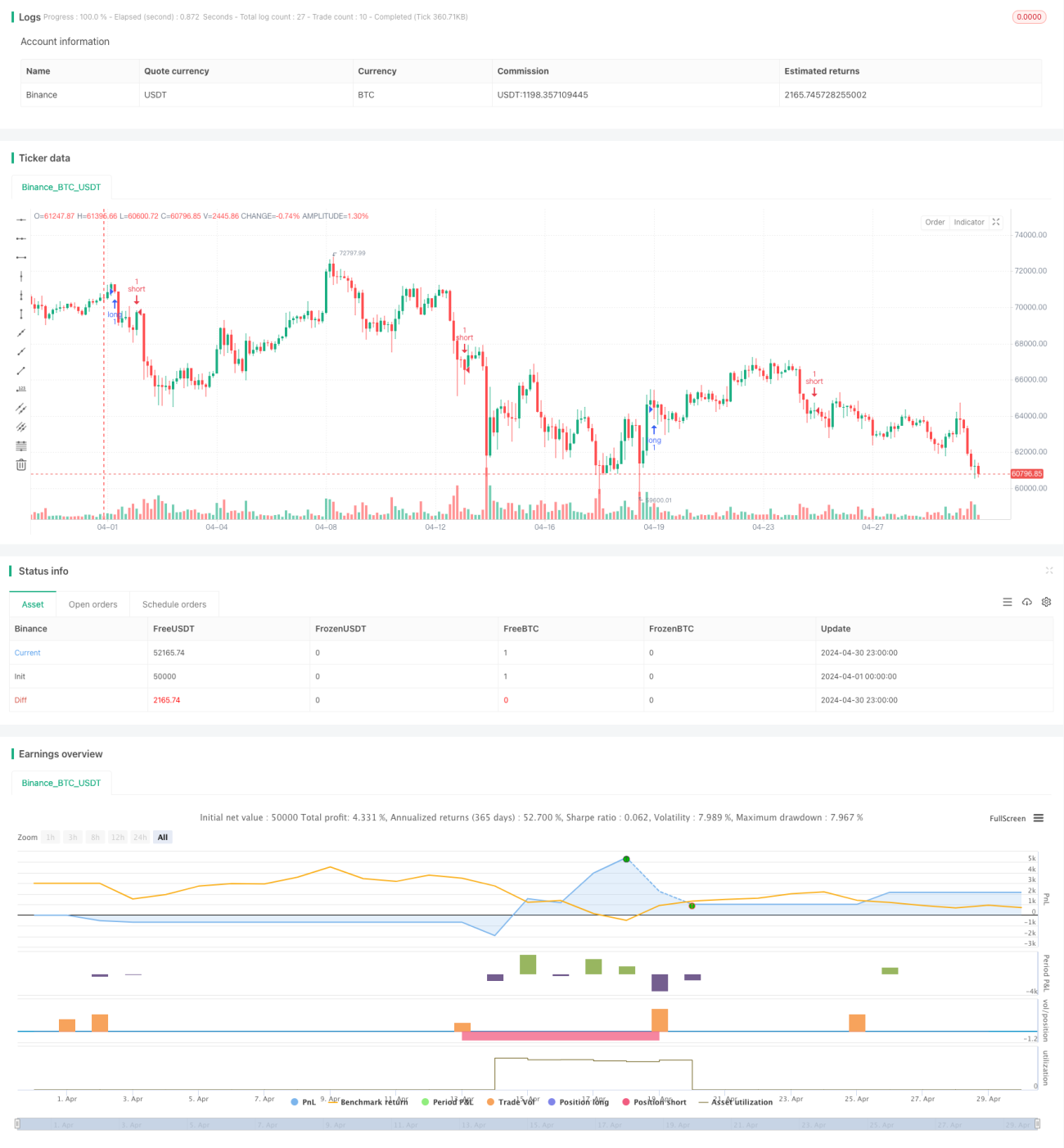

Overview

This strategy uses 15-minute chart data and combines multiple technical indicators such as Bollinger Bands (BB), Moving Averages (MA), Moving Average Convergence Divergence (MACD), Relative Strength Index (RSI), Stochastic Oscillator (STOCH), and Volume Weighted Average Price (VWAP) to generate advanced trading signals. When multiple indicators simultaneously give buy or sell signals, the strategy opens long or short positions. Additionally, the strategy sets stop-loss and take-profit levels to control risk and lock in profits.

Strategy Principles

- Use 15-minute chart data to obtain closing prices.

- Calculate the upper and lower Bollinger Bands to determine if the price is overbought or oversold.

- Calculate fast and slow moving averages to determine trend direction.

- Calculate the MACD line and signal line of the MACD indicator to determine momentum direction.

- Calculate the RSI indicator to determine if the price is overbought or oversold.

- Calculate the %K and %D lines of the Stochastic Oscillator to determine if the price is overbought or oversold.

- Calculate the VWAP indicator to determine the price position relative to the volume-weighted average price.

- Generate a buy signal when the fast moving average crosses above the slow moving average, the MACD line is greater than the signal line, RSI is above 50, the closing price is above VWAP, and the %K line is above the %D line.

- Generate a sell signal when the fast moving average crosses below the slow moving average, the MACD line is less than the signal line, RSI is below 50, the closing price is below VWAP, and the %K line is below the %D line.

- When a buy signal appears, open a long position and set stop-loss and take-profit levels.

- When a sell signal appears, open a short position and set stop-loss and take-profit levels.

Advantage Analysis

- Integrates multiple technical indicators to improve the reliability of trading signals.

- Uses 15-minute chart data to capture short-term trends and fluctuations.

- Sets stop-loss and take-profit levels to effectively control risk and lock in profits.

- Clear and easy-to-understand strategy logic.

Risk Analysis

- In a sideways market, frequent trading signals may lead to overtrading and commission losses.

- The setting of stop-loss and take-profit levels needs to be adjusted according to market conditions; inappropriate settings may lead to losses.

- The strategy relies on historical data and may not react promptly to sudden events and market abnormalities.

Optimization Directions

- Consider introducing other technical indicators, such as Bollinger Band Width and ADX, to further improve the reliability of trading signals.

- Optimize the setting of stop-loss and take-profit levels, such as using dynamic stop-loss and take-profit or adaptively adjusting based on market volatility.

- Incorporate fundamental analysis, such as economic data and policy changes, to filter and optimize trading signals.

Summary

This strategy generates advanced trading signals on a 15-minute chart by comprehensively applying multiple technical indicators and sets stop-loss and take-profit levels to control risk. The strategy logic is clear and easy to implement, but in practical application, it is necessary to pay attention to risks such as overtrading, stop-loss and take-profit settings, and response to sudden events. In the future, we can consider introducing other indicators, optimizing stop-loss and take-profit settings, and combining fundamental analysis to further improve the strategy's reliability and profit potential.

- 1