1

关注

1802

关注者

概述

这是一个结合了UT Bot和50周期指数移动平均线(EMA)的趋势追踪交易策略。该策略主要在1分钟时间周期进行短线交易,同时使用5分钟时间周期的趋势线作为方向过滤。策略采用ATR指标动态计算止损位置,并设置了双重止盈目标来优化收益。

策略原理

策略的核心逻辑基于以下几个关键组件:

- 使用UT Bot计算动态支撑阻力位

- 利用5分钟周期的50周期EMA判断总体趋势方向

- 结合21周期EMA和UT Bot信号确定具体入场点

- 通过ATR倍数设置动态跟踪止损

- 设置0.5%和1%两个止盈目标,分别平仓50%仓位

当价格突破UT Bot计算的支撑/阻力位,并且21周期EMA与UT Bot发生交叉时,如果价格位于5分钟50周期EMA的正确方向,则触发交易信号。

策略优势

- 多重时间周期结合提高了交易可靠性

- 动态ATR止损可以根据市场波动自适应调整

- 双重止盈目标平衡了收益和胜率

- 使用Heikin Ashi蜡烛图可以过滤部分假突破

- 支持灵活的交易方向选择(可以只做多、只做空或者双向交易)

策略风险

- 短周期交易可能面临较高的点差和手续费成本

- 在横盘整理市场中可能产生频繁的假信号

- 多重条件的限制可能导致错过一些潜在的交易机会

- ATR参数的设置需要针对不同市场进行优化

策略优化方向

- 可以添加成交量指标作为辅助确认

- 考虑引入更多的市场情绪指标

- 针对不同市场波动特征开发自适应参数

- 增加交易时间段的过滤

- 开发更智能的仓位管理系统

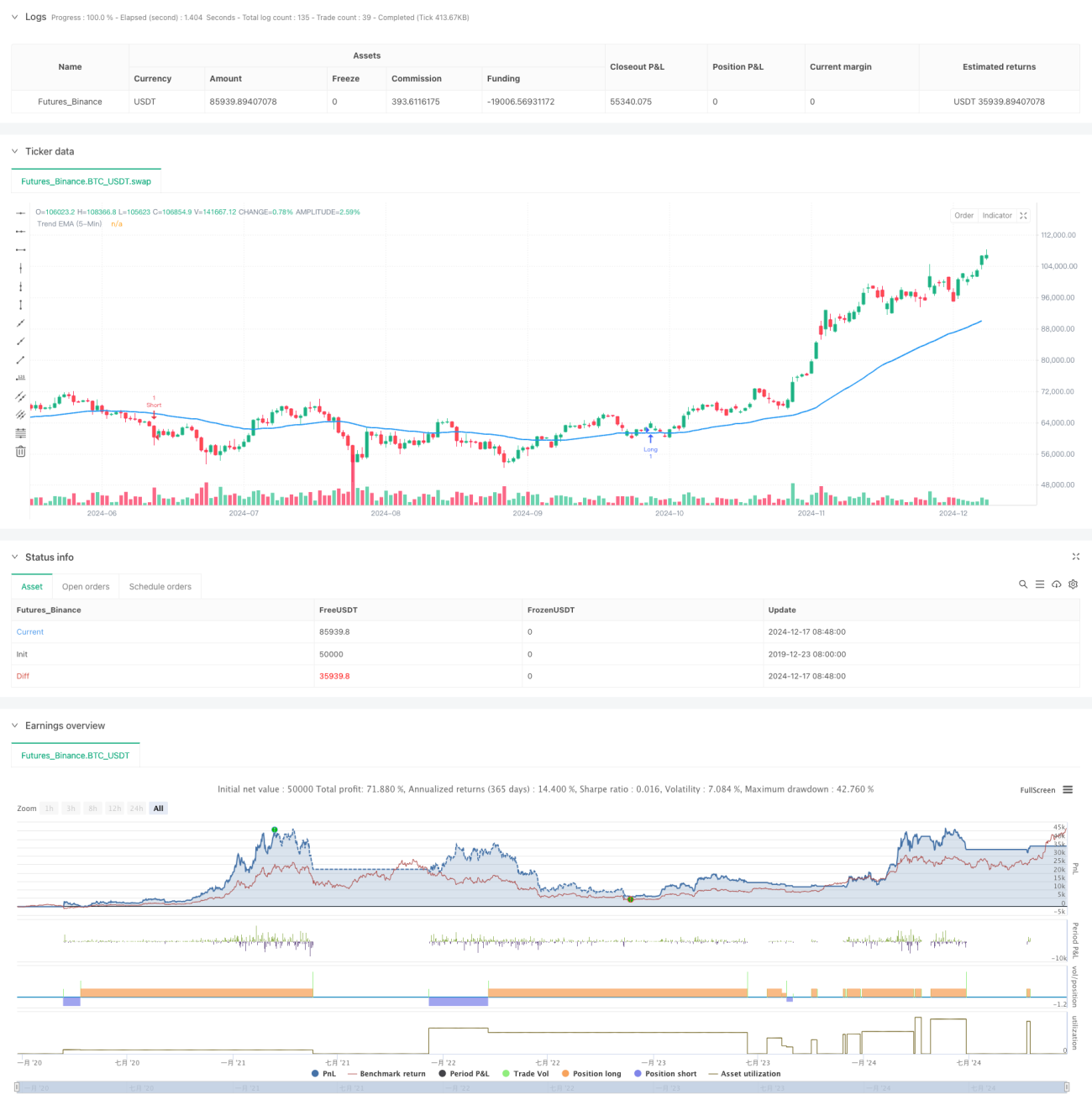

总结

该策略通过多重技术指标和时间周期的结合,构建了一个完整的交易系统。它不仅包含了明确的入场出场条件,还提供了完善的风险管理机制。虽然在实际应用中仍需要根据具体市场情况进行参数优化,但整体框架具有良好的实用性和扩展性。

策略源码

Pine

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//Created by Nasser mahmoodsani' all rights reserved

// E-mail : [email protected]

策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1