Dual Range Filter Momentum Trading Strategy

Overview

This strategy is a momentum trading strategy based on a dual range filter. The strategy calculates smooth ranges for fast and slow periods to obtain a comprehensive range filter, which is used to determine the current price trend. When the price crosses above/below this range, the strategy generates buy/sell signals. Additionally, the strategy sets four gradient take-profit levels and one stop-loss level to control risk and lock in profits.

Strategy Principle

- Calculate smooth ranges for fast and slow periods. The fast range uses a shorter period and a smaller multiple, while the slow range uses a longer period and a larger multiple.

- Use the average of the fast and slow ranges as the comprehensive range filter (TRF).

- Determine upward and downward trends by comparing the current price with the previous price.

- Calculate dynamic upper (FUB) and lower (FLB) bands as references for the trend.

- Generate buy and sell signals based on the relationship between the closing price and TRF.

- Set four gradient take-profit levels and one stop-loss level, corresponding to different position percentages and profit/loss percentages.

Advantage Analysis

- The dual range filter combines fast and slow periods, enabling the strategy to adapt to different market paces and capture more trading opportunities.

- The design of dynamic upper and lower bands helps the strategy align with the current trend and reduces false signals.

- The four gradient take-profit levels allow the strategy to secure more profits when the trend continues while locking in partial gains when the trend reverses.

- The stop-loss setting helps control the maximum loss per trade and protects account safety.

Risk Analysis

- During market fluctuations or range-bound conditions, the strategy may generate many false signals, leading to frequent trading and commission losses.

- The gradient take-profit settings may cause some profits to be locked in prematurely, preventing the strategy from fully benefiting from trend movements.

- The stop-loss setting may not completely avoid extreme losses caused by black swan events.

Optimization Direction

- Consider incorporating more technical indicators or market sentiment indicators as auxiliary conditions for trend determination to reduce false signals.

- For take-profit and stop-loss settings, dynamically adjust them according to different market environments and trading instruments to improve the strategy's adaptability.

- Based on backtesting results, further optimize parameter settings, such as the selection of fast and slow range periods, and the percentage settings for take-profit and stop-loss levels, to enhance the strategy's stability and profitability.

Summary

The dual range filter momentum trading strategy constructs a comprehensive filter using smooth ranges from fast and slow periods, combined with dynamic upper and lower bands to determine price trends and generate buy/sell signals. The strategy also sets four gradient take-profit levels and one stop-loss level to control risk and lock in profits. This strategy is suitable for use in trending markets but may generate more false signals in fluctuating markets. In the future, consider introducing more indicators, optimizing take-profit and stop-loss settings, and dynamically adjusting parameters to improve the strategy's adaptability and stability.

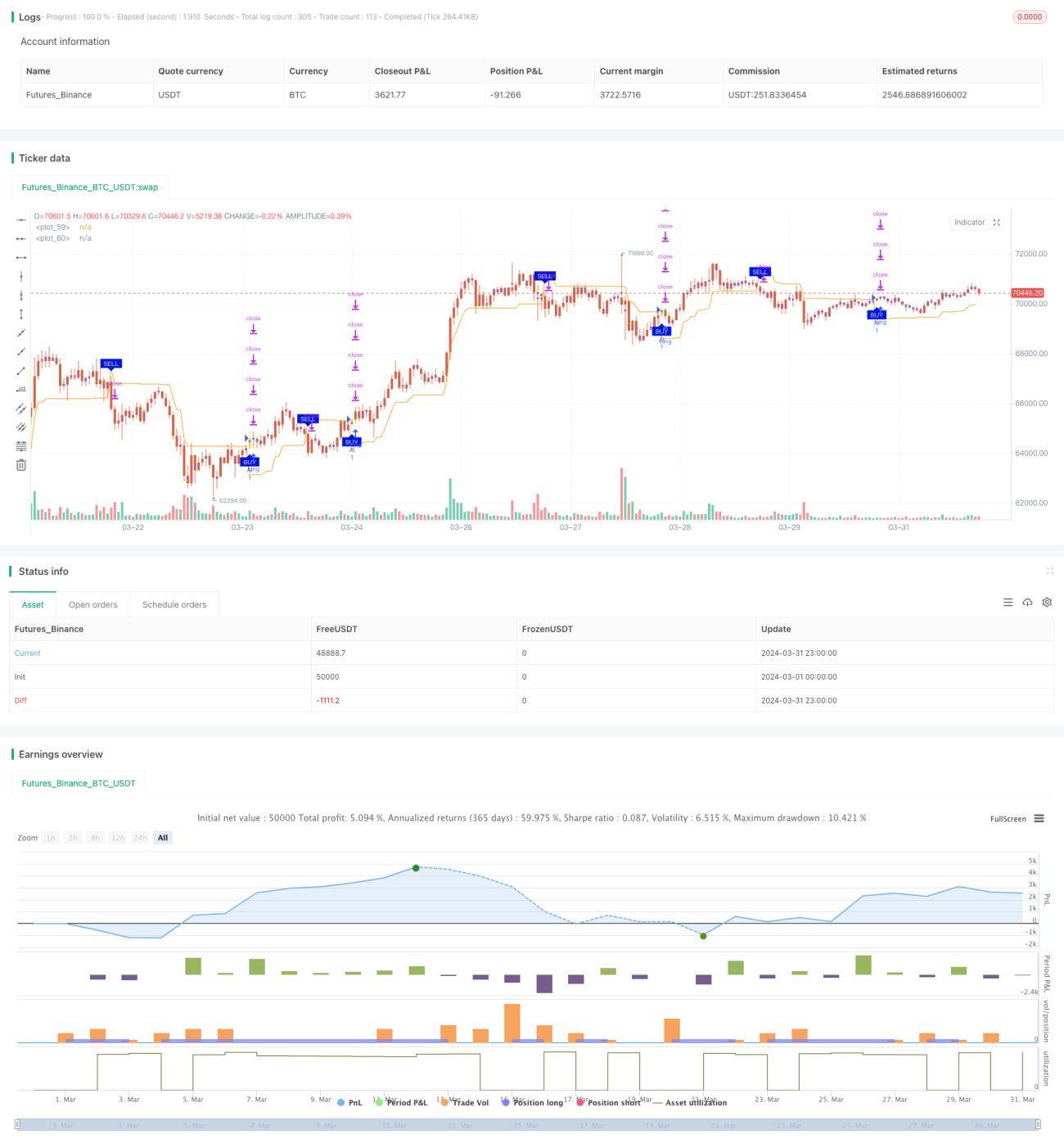

/*backtest

start: 2024-03-01 00:00:00

end: 2024-03-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=5

strategy(title='2"Twin Range Filter', overlay=true)

strat_dir_input = input.string(title='İşlem Yönü', defval='Alis', options=['Alis', 'Satis', 'Tum'])- 1