Triple Exponential Moving Average Convergence Divergence and Relative Strength Index Combined 1-Minute Chart Cryptocurrency Quantitative Trading Strategy

Overview

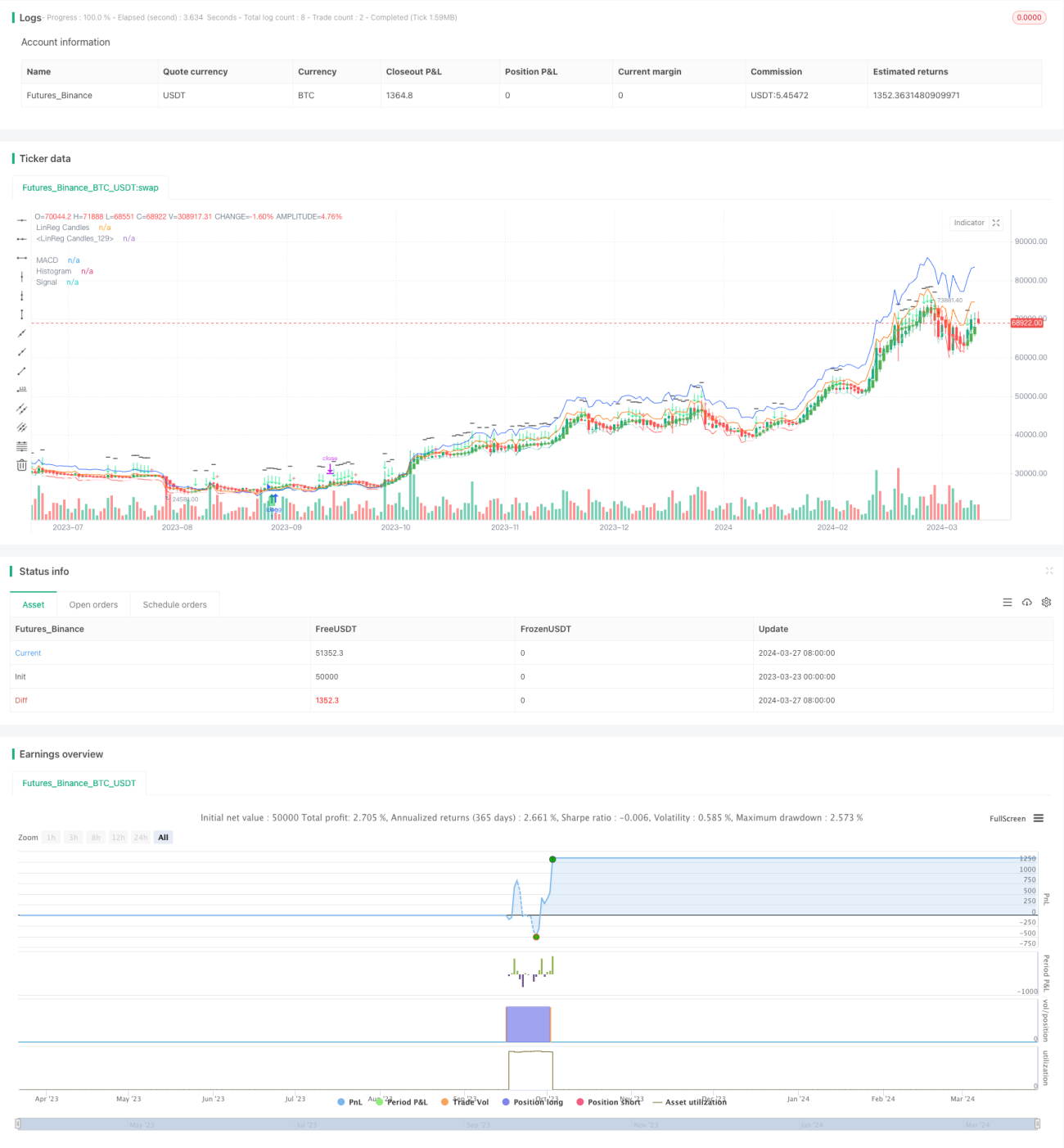

This strategy combines the Triple Exponential Moving Average Convergence Divergence (Triple MACD) and Relative Strength Index (RSI) methods, specifically designed for quantitative trading in the cryptocurrency market on a 1-minute time frame. The main idea behind the strategy is to capture changes in bullish and bearish momentum using MACD indicators with different period parameters, while employing the RSI indicator to confirm trend strength. By averaging the three MACD signals, noise can be effectively smoothed out, improving the reliability of trading signals. Additionally, the strategy utilizes linear regression techniques to identify consolidation phases in the market, avoiding frequent trades during choppy price action. The entire strategy is suitable for grid trading bots, capable of generating steady returns amidst the rapid fluctuations of the cryptocurrency market.

Strategy Principles

The strategy employs three MACD indicators with different parameters: fast line periods of 5/13/34 and slow line periods of 8/21/144. It calculates the difference between them to obtain the MACD values. These three MACD values are then averaged, and the final MACD histogram is derived by subtracting the Signal value (N-period EMA of MACD) from the averaged MACD. Simultaneously, a 14-period RSI indicator is calculated to assist in determining trend strength. A long signal is generated when the average MACD histogram shifts from negative to positive, RSI is below 55, and there is a bullish alignment. Conversely, a close signal is triggered when the average MACD histogram changes from positive to negative, RSI is above 45, and there is a bearish alignment. Furthermore, the strategy applies an 11-period linear regression to fit the candlesticks, identifying ranging markets by analyzing the ratio between the length of the candlestick bodies and shadows.

Advantage Analysis

- The combination of multiple-period MACD indicators objectively reflects trend changes in the market at different time scales, enhancing the accuracy of trend identification.

- Integrating MACD with the RSI indicator forms strict entry and exit conditions, contributing to improved strategy profitability and drawdown control.

- Averaging MACD signals effectively eliminates false signals caused by frequent indicator oscillations, making trading signals more reliable.

