Multiple Exponential Moving Average Trading Strategy

Overview

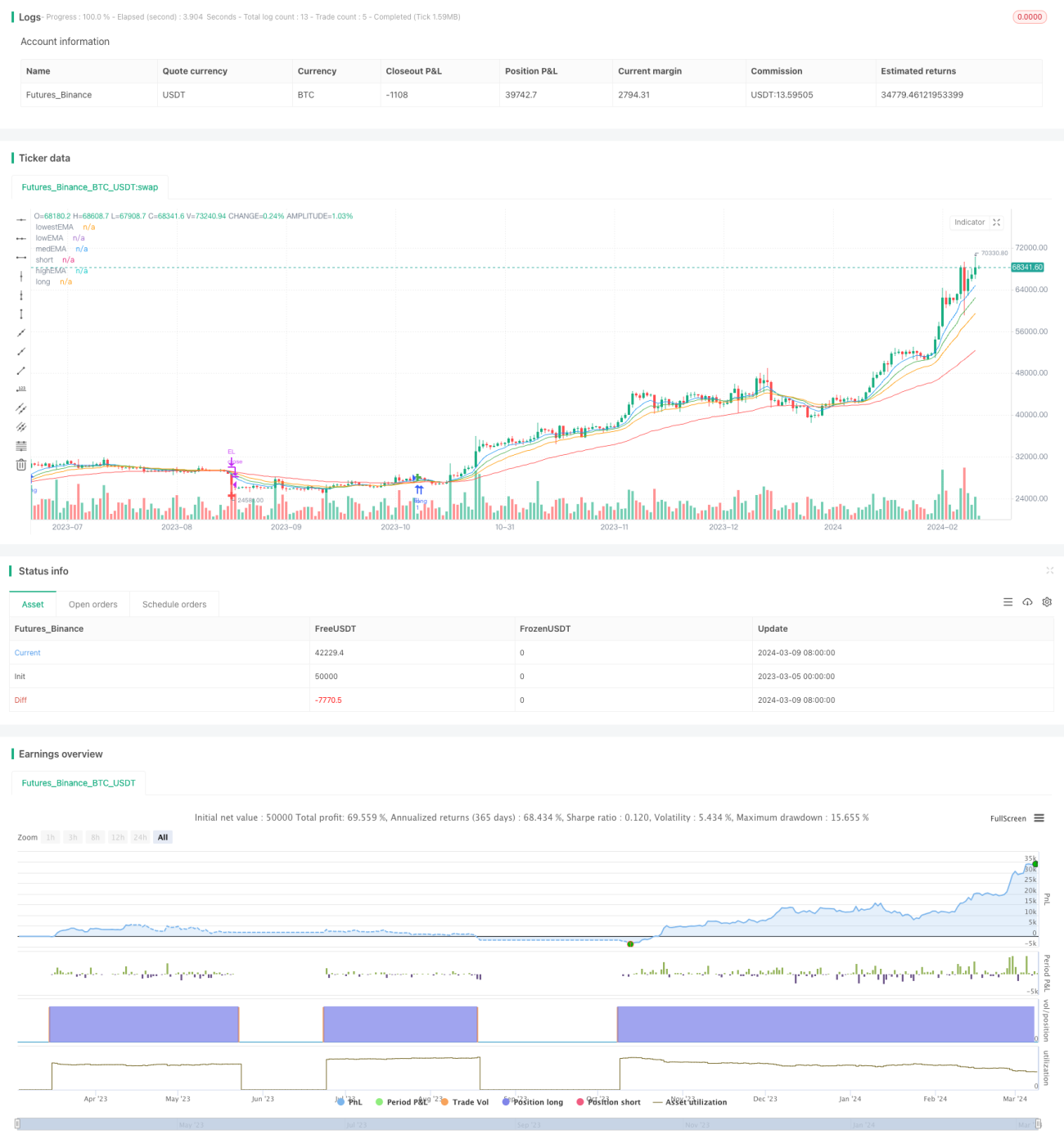

This strategy combines multiple Exponential Moving Averages (EMAs) to identify potential entry and exit points in the market. By comparing the trends of EMAs with different periods, it determines the current market trend and enters trades at the beginning of the trend formation and closes positions at the beginning of the trend's end.

