Machine Learning Inspired Dual Moving Average RSI Trading Strategy

Overview

This trading strategy is a quantitative trading system that combines moving averages and the Relative Strength Index (RSI). The strategy uses the crossover of fast and slow moving averages to identify potential trend changes, while utilizing RSI to confirm overbought and oversold market conditions. This approach aims to capture market momentum while reducing false signals through RSI filtering. The strategy design is inspired by concepts of feature combination and signal filtering in machine learning, although it does not use complex machine learning algorithms itself.

Strategy Principles

The core principles of this strategy are based on the following key components:

-

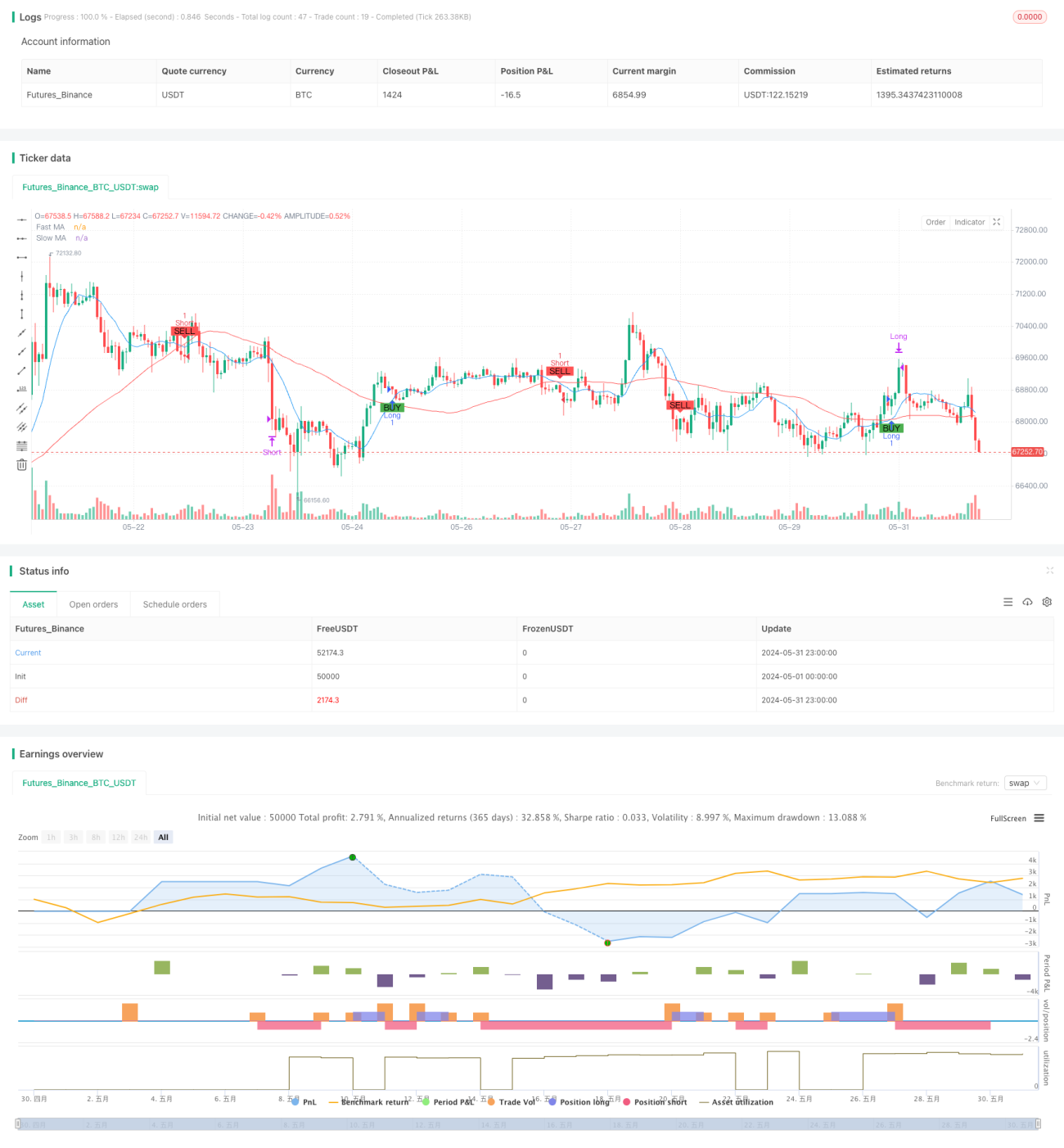

Dual Moving Average System: Uses fast (10-period) and slow (50-period) Simple Moving Averages (SMA) to identify trends. A potential long signal is generated when the fast MA crosses above the slow MA, and a potential short signal when the fast MA crosses below the slow MA.

-

RSI Filtering: A 14-period RSI is used to confirm market conditions. Long entries are allowed when RSI is below 70, and short entries when RSI is above 30, helping to avoid entering overstretched markets.

-

Entry Logic: The strategy only generates trading signals when both the MA crossover and RSI conditions are met simultaneously. This double confirmation mechanism aims to improve signal reliability.

-

Exit Logic: The strategy closes respective long or short positions when RSI reaches extreme values (above 70 or below 30), helping to secure profits when the market might be reversing.

Strategy Advantages

-

Trend Following and Momentum Combination: By combining moving averages and RSI, the strategy can capture long-term trends while identifying short-term overbought and oversold opportunities.

-

Signal Filtering: Using RSI as a secondary confirmation helps reduce false breakouts and improves trade quality.

-

Flexibility: Strategy parameters (such as MA periods and RSI thresholds) can be optimized for different markets and timeframes.

-

Risk Management: The strategy incorporates a built-in risk control mechanism by automatically closing positions when RSI reaches extreme values.

-

Visualization: The strategy marks buy and sell signals on the chart, facilitating intuitive understanding and backtesting analysis for traders.

Strategy Risks

-

Lag: Moving averages are inherently lagging indicators, which may lead to less timely entries and exits near trend reversal points.

-

