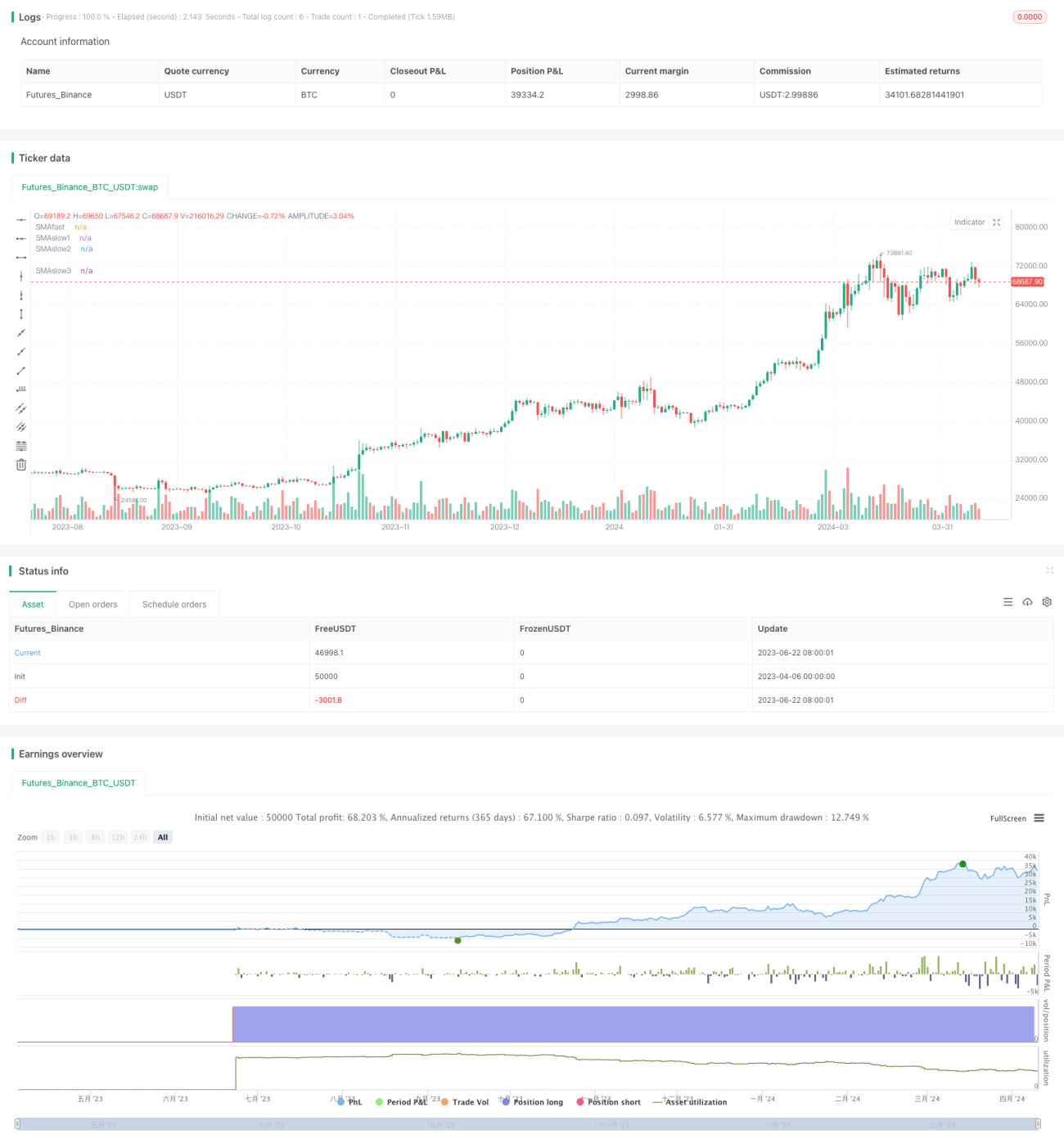

Moving Average Crossover + MACD Slow Line Momentum Strategy

Overview

This strategy combines moving average crossover and MACD indicator as the main trading signals. It uses the crossover of a fast moving average with multiple slow moving averages as the entry signal, and the positive/negative value of the MACD slow line histogram as the trend confirmation. The strategy sets multiple take-profit and stop-loss levels upon entry, and continuously adjusts the stop-loss level as the holding time increases to lock in profits.

Strategy Principle

- When the fast MA crosses above the slow MA1, the closing price is above the slow MA2, and the MACD histogram is greater than 0, go long;

- When the fast MA crosses below the slow MA1, the closing price is below the slow MA2, and the MACD histogram is less than 0, go short;

- Set multiple take-profit and stop-loss levels upon entry. The take-profit levels are based on risk preference, while the stop-loss levels are adjusted continuously as the holding time increases to gradually lock in profits;

- The periods of moving averages, MACD parameters, take-profit and stop-loss levels, etc., can all be flexibly adjusted to adapt to different market conditions.

This strategy uses MA crossover to capture trends and MACD to confirm the direction, enhancing the reliability of trend judgment. The multiple take-profit and stop-loss design helps to better control risks and profits.

Strategy Advantages

- MA crossover is a classic trend-following method that can timely capture the formation of trends;

- The use of multiple MAs can more comprehensively judge the strength and persistence of trends;

- The MACD indicator can effectively identify trends and judge momentum, serving as a strong supplement to MA crossover;

- The multiple take-profit and dynamic stop-loss design can both control risks and let profits run, enhancing the robustness of the system;

- The parameters are adjustable and adaptable, and can be flexibly set according to different instruments and timeframes.

Strategy Risks

- MA crossover has the risk of signal lag, which may miss early trends or chase high;

- Improper parameter settings may lead to overtrading or overly long holding periods, increasing costs and risks;

- Overly aggressive stop-loss levels may lead to premature stop-outs, while overly conservative take-profit levels may affect returns;

- Abrupt trend changes or market anomalies may cause the strategy to fail.

These risks can be controlled by optimizing parameters, adjusting positions, setting additional conditions, etc. However, no strategy can completely avoid risks, and investors need to treat it with caution.

Strategy Optimization Directions

- Consider introducing more indicators, such as RSI, Bollinger Bands, etc., to further confirm trends and signals;

- Conduct more refined optimization on the setting of take-profit and stop-loss levels, such as considering ATR or percentage-based levels;

- Dynamically adjust parameters based on market volatility to improve adaptability;

- Introduce a position sizing module to adjust position sizes based on risk conditions;

- Ensemble the strategy to establish a strategy portfolio to diversify risks.

Through continuous optimization and improvement, the strategy can become more robust and reliable, better adapting to the changing market environment. But optimization needs to be done with caution to avoid overfitting.

Summary

This strategy combines MA crossover and MACD indicators to construct a relatively complete trading system. The design of multiple MAs and multiple operations enhances the system's trend-capturing and risk-control capabilities. The strategy logic is clear and easy to understand and implement, suitable for further optimization and improvement. However, it still needs to be applied with caution in practice, paying attention to risk control. With reasonable optimization and configuration, this strategy has the potential to become a robust and effective trading tool.

- 1