Strategy Principle

This strategy uses 4 EMAs with different periods as core indicators, namely ultra-short-term EMA (default 8 periods), short-term EMA (default 13 periods), medium-term EMA (default 21 periods), and long-term EMA (default 55 periods). When the long-term EMA is below the other three EMAs, it is judged that the current market may be at the beginning of an upward trend, and the strategy opens a long position; when the long-term EMA is above the other three EMAs, it is judged that the current market may be at the beginning of a downward trend, and the strategy closes all long positions. The strategy identifies trend turning points by this combination of long and short EMA arrangements to capture nascent trends.

Compared to Simple Moving Average (SMA), EMA places more emphasis on recent prices and thus its trend is more sensitive and can react to price changes more quickly. The crossover of EMAs with different periods reflects the strength of trends on different time scales. The long-term EMA is the most stable and represents the significant market trend; the medium and short-term EMAs are relatively sensitive and reflect the short and medium-term market trends. They together constitute the core logic of this strategy.

Advantage Analysis

-

Wide applicability: This strategy is based on the EMA indicator of the price itself and is applicable to most varieties with good liquidity and relatively smooth trends, such as various futures, forex, mainstream cryptocurrencies, etc.

-

Trend tracking: By comparing the position relationship of EMAs with different periods to determine the trend, it can capture the beginning of trend formation to a certain extent and track the trend.

-

Flexible parameters: The period parameters of EMA can be flexibly adjusted according to the characteristics of varieties, investment horizon, etc., and have certain adaptability.

-

Clear logic: The strategy generates trading signals based on a simple combination of long and short EMA arrangements, and the logic is clear and easy to understand and implement.

Risk Analysis

-

EMA lag: EMA is essentially a trend-tracking indicator and has a certain lag, which may generate more false signals in a turbulent market.

-

Parameter sensitivity: The selection of EMA period parameters has a significant impact on the strategy performance, and the parameters optimized may not maintain good performance on out-of-sample data.

-

Lack of filtering: This strategy lacks further filtering of trading signals, and all generated signals will be traded, which may result in some low-quality trades.

-

Fixed position: Currently, the strategy opens a fixed 1 unit position each time, lacking dynamic position control based on risk, and risk management is not perfect enough.

Optimization Direction

-

Introduce trend filtering: On the basis of EMA signals, add trend strength filtering indicators such as ATR and ADX to filter out signals from weak trends and turbulent periods.

-

Introduce volatility filtering: On the basis of trend filtering, volatility filtering such as Bollinger Band width can be further introduced to filter out low-quality signals that may be caused by high volatility.

-

Optimize stop-loss: Currently, the strategy lacks a clear stop-loss logic. After introducing trend and volatility filtering, dynamic stop-loss based on ATR or percentage can be added to control the maximum loss of a single trade.

-

Dynamic position: Based on the volatility of varieties, the proportion of account value, etc., the number of positions opened by the strategy each time can be dynamically controlled to pursue higher absolute returns while reducing risk.

-

Optimize parameters: For different varieties and different periods, the optimal parameters of EMA may be different, and parameter optimization needs to be performed separately according to the characteristics of varieties to improve the applicability of the strategy.

Summary

This strategy identifies trend turning points by comparing the long and short arrangement combinations of 4 EMAs with different periods to capture the beginning of trend formation. The idea is simple and clear. Its advantages lie in its wide range of applicability, clear logic, and flexible parameters, and it can track trends well; but at the same time, it also has the inherent lag of EMA indicators, as well as problems such as parameter sensitivity, lack of filtering, and fixed position. In the future, the robustness and profitability of this strategy can be improved from aspects such as introducing trend and volatility filtering, optimizing stop-loss, dynamic position, and parameter optimization to make it more complete and reliable.

- 1