EMA Cross Strategy with RSI Divergence, 30-Minute Trend Identification, and Price Exhaustion

Overview

This strategy combines technical indicators such as EMA crossover, RSI divergence, 30-minute trend identification, and price exhaustion to capture market trends and price turning points. The strategy determines the trend direction using the crossover of EMA13 and EMA26, identifies potential trend reversals using RSI divergence, and considers the trend status within the 30-minute timeframe and price exhaustion conditions to optimize entry points.

Strategy Principles

- EMA Crossover: A buy signal is generated when EMA13 crosses above EMA26, and a sell signal is generated when it crosses below.

- RSI Divergence: A bullish divergence occurs when the price makes a new low, but RSI does not; a bearish divergence occurs when the price makes a new high, but RSI does not.

- 30-Minute Trend Identification: The current trend status within the 30-minute timeframe is determined by comparing the closing price with the 30-minute EMA5 and EMA10.

- Price Exhaustion: The RSI indicator is used to identify overbought and oversold conditions.

- Trading Signals: Combining the above factors, a buy signal is generated when there is an EMA crossover, RSI divergence, an uptrend in the 30-minute timeframe, and oversold conditions; a sell signal is generated when there is an EMA crossover, RSI divergence, a downtrend in the 30-minute timeframe, and overbought conditions.

Strategy Advantages

- Multi-dimensional Analysis: Combining multiple dimensions such as trend, momentum, and price exhaustion improves signal accuracy.

- Trend Confirmation: Avoids frequent trading in choppy markets by confirming trends within the 30-minute timeframe.

- Turning Point Capture: Captures potential trend reversal points using RSI divergence and price exhaustion.

- Risk Control: Reduces risk by trading only after trend confirmation and turning point signals appear.

Strategy Risks

- Parameter Optimization: The parameters used in the strategy, such as EMA and RSI periods, may need to be optimized for different markets and assets.

- Trend Transitions: During the early stages of a trend transition, EMA crossover and RSI divergence signals may be delayed or misleading.

- False Signals: In some cases, RSI divergence may generate false signals, leading to incorrect trades.

- Unexpected Events: The strategy may not be able to handle unexpected events and irrational market fluctuations.

Strategy Optimization Directions

- Dynamic Parameter Optimization: Dynamically adjust parameters such as EMA and RSI periods based on market conditions and volatility.

- Trend Strength Filtering: Introduce trend strength indicators like ADX to filter signals in weak trends or choppy markets.

- Multi-Timeframe Confirmation: Combine trends and signals from multiple timeframes to improve signal reliability.

- Stop Loss and Take Profit: Implement appropriate stop loss and take profit strategies to further control risk and optimize returns.

Summary

This strategy analyzes the market from multiple dimensions by combining technical indicators such as EMA crossover, RSI divergence, 30-minute trend identification, and price exhaustion to capture trends and potential turning points. The strategy's advantages lie in multi-dimensional analysis, trend confirmation, turning point capture, and risk control. However, it also faces risks such as parameter optimization, trend transitions, false signals, and unexpected events. In the future, the strategy can be optimized through dynamic parameter optimization, trend strength filtering, multi-timeframe confirmation, and the implementation of stop loss and take profit strategies to further improve its robustness and profitability.

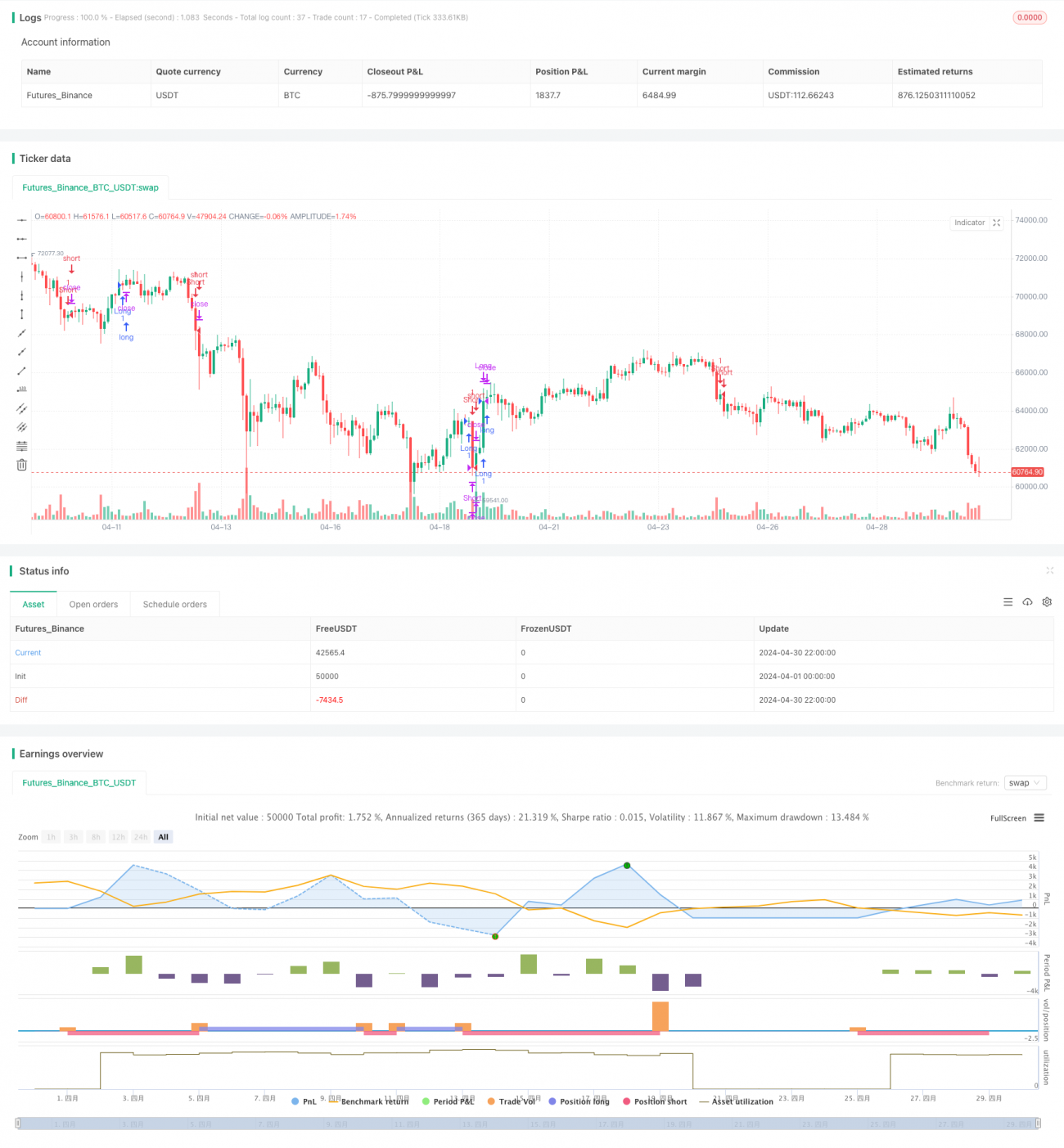

/*backtest

start: 2024-04-01 00:00:00

end: 2024-04-30 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("EMA Cross Strategy with RSI Divergence, 30-Minute Trend Identification, and Price Exhaustion", overlay=true)

// Definição das médias móveis exponenciais para tendência de curto prazo (30 minutos)- 1