Alligator Long-Term Trend Following Trading Strategy

Overview

The Alligator Long-Term Trend Following Trading Strategy is a quantitative trading strategy based on the Williams Alligator indicator. The strategy utilizes a combination of moving averages with different periods to capture the main trends in the market, suitable for medium to long-term trend following trades. The main idea of the strategy is to determine the direction and strength of the trend by the opening direction of the Alligator indicator and the relative position of the price to the Alligator indicator, and make trading decisions accordingly.

Strategy Principles

The Alligator Long-Term Trend Following Trading Strategy uses three moving averages with different periods to construct the Alligator indicator, namely:

- Jaw line: 13-period SMMA, shifted 8 bars into the future

- Teeth line: 8-period SMMA, shifted 5 bars into the future

- Lips line: 5-period SMMA, shifted 3 bars into the future

When the Alligator indicator's mouth opens upward, i.e., the Jaw line is at the bottom, the Teeth line is in the middle, and the Lips line is at the top, and the price is above the Alligator indicator, the strategy will open a long position. This situation indicates that an upward trend wave has been confirmed, and we want to hold the position until the trend ends.

When the price breaks below the Jaw line, the strategy will close the long position. This ensures that we will not continue to hold positions in a bear market.

Strategy Advantages

- Suitable for medium to long-term trading: The strategy is based on the Alligator indicator, which can effectively capture the main trends in the market, making it very suitable for medium to long-term trend following trades.

- Low trading frequency: The strategy only opens positions when a trend is confirmed and closes positions when the trend ends, resulting in a relatively low trading frequency, which can effectively reduce trading costs.

- Wide range of applications: The strategy can be applied to various financial markets, such as forex, cryptocurrencies, etc., with strong adaptability and flexibility.

- No need for parameter optimization: The strategy completely follows market trends and does not require parameter optimization, making it simple and easy to use.

Strategy Risks

- Potential slippage risk: In cases of severe market fluctuations or insufficient liquidity, trading orders may not be executed at the expected price, leading to slippage risk.

- Lack of fixed risk management: The strategy does not have fixed risk management settings, and the position size of each trade needs to be adjusted according to one's risk preference.

- Possible missed short-term opportunities: As the strategy focuses on capturing medium to long-term trends, it may miss some short-term trading opportunities.

Strategy Optimization Directions

- Add risk management module: Consider adding some risk management measures, such as stop-loss, dynamic position adjustment, etc., to better control risks.

- Combine with other technical indicators: Try combining the Alligator indicator with other technical indicators, such as RSI, MACD, etc., to improve the accuracy and reliability of the strategy.

- Optimize parameter settings: Although the strategy does not require parameter optimization, you can try backtesting different time periods and trading targets to find the optimal parameter combination.

Summary

The Alligator Long-Term Trend Following Trading Strategy is a simple, easy-to-use, and widely applicable quantitative trading strategy. By utilizing the Alligator indicator to capture the main trends in the market, the strategy can achieve stable returns over the medium to long term. Although the strategy has some potential risks, by adding risk management modules, combining with other technical indicators, and optimizing parameter settings, the strategy's performance and stability can be further improved. For investors who prefer medium to long-term trend following trades, the Alligator Long-Term Trend Following Trading Strategy is a choice worth considering.

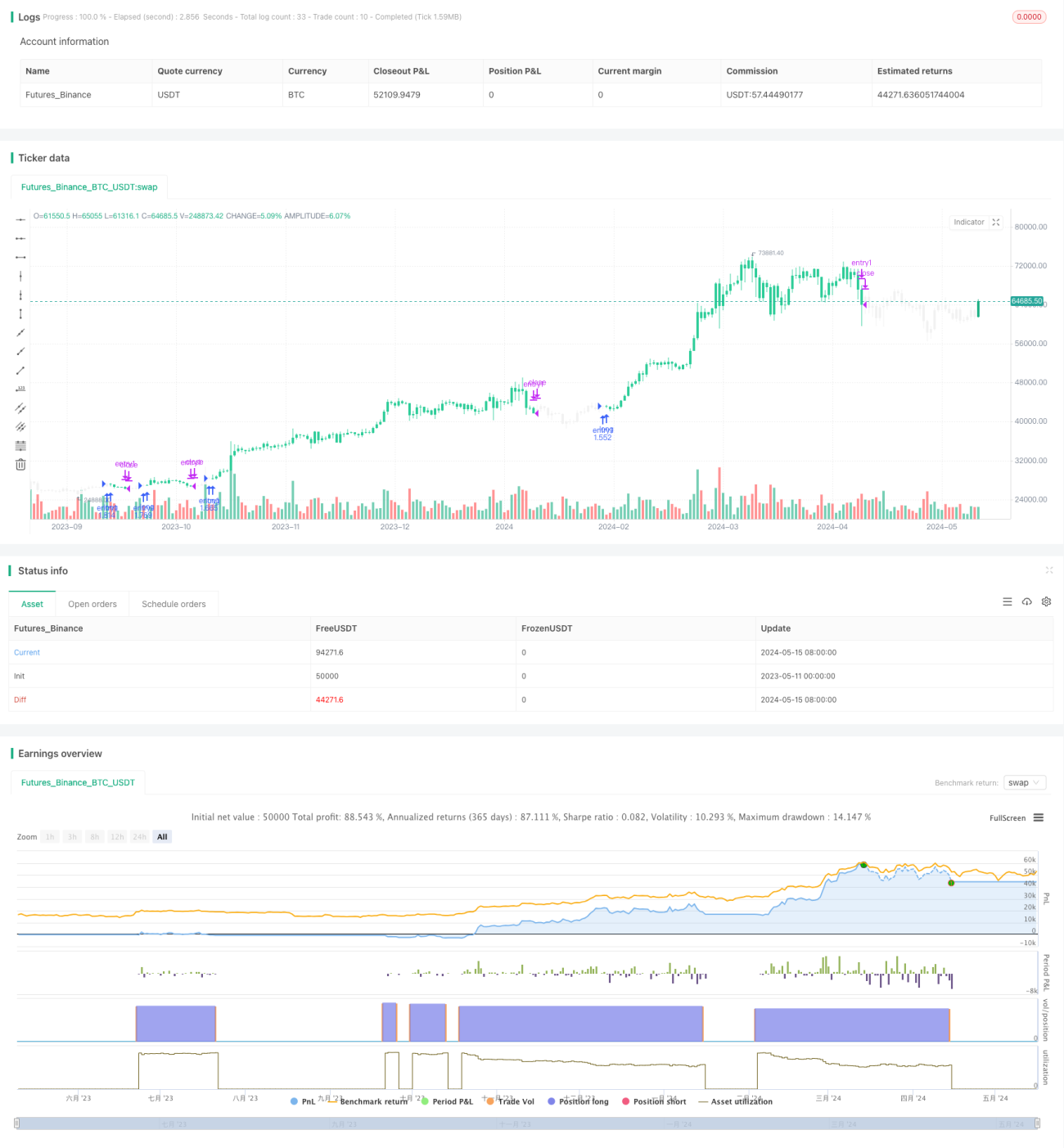

/*backtest

start: 2023-05-11 00:00:00

end: 2024-05-16 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//_______ <licence>

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Skyrex

- 1