AlphaTradingBot Trading Strategy

Overview

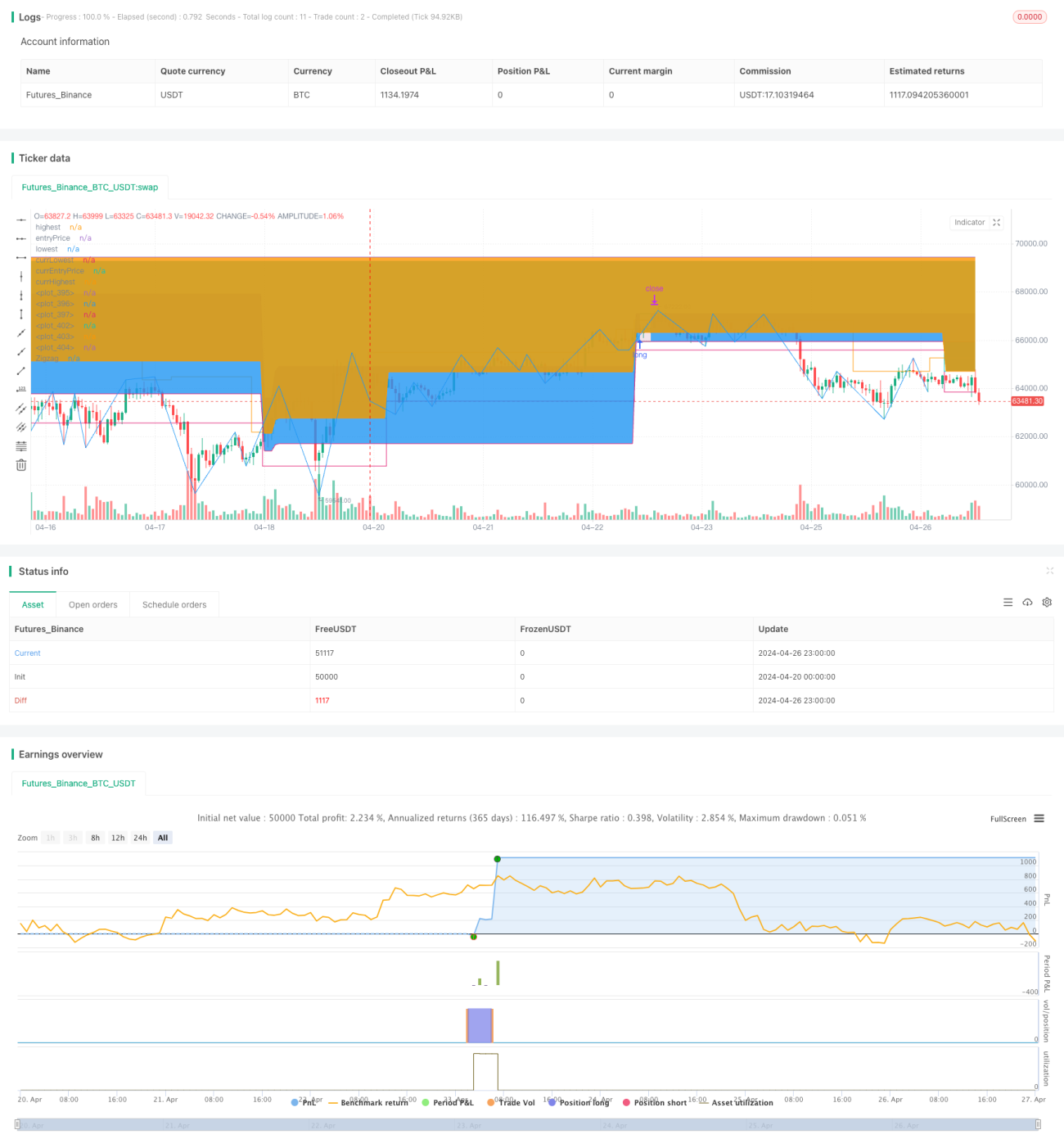

AlphaTradingBot is a day trading strategy based on the Zigzag indicator and Fibonacci sequence. The strategy identifies the high points (HH) and low points (LL) of the market to determine the trend, and uses Fibonacci retracements and expansions to set entry points, take-profits, and stop-losses. The strategy only runs within a specified date range and can go both long and short, with some ability to grasp trends and control risk-reward ratio.

Strategy Principle

- Use the Zigzag indicator to identify the market's high points (HH), low points (LL), higher lows (HL), and lower highs (LH).

- When an HH appears, it is regarded as the beginning of an uptrend and the strategy starts looking for long opportunities; when an LL appears, it is regarded as the beginning of a downtrend and the strategy starts looking for short opportunities.

- In an uptrend, if an HL appears, the range formed by the HL and the previous LL is used as the Fibonacci retracement range for longs. If the price breaks the previous high, a long order is placed in the 23.6%-38.2% (adjustable) retracement zone, with the stop-loss set at the 61.8% retracement level and the take-profit calculated based on the RR value (adjustable).

- In a downtrend, if an LH appears, the range formed by the LH and the previous HH is used as the Fibonacci retracement range for shorts. If the price breaks the previous low, a short order is placed in the 61.8%-76.4% (adjustable) retracement zone, with the stop-loss set at the 38.2% retracement level and the take-profit calculated based on the RR value (adjustable).

- Order management: Only one order is placed per signal until that order is closed. If the loss of a single trade reaches X% (adjustable) of the total account balance, the strategy stops running.

Advantage Analysis

- Strong trend-following ability. Effectively identifies trends through Zigzag and can enter at the early stage of a trend.

- Clear retracement logic. Uses Fibonacci retracements to set entry zones and enters during trend retracements, resulting in a relatively high win rate.

- Controllable risk. Controls the risk of each trade by setting a maximum single-trade loss percentage, while a strict stop-loss system also ensures overall risk control.

- Optimizable risk-reward ratio. The RR value can be adjusted according to market characteristics and personal preferences to optimize the strategy's risk-reward ratio.

Risk Analysis

- Frequent trading. Due to the high sensitivity of Zigzag, it may generate signals frequently, leading to over-trading.

- Imprecise trend identification. The trends determined by Zigzag may still have deviations, resulting in less-than-ideal entry timing.

- Poor performance in range-bound markets. In sideways markets, the strategy may generate more losing trades.

- Limited running period. The strategy only runs within a specified date range and may miss some market moves.

Optimization Direction

- Introduce more technical indicators, such as MA and MACD, to improve the accuracy of trend identification.

- Optimize position management, such as dynamically adjusting position size based on indicators like ATR.

- Optimize take-profit and stop-loss logic, such as dynamically adjusting stop-loss levels based on market volatility.

- Introduce market sentiment indicators to avoid entering during extreme optimism or pessimism.

- Relax the date restriction to increase the strategy's versatility.

Summary

AlphaTradingBot is a trend-following intraday strategy based on the Zigzag indicator and Fibonacci retracements. It determines trends through high and low points and enters during trend retracements, aiming to pursue a higher win rate and risk-reward ratio. The strategy's advantages lie in its strong trend-grasping ability, clear retracement logic, and measurable risk, but it also faces risks such as over-trading, trend misjudgment, and poor performance in range-bound markets. In the future, the strategy can be optimized in terms of technical indicators, position management, take-profit and stop-loss, and market sentiment to improve its robustness and profitability.

- 1