Trend Following Average True Range Trailing Stop Strategy

Overview

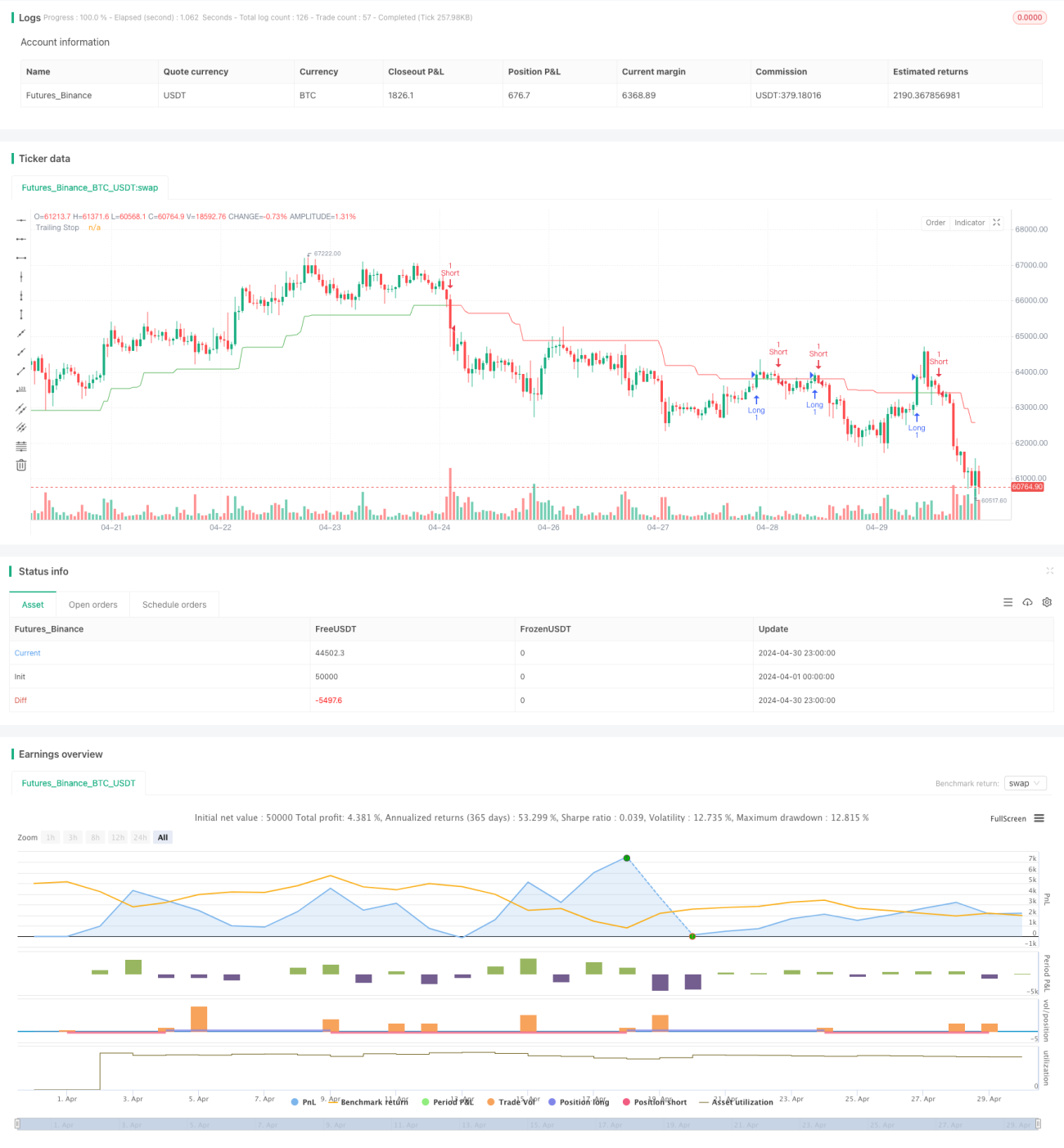

This strategy uses the Average True Range (ATR) as the basis for a Trailing Stop (TS), dynamically adjusting the stop-loss position to follow the trend. When the price moves in a favorable direction, the stop-loss position is adjusted accordingly to lock in profits; when the price moves in an adverse direction, the stop-loss position remains unchanged, and once the price reaches the stop-loss price, the position is closed. The key to this strategy lies in the dynamic adjustment of the stop-loss position, which can both protect profits and allow profits to expand as the trend continues.

Strategy Principle

- Calculate the ATR as the basis for the trailing stop. ATR reflects market volatility and is used to measure the average magnitude of price changes.

- Calculate the stop-loss distance nLoss based on the ATR and the KeyValue parameter. KeyValue is a user-defined multiplier, and nLoss is the product of KeyValue and ATR, indicating that the stop-loss distance is several times the ATR.

- Calculate the dynamic trailing stop position xATRTrailingStop. For a long position, it is set to the greater of "the highest price of the previous candle and (close - nLoss)"; for a short position, it is set to the lesser of "the lowest price of the previous candle and (close + nLoss)".

- Generate entry signals. When the closing price crosses above xATRTrailingStop, go long; when the closing price crosses below xATRTrailingStop, go short.

Advantage Analysis

- The stop-loss position is dynamically adjusted with price fluctuations, allowing profits to be locked in while also allowing profits to expand as the trend continues.

- The stop-loss position is based on the ATR calculation, which can objectively reflect market volatility and is more flexible and effective compared to subjectively set fixed stop-losses.

- By amplifying the ATR with the KeyValue parameter, you can set an appropriate stop-loss distance based on your risk preference. A larger KeyValue will result in a wider stop-loss space and fewer stop-loss occurrences.

Risk Analysis

- Trend-following strategies perform poorly in choppy markets, and when the unilateral trend is not clear, frequent stop-losses can lead to rapid loss of funds.

- The entry timing relies on the cross signal between the closing price and the dynamic stop-loss line, which may result in consecutive small stop-losses in a choppy market.

- Trailing stop strategies cannot avoid gaps caused by significant bearish or bullish news, and the adjustment speed of the stop-loss position cannot keep up with the price change speed, resulting in actual losses far greater than expected controllable losses.

Optimization Direction

- Trend judgment indicators, such as moving average systems and momentum indicators, can be added to the strategy to only enter the market when the trend is clear, avoiding frequent trading in choppy markets.

- A take-profit strategy can be considered, such as calculating position sizes based on the Kelly formula, setting fixed profit points for retracement stop-profits, etc., to reduce the possibility of potential profit givebacks at the end of a trend.

- For gap openings, a maximum stop-loss limit can be set, such as a fixed amount or a fixed percentage. Once this limit is reached, the position is immediately stopped out regardless of where the dynamic stop-loss price is.

Summary

The ATR trailing stop strategy can dynamically adjust the stop-loss position based on the magnitude of price fluctuations and can achieve good results in trending markets. However, this strategy also has risks such as inability to cope with choppy markets, excessive stop-loss frequency, and difficulty in avoiding gap openings. To address these shortcomings, the strategy can be optimized and improved in terms of trend judgment, take-profit strategies, and maximum stop-loss limits. With these adjustments, the strategy's adaptability and profitability can hopefully be enhanced.

- 1