Keltner Channels EMA ATR Strategy

Overview

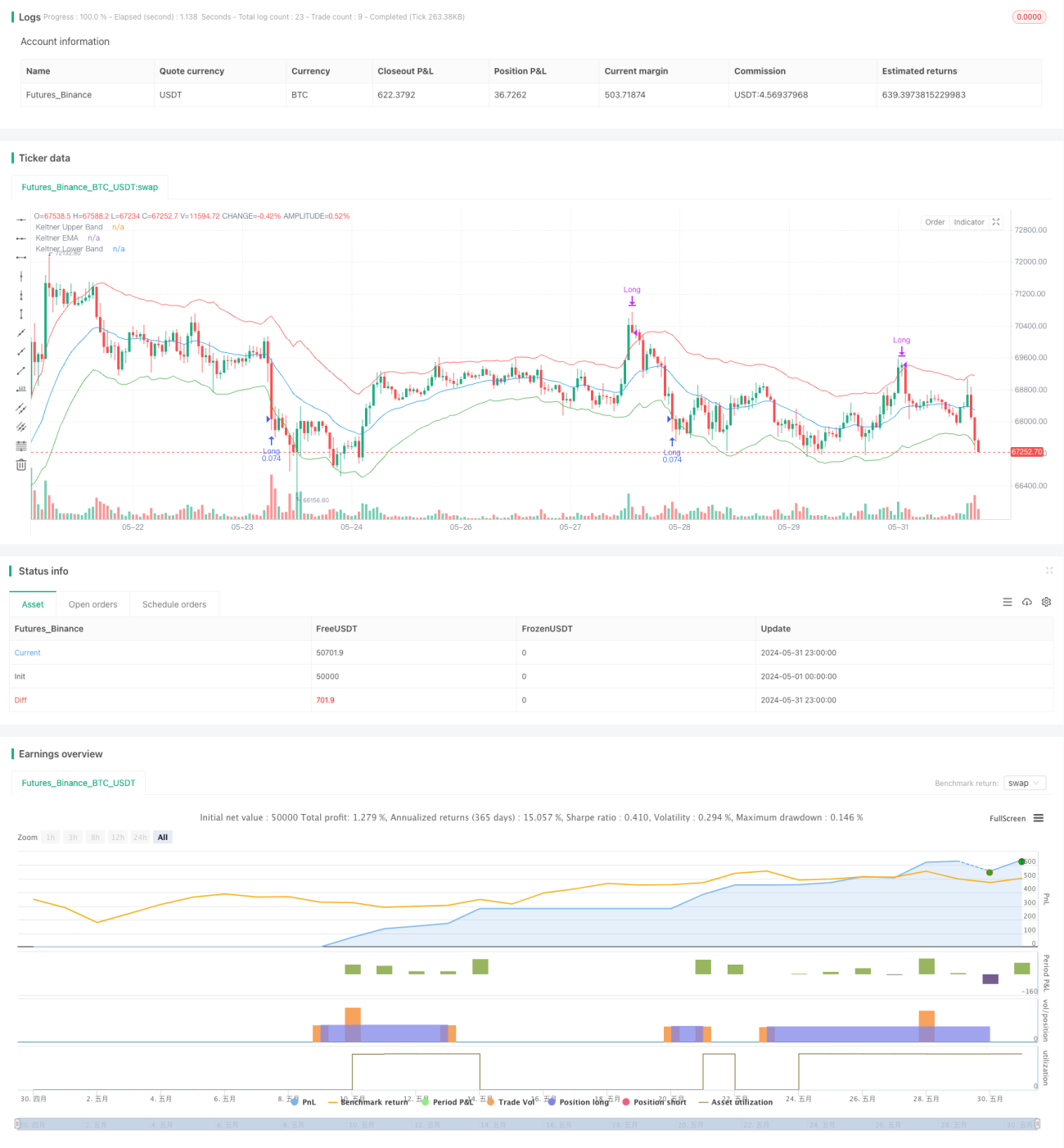

This strategy is based on the Keltner Channels indicator, which uses the Exponential Moving Average (EMA) and Average True Range (ATR) to construct upper and lower channels. When the price breaks below the lower channel, it enters a long position, and when the price breaks above the upper channel, it closes the position. This strategy attempts to capture the price volatility range and takes profit when the price breaks above the upper channel.

Strategy Principles

- Calculate the EMA of a specified period as the middle line of the Keltner Channels.

- Calculate the ATR of a specified period, then multiply it by a factor to serve as the upper and lower channels.

- When the closing price falls below the lower channel, enter a long position and record the entry price.

- When the opening price breaks above the upper channel, close the position.

- If already in a position and the opening price is higher than the upper channel, close the long position.

Strategy Advantages

- Adaptability to price volatility. Since Keltner Channels use ATR to construct the upper and lower channels, and ATR measures price volatility, the channel width will increase accordingly when volatility is high, effectively reducing the cost of frequent trading.

- Clear logic, simplicity, and easy to understand and implement. The indicators used in this strategy are simple, and the core logic is relatively easy to grasp.

- Certain trend-following capability. In an uptrend, this strategy can hold a long position until the price breaks above the upper channel.

Strategy Risks

- Lack of explicit stop-loss mechanism. This strategy does not set a stop-loss after entering a position, which may lead to a large drawdown in adverse market conditions.

- Rough definition of breakout signals. Using only the closing price falling below the lower channel and the opening price breaking above the upper channel as entry and exit signals may produce some misjudgments, leading to losing trades.

- The choice of strategy parameters has a significant impact on the results. The selection of EMA and ATR periods and the setting of the ATR multiple will affect the strategy performance, but the strategy does not provide a clear parameter optimization method.

Strategy Optimization Directions

- Introduce an explicit stop-loss mechanism. Consider setting a stop-loss at a fixed number of points or percentage when entering a position to control the maximum loss of a single trade.

- Optimize the judgment conditions of signals. Consider using more price information to confirm the breakout, such as requiring the closing price to be below the lower channel for several consecutive candles before entering a position to avoid false breakouts.

- Perform parameter optimization. Use methods such as genetic algorithms to optimize the periods of EMA and ATR and the ATR multiple to find the parameter combination that is more suitable for the current market.

- Add filtering conditions. Consider adding some filtering signals, such as only entering a position when ADX is above a certain threshold or using the MA bullish crossover as a trend filter.

Summary

This strategy is based on the Keltner Channels indicator and conducts trades based on the logic of price breaking above or below the channels. Its advantages are simple and clear logic and strong adaptability. Its disadvantages are the lack of stop-loss and poor signal quality. In the future, the strategy can be improved by introducing stop-loss, optimizing signals, parameter optimization, and adding filtering conditions.

/*backtest

start: 2024-05-01 00:00:00

end: 2024-05-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © satrusskumar

//@version=5- 1