Performance in Ranging Markets: In sideways or choppy markets, frequent MA crossovers may result in excessive false signals and trading costs.

-

Parameter Sensitivity: Strategy performance may be sensitive to the chosen MA periods and RSI thresholds, with different parameters potentially performing differently across various market environments.

-

Lack of Stop-Loss Mechanism: The current strategy does not have explicit stop-loss rules, which may lead to significant losses in extreme market conditions.

-

Over-reliance on Technical Indicators: The strategy is entirely based on technical indicators, ignoring other important factors such as fundamentals and market sentiment.

Strategy Optimization Directions

-

Adaptive Parameters: Introduce adaptive mechanisms to dynamically adjust MA periods and RSI thresholds based on market volatility, adapting to different market environments.

-

Add Trend Strength Filter: Consider adding ADX (Average Directional Index) to measure trend strength, trading only in strong trend markets to reduce false signals in ranging markets.

-

Introduce Stop-Loss Mechanism: Implement dynamic stop-losses based on ATR (Average True Range) or use fixed percentage stop-losses for better risk control.

-

Optimize Exit Strategy: In addition to RSI extreme value exits, consider adding trailing stops or trend reversal-based exit signals to better secure profits.

-

Add Volume Filter: On top of entry signals, add volume confirmation, executing trades only when accompanied by increased volume to improve signal reliability.

-

Multi-Timeframe Analysis: Incorporate longer-term trend analysis, trading only in the direction of the main trend to improve win rates.

-

Machine Learning Optimization: Use machine learning algorithms such as genetic algorithms or Bayesian optimization to find optimal parameter combinations, enhancing strategy stability and adaptability.

Conclusion

This Machine Learning Inspired Dual Moving Average RSI Trading Strategy provides a framework that combines trend following and momentum trading. By identifying trends through moving averages and optimizing signals with RSI, the strategy aims to capture major market movements. While the strategy design is relatively simple, it provides a good foundation for further optimization and expansion. Traders can adjust parameters according to their risk preferences and market views, or add additional filtering conditions to improve strategy performance. However, in practical application, thorough backtesting and forward testing are still necessary, combined with appropriate money management strategies, to ensure robust performance in real market environments.

- 1