Standard Deviation DEV Trading Strategy Based on Relative Strength Index RSI and Simple Moving Average SMA

Overview

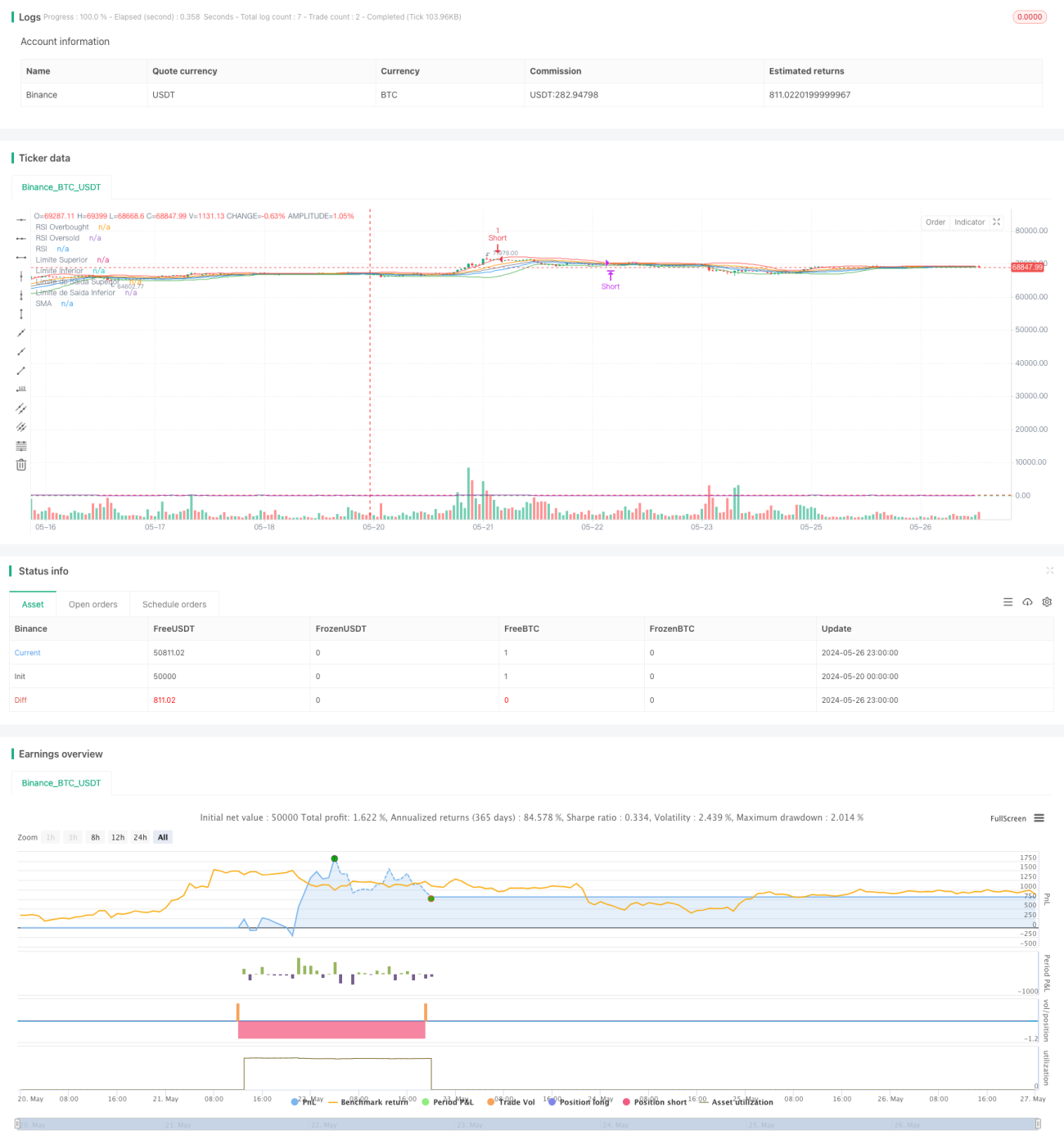

This Pine Script strategy is based on the Relative Strength Index (RSI) and the standard deviation (DEV) of price volatility. It determines entry points by comparing the price with upper and lower bands, while using RSI as an auxiliary filtering indicator. It generates long entry signals when the price breaks above the lower band and RSI is below the oversold threshold, and short entry signals when the price breaks below the upper band and RSI is above the overbought threshold. The strategy closes long positions when the price breaks below the exit lower band or RSI exceeds the overbought threshold, and closes short positions when the price breaks above the exit upper band or RSI falls below the oversold threshold. This strategy can dynamically adjust according to market volatility conditions, cutting losses in time during high volatility and holding positions for profit during low volatility. It is a quantitative trading strategy that can adapt to different market states.

Strategy Principle

- Calculate the Simple Moving Average (SMA) and Standard Deviation (DEV) of the price over the past "length" periods.

- Construct a volatility channel with SMA as the centerline, SMA+thresholdEntryDEV as the upper band, and SMA-thresholdEntryDEV as the lower band.

- Simultaneously calculate the RSI indicator of the closing price over the past "rsiLength" periods.

- When the price breaks above the lower band and RSI is below the oversold threshold "rsiOversold", generate a long entry signal.

- When the price breaks below the upper band and RSI is above the overbought threshold "rsiOverbought", generate a short entry signal.

- Construct another narrower exit channel with SMA as the centerline, SMA+thresholdExitDEV as the upper band, and SMA-thresholdExitDEV as the lower band.

- When holding a long position, if the price breaks below the exit lower band or RSI exceeds the overbought threshold, close the long position.

- When holding a short position, if the price breaks above the exit upper band or RSI falls below the oversold threshold, close the short position.

Advantage Analysis

- By using both price behavior and momentum indicators for auxiliary judgment, it can effectively filter out false signals.

- By dynamically adjusting the channel width based on volatility, the strategy can adapt to different market states.

- By setting two sets of channels, it can cut losses in the early stage of price reversal and control drawdowns, while still being able to hold positions for profit after a trend is formed.

- The code logic and parameter settings are clear and easy to understand and optimize.

Risk Analysis

- When the market continues to run in a unilateral trend, the strategy may cut losses too early and miss out on trend profits.

- Parameter settings have a significant impact on the strategy's performance, and parameter optimization needs to be performed separately for different varieties and time frames.

- The strategy performs better in oscillating markets and average in trending markets. If a long-term trend suddenly reverses, the strategy may experience a larger drawdown.

- If the volatility of the underlying asset changes drastically, the fixed parameter settings may become invalid.

Optimization Direction

- Try introducing trend judgment indicators, such as long-short term moving average crossovers, ADX, etc., to distinguish between trending and oscillating markets and use different parameter settings.

- Consider using more adaptive volatility indicators, such as ATR, to dynamically adjust the width of the volatility channel.

- Before opening a position, perform trend judgment on the price movement to detect whether it is in a clear trend to avoid counter-trend trading.

- Use genetic algorithms, grid search, and other methods to optimize different parameter combinations and find the best parameter settings.

- Consider using different parameter settings for long and short positions to control risk exposure.

Summary

This strategy combines volatility channels and the Relative Strength Index to make entry and exit decisions based on price fluctuations while referencing the RSI indicator. It can better capture short-term trends and cut losses and take profits in a timely manner. However, the strategy's performance is relatively sensitive to parameter settings and needs to be optimized for different market environments and underlying assets. At the same time, consider introducing other indicators to assist in judging market trends in order to fully leverage the advantages of this strategy. Overall, this strategy has a clear idea, rigorous logic, and is a good quantitative trading strategy.

- 1