1

关注

1802

关注者

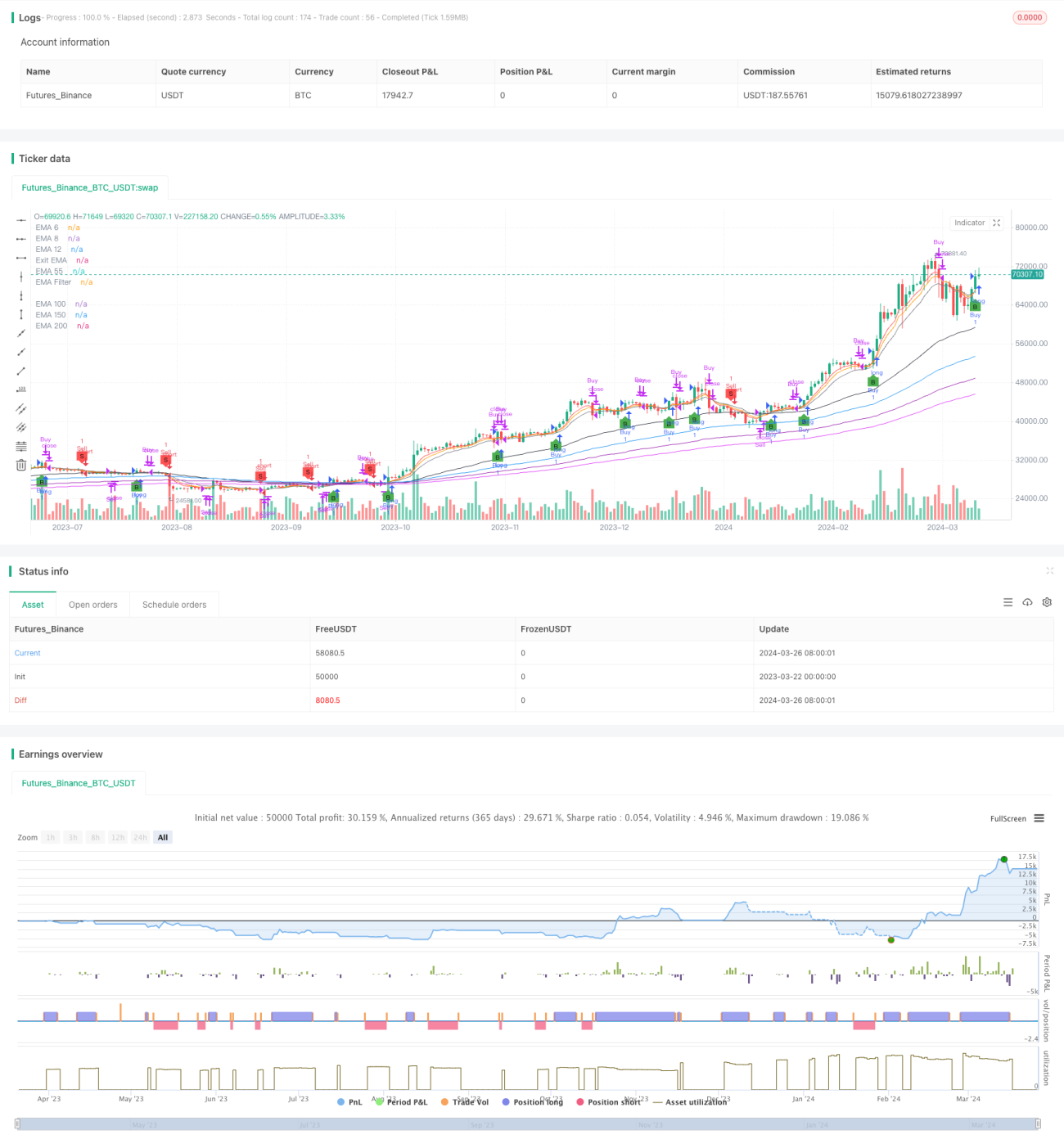

策略概述

该策略结合了多个指数移动平均线(EMA)、相对强弱指数(RSI)以及基于标准差的出场条件来识别潜在的买卖机会。使用了短期(6、8、12天)、中期(55天)和长期(150、200、250天)的 EMA 来分析市场趋势的方向和强度。RSI 采用可配置的买入(30)和卖出(70)阈值来评估动量并识别超买或超卖状况。该策略还采用了一个独特的出场机制,当收盘价触及 12 日 EMA 的可配置标准差范围(默认为0.5)时触发出场,从而提供了一种潜在的保护利润或降低损失的方法。

策略原理

- 计算多个周期的 EMA(6、8、12、55、100、150、200)作为视觉参考,以评估市场趋势。

- 根据用户输入的蜡烛线数量(3-4根),计算最近 N 根蜡烛线的最高价和最低价。

- 买入条件:当前收盘价高于最近 N 根蜡烛线的最高价,且高于 EMA 过滤器(如果启用)。

- 卖出条件:当前收盘价低于最近 N 根蜡烛线的最低价,且低于 EMA 过滤器(如果启用)。

- 长仓出场条件:当前收盘价低于 12 日 EMA + 0.5 倍标准差,或低于 12 日 EMA。

- 短仓出场条件:当前收盘价高于 12 日 EMA - 0.5 倍标准差,或高于 12 日 EMA。

- 使用 RSI 作为辅助指标,默认周期为14,超卖阈值为30,超买阈值为70。

策略优势

- 结合了趋势跟踪(多重 EMA)和动量(RSI)两个维度,提供了更全面的市场分析视角。

- 独特的基于标准差的出场机制,可在保护利润和控制风险之间取得平衡。

- 代码模块化程度高,关键参数可由用户配置,灵活性强。

- 适用于多个品种和时间周期,特别是日线的股票和比特币交易。

风险分析

- 在震荡市或趋势反转初期,频繁出现虚假信号,导致连续亏损。

- 默认参数并非对所有市场环境都有效,需结合回测对参数进行优化。

- 单纯依赖本策略进行交易风险较大,建议结合其他指标、支撑阻力位等辅助决策。

