Multi-Factor Dynamic Adaptive Trend Following Strategy

Overview

The Multi-Factor Dynamic Adaptive Trend Following Strategy is a systematic trading approach that combines multiple technical indicators. This strategy utilizes the Moving Average Convergence Divergence (MACD), Relative Strength Index (RSI), Average True Range (ATR), and Simple Moving Averages (SMA) to capture market trends and optimize entry and exit points. By employing multiple indicator confirmations, the strategy aims to increase trade success rates while implementing dynamic stop-loss and take-profit methods to adapt to various market environments, balancing risk management and profit maximization.

Strategy Principles

The core principle of this strategy is to identify and confirm market trends through the synergistic use of multiple technical indicators. Specifically:

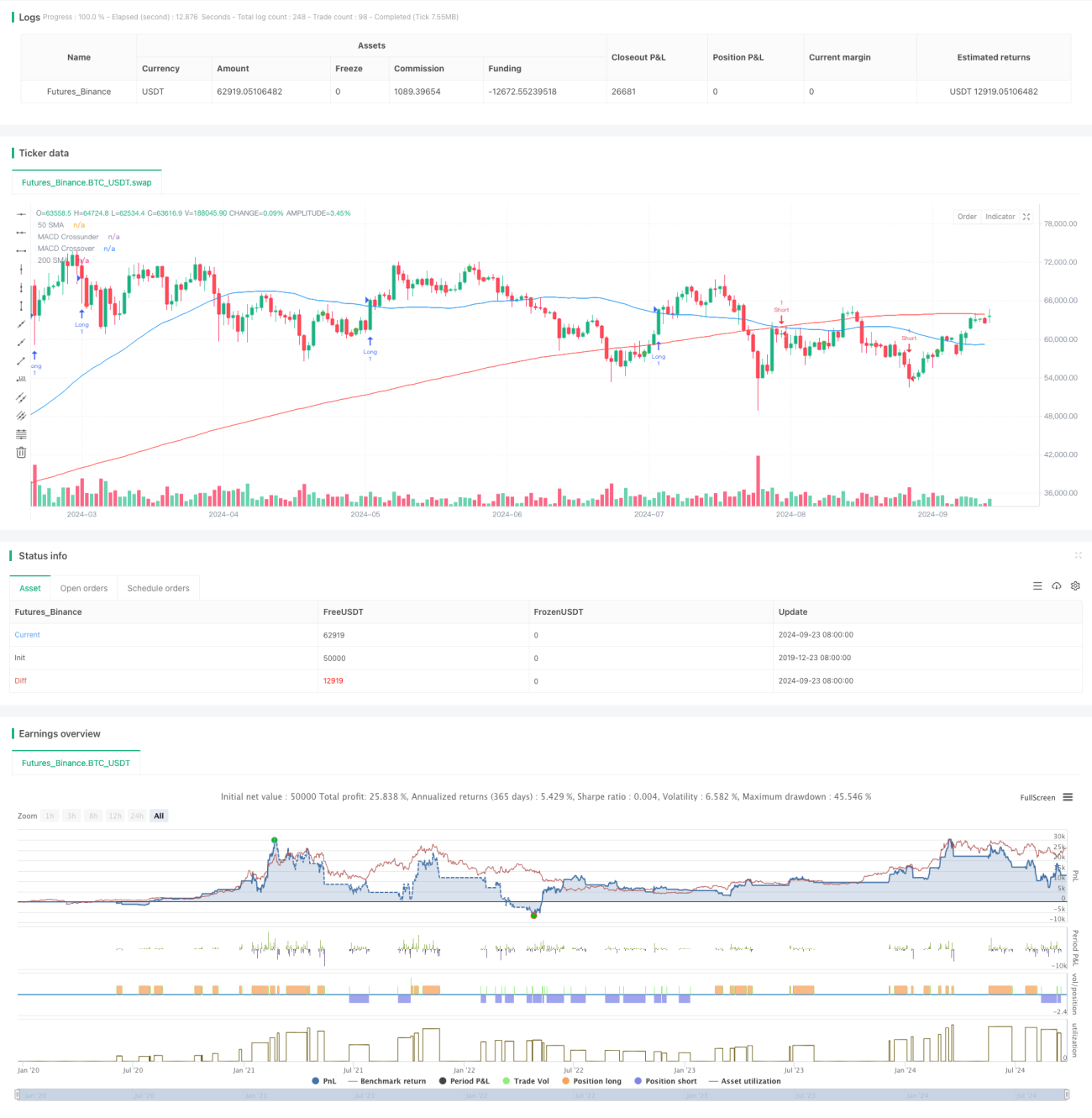

- MACD crossovers are used to capture potential trend reversal points.

- RSI confirms price momentum, avoiding entries in overbought or oversold conditions.

- The relationship between 50-day and 200-day SMAs determines the overall market trend.

- ATR is applied to dynamically set stop-loss and take-profit levels, adapting to market volatility.

The strategy initiates a long position when the MACD line crosses above the signal line, RSI is below 70, price is above the 50-day SMA, and the 50-day SMA is above the 200-day SMA. Opposite conditions trigger short signals. The strategy employs a 2x ATR stop-loss and a 3x ATR take-profit, ensuring a 1:1.5 risk-reward ratio.

Strategy Advantages

- Multi-dimensional confirmation: By combining multiple indicators, the strategy provides a more comprehensive market assessment, reducing the impact of false signals.

- Dynamic risk management: Utilizing ATR to adjust stop-loss and take-profit levels allows the strategy to adapt to varying market volatility conditions.

- Trend following and momentum integration: The strategy considers both long-term trends (via SMAs) and short-term momentum (via MACD and RSI), helping to capture strong, persistent trends.

- Systematic decision-making: Clear entry and exit rules reduce subjective judgment, promoting trading discipline.

- Flexibility: Strategy parameters can be adjusted for different markets and trading instruments, offering high adaptability.

Strategy Risks

- Underperformance in ranging markets: In the absence of clear trends, the strategy may generate frequent false signals, increasing transaction costs.

