MACD Trend Following Strategy

Overview

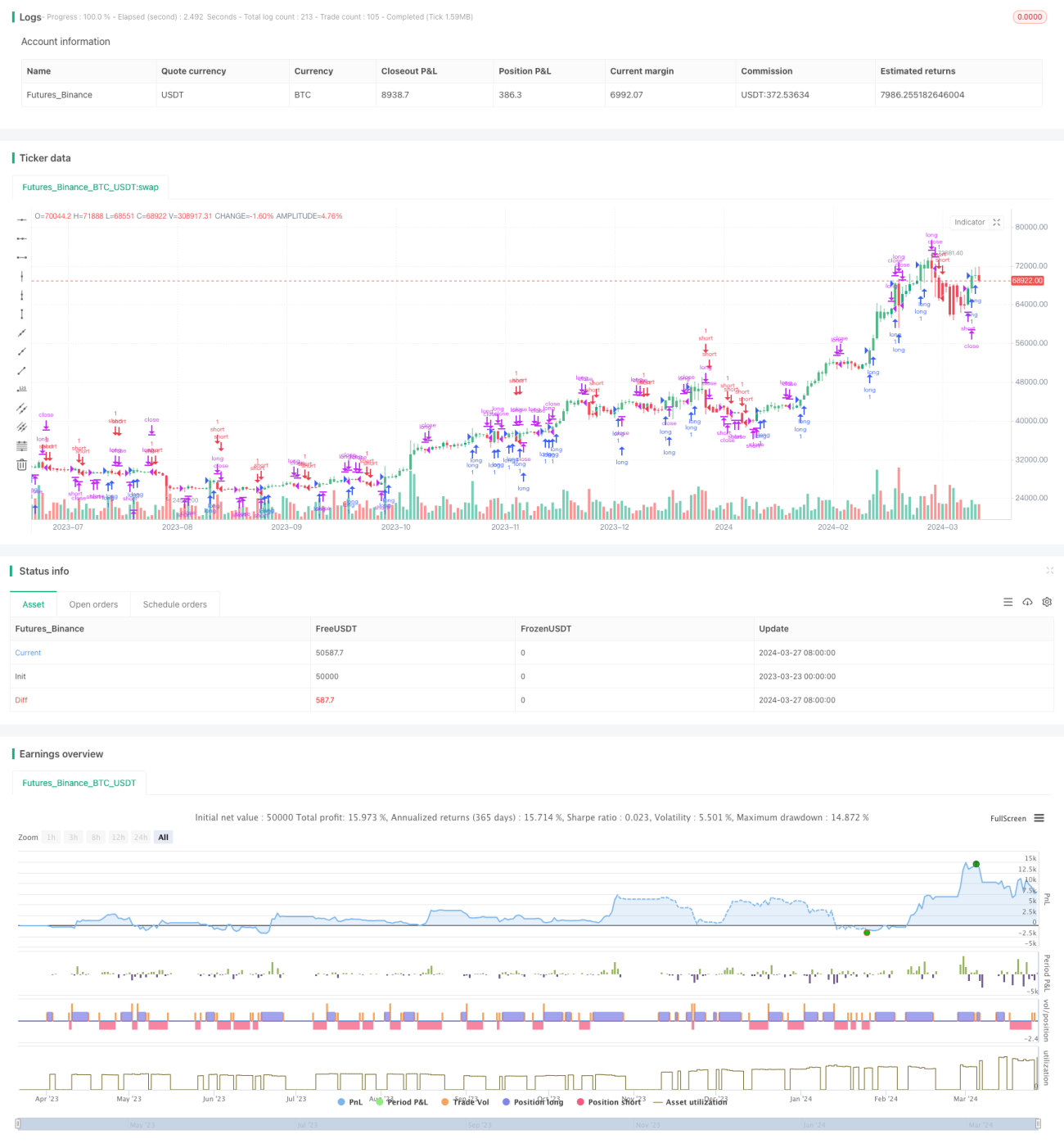

The MACD Trend Following Strategy is a quantitative trading strategy based on the MACD indicator. The main idea of this strategy is to use the golden cross and death cross signals of the MACD indicator to determine the direction of the trend and establish long or short positions at appropriate times. When the MACD line crosses above the signal line and above the zero axis, a long position is opened; when the MACD line crosses below the signal line and below the zero axis, a short position is opened. The strategy uses the most recent low point as the stop loss for long positions and the most recent high point as the stop loss for short positions. The closing condition is when the MACD line crosses the signal line in the opposite direction.

Strategy Principle

The core principle of the MACD Trend Following Strategy is to use the MACD indicator to capture the formation and reversal of trends. The MACD indicator consists of the difference between two moving averages (fast and slow) and is used in conjunction with a signal line to generate trading signals. When the MACD line crosses above the signal line and above the zero axis, it indicates an upward trend is forming, and a long position is opened. When the MACD line crosses below the signal line and below the zero axis, it indicates a downward trend is forming, and a short position is opened. The strategy uses the most recent significant low point as the stop loss for long positions and the most recent significant high point as the stop loss for short positions to control risk. When the MACD line crosses the signal line in the opposite direction, the current position is closed.

Strategy Advantages

-

The MACD Trend Following Strategy can effectively capture trending opportunities by establishing positions at the beginning of trend formation, fully utilizing the momentum of the trend.

-

The strategy uses both the MACD golden/death cross and the zero axis as filtering conditions, which can better filter out false signals in a oscillating market.

-

The strategy uses the most recent significant high and low points as stop loss levels, which can control the risk exposure of a single trade.

-

The strategy logic is clear, easy to understand and implement, making it suitable for beginners to learn.

Strategy Risks

-

The MACD indicator is essentially a lagging indicator, which may experience significant drawdowns at the beginning of trend reversals.

-

The strategy may generate frequent trades in a oscillating market, leading to high transaction costs.

-

The setting of stop loss levels depends on the most recent significant high and low points, which may result in premature or delayed stop losses in certain situations.

-

The strategy does not consider position sizing and money management, which need to be optimized based on specific circumstances in practical applications.

Strategy Optimization Directions

-

Consider introducing other technical indicators or price behavior patterns as filtering conditions to improve the reliability and accuracy of signals.

-

Optimize the method of setting stop loss levels, such as using ATR or percentage-based stop losses, to better control risk.

-

Introduce position sizing and money management mechanisms to dynamically adjust position sizes based on market volatility and account equity.

-

Optimize and adjust parameters for different markets and trading instruments to find the most suitable parameter combinations.

Summary

The MACD Trend Following Strategy is a simple and effective quantitative trading strategy that captures trending opportunities by leveraging the characteristics of the MACD indicator. The strategy has a clear logic, is easy to understand and implement, making it suitable for beginners to learn. However, in practical applications, attention needs to be paid to risk control, and it should be combined with other methods for optimization and improvement to achieve more robust trading performance.

/*backtest

start: 2023-03-23 00:00:00

end: 2024-03-28 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("MACD trendfollow", shorttitle="MACD TF", overlay=true)

// switch = input(true, title="Enable MACD Bar Color")

// X001TK MACD trendfollow Strategy- 1