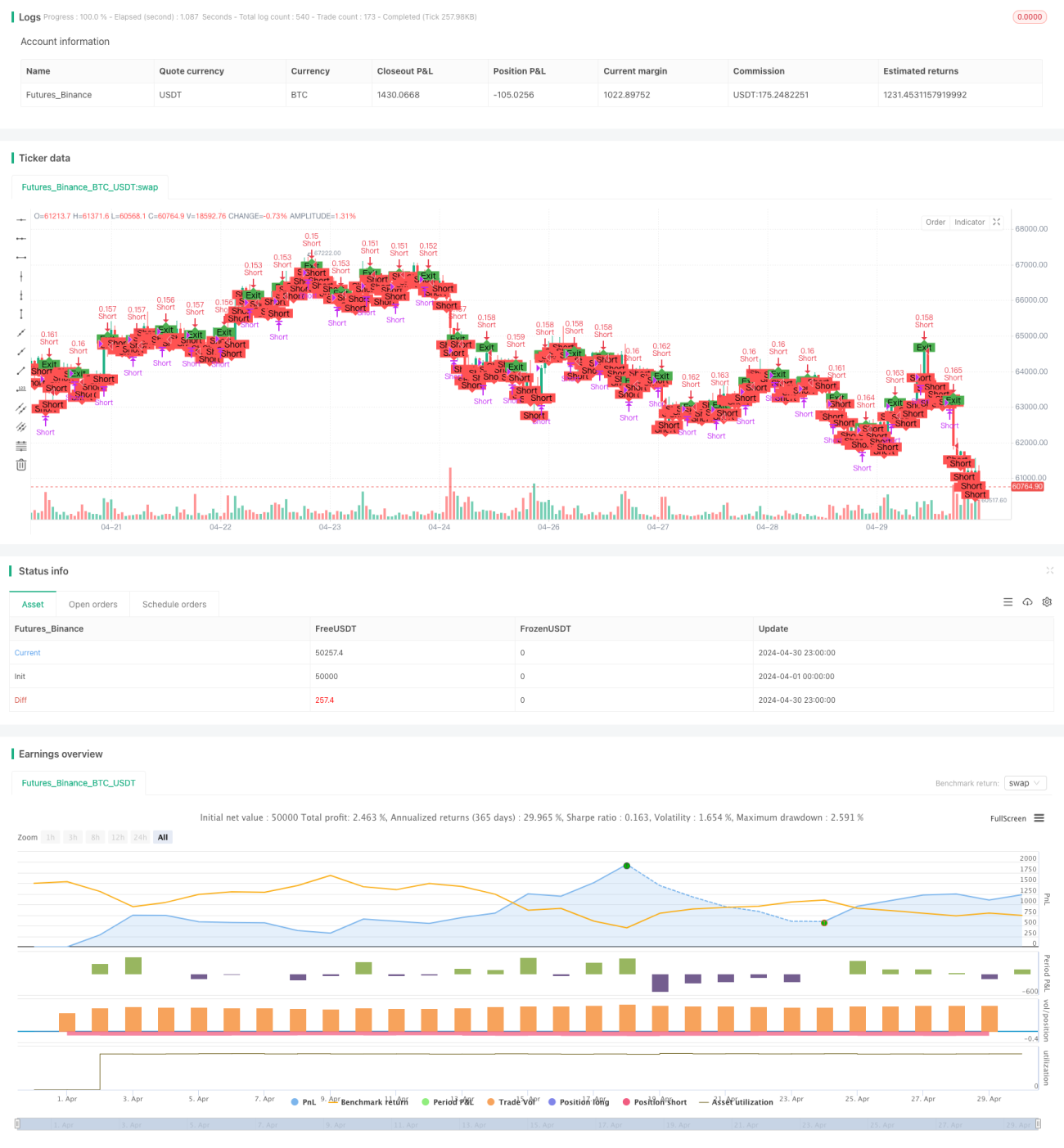

Overview

The "Short-term Short Selling Strategy for High-liquidity Currency Pairs" aims to capitalize on short-term downward movements in high-liquidity currency pairs by entering short positions when the price is expected to drop. The strategy enters short positions based on specific conditions and employs dynamic position sizing and risk management measures to control risks and lock in profits.