- Lag effect: Due to the use of lagging indicators like moving averages, the strategy may miss opportunities at the beginning of trends.

- Over-reliance on technical indicators: Neglecting fundamental factors may lead to incorrect decisions during significant events or news releases.

- Parameter sensitivity: Strategy performance may be sensitive to indicator parameter settings, requiring periodic optimization to adapt to market changes.

- Drawdown risk: The 2x ATR stop-loss setting may be insufficient to effectively control risk during sharp market reversals.

Strategy Optimization Directions

- Implement volatility filtering: Consider suspending trades in low volatility environments to reduce false signals in ranging markets.

- Incorporate fundamental factors: Integrate economic data releases and company earnings reports to enhance strategy comprehensiveness.

- Optimize indicator combination: Experiment with additional indicators like Bollinger Bands or Ichimoku Cloud to improve strategy robustness.

- Develop adaptive parameters: Create machine learning models to dynamically adjust indicator parameters based on market conditions.

- Refine market state classification: Distinguish between different market environments (e.g., trending, ranging, high volatility) and adjust strategy parameters accordingly.

- Introduce multi-timeframe analysis: Combine signals from multiple time periods to improve trading decision accuracy.

Summary

The Multi-Factor Dynamic Adaptive Trend Following Strategy offers traders a systematic, quantifiable trading method by integrating multiple technical indicators. This strategy excels in clearly trending markets, effectively capturing medium to long-term price movements. Its dynamic risk management mechanism and multi-dimensional signal confirmation process help enhance trading stability and reliability. However, the strategy also has limitations, such as performance issues in ranging markets and over-reliance on technical indicators. Through continuous optimization and the introduction of more diverse analytical dimensions, this strategy has the potential to evolve into a more comprehensive and robust trading system. Traders employing this strategy should conduct appropriate parameter adjustments and backtesting based on specific market characteristics and individual risk preferences to achieve optimal trading results.

- 1