price fluctuations to generate trend signals. At the same time, it calculates the Average Directional Index (ADX) and positive/negative directional movement indices (+/-DI) to determine the existence and strength of a trend. When ADX is above a specified parameter, a trend is considered to exist. When the positive directional movement index is higher than the negative directional movement index, it is a bullish signal.

The strategy uses the crossover of MA and ADX indicators as the basis for trading decisions. When ADX is above the threshold and DIdiff (DI+ - DI-) is greater than 0, it goes long. When ADX is above the threshold and DIdiff is less than 0, it exits positions.

Advantage Analysis

Combining the advantages of moving average and ADX index, this strategy can effectively identify the existence and direction of trends and reduce false signals. Compared to a single indicator, this combined indicator can provide more reliable trading signals.

In addition, this strategy is a fully quantitative strategy based on parameter calculations with good backtesting results and stable live performance, making it suitable for algorithmic trading.

Risk Analysis

This strategy is prone to trading risks during significant market fluctuations. When prices move violently and the indicators do not react, it can bring losses to the account. In addition, improper parameter settings can also affect strategy performance.

Losses can be controlled by stop loss. At the same time parameters can be optimized and combined with other indicators for filtering to reduce false signals.

Optimization Directions

The following aspects of this strategy can be optimized:

-

Combine with other indicators for filtering, such as Bollinger Bands, RSI etc. to improve signal quality

-

Optimize the length parameters of the moving average and ADX to find the optimal parameter combination

-

Add stop loss mechanisms to control single loss

-

Test different holding periods to find the optimal holding cycle

Conclusion

The Momentum Average Directional Movement Index Moving Average Crossover Strategy can effectively identify market trend directions by calculating price momentum and trend strength. It is a reliable trend tracking strategy. This strategy has high algorithmic degree, stable backtesting, and good live performance. Further optimization may lead to better strategy efficiency.

- 1