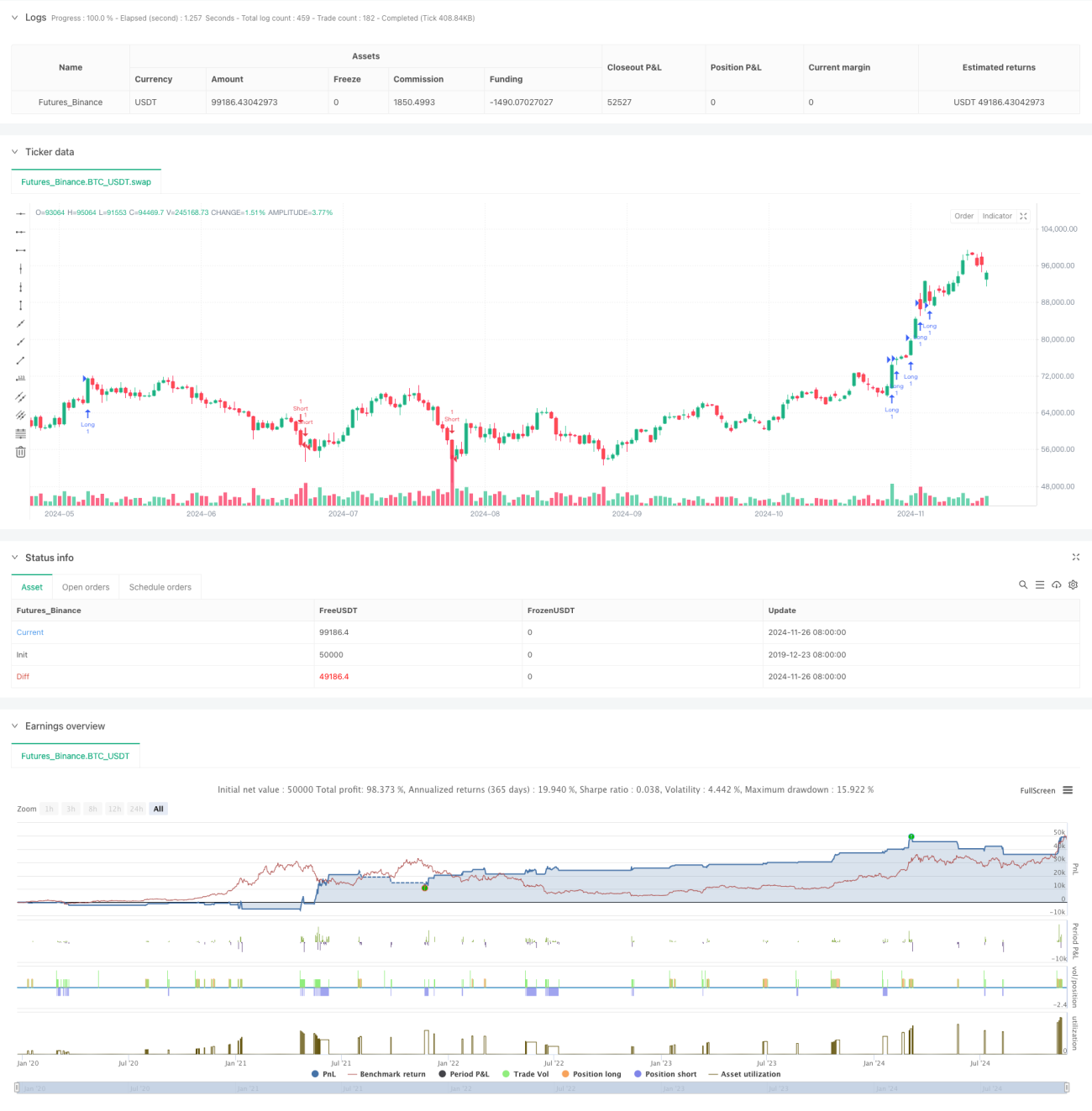

Overview

This strategy is a quantitative trading system based on Elder's Force Index (EFI), combining standard deviation and moving averages for signal generation, while using ATR for dynamic stop-loss and take-profit positioning. The strategy calculates fast and slow EFI indicators, normalizes them using standard deviation, and generates trading signals through crossover analysis, creating a complete trading system. It employs dynamic stop-loss and trailing take-profit mechanisms to effectively control risks while pursuing higher returns.

Strategy Principle

The strategy is built on several core elements:

- Uses two different periods (13 and 50) to calculate fast and slow force indices

- Normalizes both EFI periods using standard deviation to make signals more statistically significant

- Generates long signals when both fast and slow EFI simultaneously break above the standard deviation threshold

- Generates short signals when both fast and slow EFI simultaneously break below the standard deviation threshold

- Uses ATR for dynamic stop-loss positioning that adjusts with price movement

- Implements ATR-based trailing take-profit mechanism to protect and grow profits

Strategy Advantages

- Signal system combines momentum and volatility characteristics, improving trading reliability

- Standard deviation normalization makes signals statistically significant, reducing false signals

- Dynamic stop-loss mechanism effectively controls risk and prevents large drawdowns

- Trailing take-profit mechanism both protects and allows profits to grow

- Clear strategy logic with adjustable parameters, suitable for optimization across different markets

Strategy Risks

- May generate false signals in highly volatile markets, requiring additional filtering mechanisms

- Sensitive parameter selection might lead to overtrading, increasing transaction costs

- Potential lag at trend reversal points, affecting strategy performance

- Improper stop-loss positioning might result in premature exits or excessive losses

- Need to consider the impact of transaction costs on strategy returns

Optimization Directions

- Add market condition assessment mechanism to use different parameters in different market states

- Introduce volume filters to improve signal reliability

- Optimize stop-loss and take-profit parameters to better adapt to market volatility

- Add trend filters to avoid frequent trading in ranging markets

- Consider adding time filters to avoid trading during unfavorable periods

Summary

The strategy builds a complete trading system by combining EFI indicators, standard deviation, and ATR. Its strengths lie in high signal reliability and reasonable risk control, though optimization for different market environments is still needed. The strategy's stability and profitability can be further improved by adding market condition assessment, volume filtering, and other mechanisms. Overall, it provides a solid quantitative trading framework with practical value.

- 1