Bollinger Bands Momentum Crossover Strategy

Overview

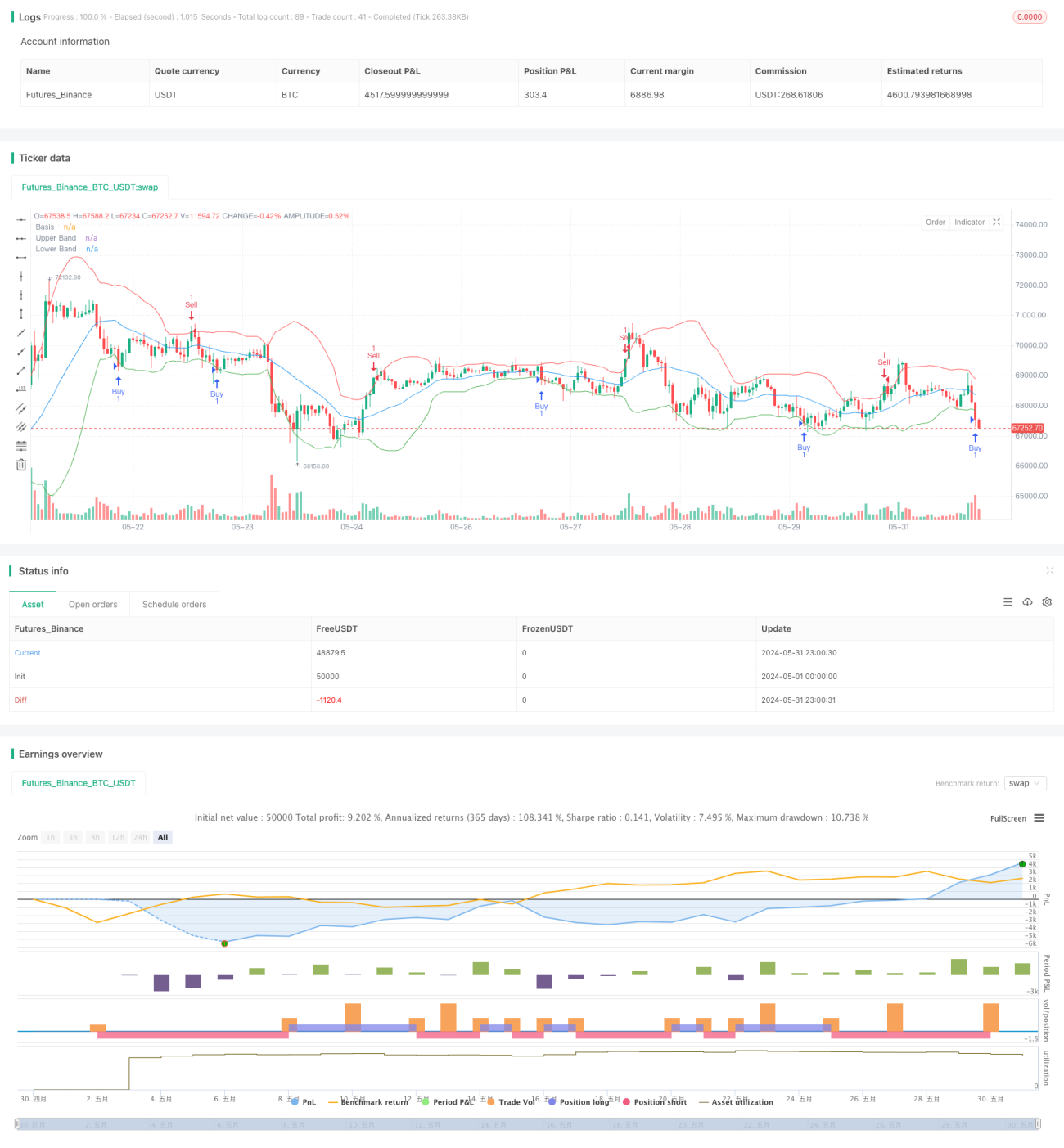

The Bollinger Bands Momentum Crossover Strategy is a technical analysis-based trading method that combines the Bollinger Bands indicator with price momentum concepts. This strategy primarily uses the crossover of price with the upper and lower Bollinger Bands to generate buy and sell signals, aiming to capture overbought and oversold market opportunities. By observing whether the price breaks through the upper or lower bands of the Bollinger Bands, traders can identify potential reversal points and profit from market fluctuations.