The main ideas of the strategy are as follows:

- Select high-liquidity currency pairs as the trading instruments.

- Enter short positions based on price drop percentage conditions.

- Dynamically calculate position size based on a predefined risk percentage of the account equity.

- Set stop-loss and take-profit conditions to limit potential losses and lock in profits.

- Exit the trade based on trade duration or price movement conditions.

Strategy Principles

This strategy takes advantage of the short-term downward trends in high-liquidity currency pairs. When the price meets specific conditions, the strategy enters a short position. The specific principles are as follows:

- Ensure there are no open trades to guarantee only one active trade at a time.

- Set the duration of the short trade, which is 7 days by default.

- Enter a short position when the price has dropped by a predefined percentage (default is 30%) from the entry price.

- Dynamically calculate the position size based on a predefined risk percentage of the account equity to control the capital allocation for each trade and overall risk.

- Set stop-loss and take-profit conditions. When the price moves unfavorably, the strategy exits the trade to minimize losses; when the price moves favorably, the strategy exits the trade to lock in profits.

- Exit the trade based on trade duration or price movement conditions.

Strategy Advantages

- Short-term trading: The strategy focuses on capturing short-term downward movements in high-liquidity currency pairs, with a relatively short trading cycle, which helps achieve profit targets quickly.

- Dynamic position sizing: By dynamically calculating the position size based on a predefined risk percentage of the account equity, the strategy effectively controls the risk exposure for each trade and adapts to different market conditions.

- Risk management: The strategy sets stop-loss and take-profit conditions to exit trades promptly when the price moves unfavorably, minimizing potential losses, and to lock in profits when the price moves favorably, protecting realized gains.

- Simplicity and ease of use: The conditions and logic of the strategy are relatively simple and easy to understand and implement, making it suitable for traders with different levels of experience.

Strategy Risks

- Market risk: The price movements of currency pairs are uncertain, and unexpected events or unusual trends may occur in the short term, causing the strategy to perform differently than expected.

- Slippage risk: In cases of high market volatility or low liquidity, the actual execution price may differ from the expected price, impacting the profitability of the strategy.

- Parameter optimization risk: The performance of the strategy depends on the selection of multiple parameters, such as short duration, price drop percentage, stop-loss, and take-profit percentages. Inappropriate parameter settings may lead to suboptimal performance of the strategy.

Strategy Optimization Directions

- Introduce more technical indicators: Incorporate other technical indicators, such as moving averages, Relative Strength Index (RSI), etc., into the entry and exit conditions to improve the reliability and accuracy of entry signals.

- Optimize parameter selection: Conduct optimization and sensitivity analysis on key parameters, such as short duration, price drop percentage, stop-loss, and take-profit percentages, to find the optimal combination of parameters that enhance the profitability and stability of the strategy.

- Incorporate market sentiment analysis: Combine market sentiment indicators, such as the Volatility Index (VIX), trading volume, etc., to assess market sentiment and avoid entering trades during periods of extreme pessimism or significantly reduced trading volume, improving the adaptability of the strategy.

- Multi-currency pair portfolio: Apply the strategy to multiple high-liquidity currency pairs to construct a diversified investment portfolio, spreading the risk of individual currency pairs and enhancing the overall stability of returns.

Summary

The "Short-term Short Selling Strategy for High-liquidity Currency Pairs" aims to capture short-term downward trends in high-liquidity currency pairs by entering short positions under specific conditions and employing dynamic position sizing and risk management measures to generate profits while controlling risks. The advantages of the strategy lie in its short-term trading approach, dynamic position sizing, and simplicity. However, it also faces market risk, slippage risk, and parameter optimization risk. To further optimize the strategy, considerations can be given to introducing more technical indicators, optimizing parameter selection, incorporating market sentiment analysis, and applying the strategy to multiple currency pairs. With continuous optimization and refinement, the strategy has the potential to achieve stable profitability in the currency market.

- 1