- Utilizing linear regression to determine ranging markets helps avoid entering trades during oscillating markets when the trend is unclear, reducing losing trades.

- In the rapidly changing cryptocurrency market, a 1-minute level quantitative trading strategy is better positioned to capture trading opportunities arising from market fluctuations in a timely manner.

Risk Analysis

- The strategy performs better in unidirectional trend markets. If the market remains in a wide-ranging oscillation state for an extended period, trading signals may frequently become invalid.

- Due to the high volatility of the cryptocurrency market, extreme abnormal fluctuations in the short term may lead to significant drawdowns.

- The selection of strategy parameters has a clear impact on overall profitability. Improper parameter settings may cause the strategy to fail. Therefore, sufficient parameter optimization and backtesting verification for different trading instruments are necessary before live trading.

Optimization Directions

- Consider introducing indicators related to price volatility, such as ATR, to filter entry signals and reduce potential losses caused by abnormal market fluctuations.

- In addition to linear regression, other methods such as support and resistance levels, Bollinger Bands channels, etc., can be explored to further improve the accuracy of identifying ranging markets.

- In trend markets, introduce trailing stop-loss to optimize exit points, maximizing the profit of each trade.

- Considering the characteristic differences among various trading instruments, set different strategy parameters for different instruments to enhance the adaptability and stability of the overall strategy.

Summary

This strategy cleverly combines the Triple MACD with the RSI indicator and utilizes linear regression techniques to identify ranging markets, forming a complete set of high-frequency quantitative trading strategies. The strict entry and exit conditions and the application of averaged MACD signals contribute to improved trading accuracy and drawdown control. Although the strategy performs better in unidirectional trend markets, measures such as introducing volatility filters, optimizing ranging market identification methods, setting trailing stop-losses, and establishing independent parameters for different instruments can further enhance the strategy's adaptability and robustness. Overall, this is a very promising cryptocurrency quantitative trading strategy that merits further optimization and live trading application.

- 1