Strategy Principles

The core principle of this strategy is to use Bollinger Bands to measure market volatility and price deviation. Bollinger Bands consist of three lines: the middle band (simple moving average), the upper band (middle band plus a multiple of standard deviation), and the lower band (middle band minus a multiple of standard deviation). The specific logic of the strategy is as follows:

- Calculate Bollinger Bands: Use a 20-period simple moving average as the middle band, with upper and lower bands 2 standard deviations away from the middle band.

- Buy signal: When the closing price is below the lower band, the market is considered potentially oversold, triggering a buy signal.

- Sell signal: When the closing price is above the upper band, the market is considered potentially overbought, triggering a sell signal.

- Position closing logic: When holding a long position, if a sell signal appears, close the long position; when holding a short position, if a buy signal appears, close the short position.

The strategy uses variables in_long and in_short to track the current position status, ensuring that positions are not repeatedly opened and are closed at appropriate times.

Strategy Advantages

-

Combination of trend following and reversal: This strategy can capture both trend continuation (when price moves near the upper or lower bands) and potential reversals (when price breaks through the Bollinger Bands).

-

Strong adaptability: Bollinger Bands automatically adjust their width according to market volatility, allowing the strategy to adapt to different market environments.

-

Risk control: By opening positions when the price breaks through the Bollinger Bands, the strategy controls entry risk to some extent.

-

Clear entry and exit signals: The strategy provides clear buy and sell signals, reducing the impact of subjective judgment.

-

Visualization support: The strategy plots Bollinger Bands on the chart, allowing traders to visually analyze market conditions.

Strategy Risks

-

False breakout risk: Prices may briefly break through the Bollinger Bands and then return, leading to false signals.

-

Poor performance in trending markets: In strongly trending markets, prices may run outside the Bollinger Bands for extended periods, resulting in frequent trading and potential losses.

-

Lag: Due to the use of moving averages, the strategy may react slowly to rapid market changes.

-

Parameter sensitivity: The period and standard deviation multiplier of the Bollinger Bands significantly impact strategy performance and require careful optimization.

-

Lack of stop-loss mechanism: The current strategy does not have explicit stop-loss settings, which may lead to significant losses during extreme market volatility.

Strategy Optimization Directions

-

Introduce additional confirmation indicators: Combine other technical indicators (such as RSI or MACD) to filter trading signals and improve accuracy.

-

Dynamic parameter adjustment: Automatically adjust the Bollinger Bands period and standard deviation multiplier based on market volatility to adapt to different market environments.

-

Add stop-loss and take-profit mechanisms: Set stop-loss and take-profit levels based on ATR or fixed points to control risk and lock in profits.

-

Optimize entry timing: Consider entering positions when the price retests the Bollinger Bands instead of entering directly on breakouts to reduce false breakout risk.

-

Incorporate volume analysis: Combine volume indicators to help confirm the validity of breakouts and improve trade success rates.

-

Time filtering: Add time filtering conditions to avoid trading during highly volatile or low liquidity periods.

-

Consider market conditions: Use Bollinger Band width or other indicators to determine whether the market is in a trending or ranging state, and adopt different trading strategies accordingly.

Conclusion

The Bollinger Bands Momentum Crossover Strategy is a trading method that combines mean reversion and trend-following concepts. By leveraging the relationship between price and Bollinger Bands, this strategy aims to capture market overbought and oversold opportunities and potential reversal points. While the strategy has advantages such as strong adaptability and clear signals, it also faces risks like false breakouts and poor performance in trending markets. To improve the strategy's robustness and profitability, consider introducing additional confirmation indicators, optimizing parameter settings, and adding risk management mechanisms. In practical application, traders need to continuously optimize and backtest the strategy based on specific market environments and individual risk preferences to achieve the best trading results.

- 1