- 对突发重大事件引发的趋势反转响应较慢。

优化方向

- 对 EMA 和 RSI 参数进行优化:根据品种、周期和市场特点,对各项参数组合进行穷举,寻找最佳参数区间。

- 加入止损止盈机制:参考 ATR 等波动率指标,设置合理的止损和止盈位,控制单笔交易风险。

- 引入仓位管理:可根据趋势强度(如 ADX)或距离关键支撑阻力位远近,调节仓位大小。

- 与其他技术指标组合使用:如布林带、MACD、均线交叉等,提高开平仓信号可靠性。

- 分市场状态优化:对趋势、震荡、转折等不同市场状态分别优化参数组合。

总结

本文提出了一个基于多重移动平均线、RSI 和标准差出场的蜡烛线高度突破交易策略。该策略从趋势和动量两个维度对市场进行分析,同时采用了独特的标准差出场机制,在捕捉趋势机会的同时兼顾风险控制。策略思路清晰,逻辑严谨,代码实现简洁高效。经过合理优化,该策略有望成为一个稳健的日内中高频交易策略。但需注意,任何策略都有其局限性,盲目使用可能带来风险。量化交易不应是机械的"信号-下单"过程,而应建立在对整体市场态势的把握和审慎的风险管理之上。交易者还需不断评估策略表现,适时调整,并与自己的交易风格和承受能力相结合,才能长期立于不败之地。

策略源码

Pine

/*backtest

start: 2023-03-22 00:00:00

end: 2024-03-27 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Candle Height Breakout with Configurable Exit and Signal Control", shorttitle="CHB Single Signal", overlay=true)

// Input parameters for EMA filter and its length策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1