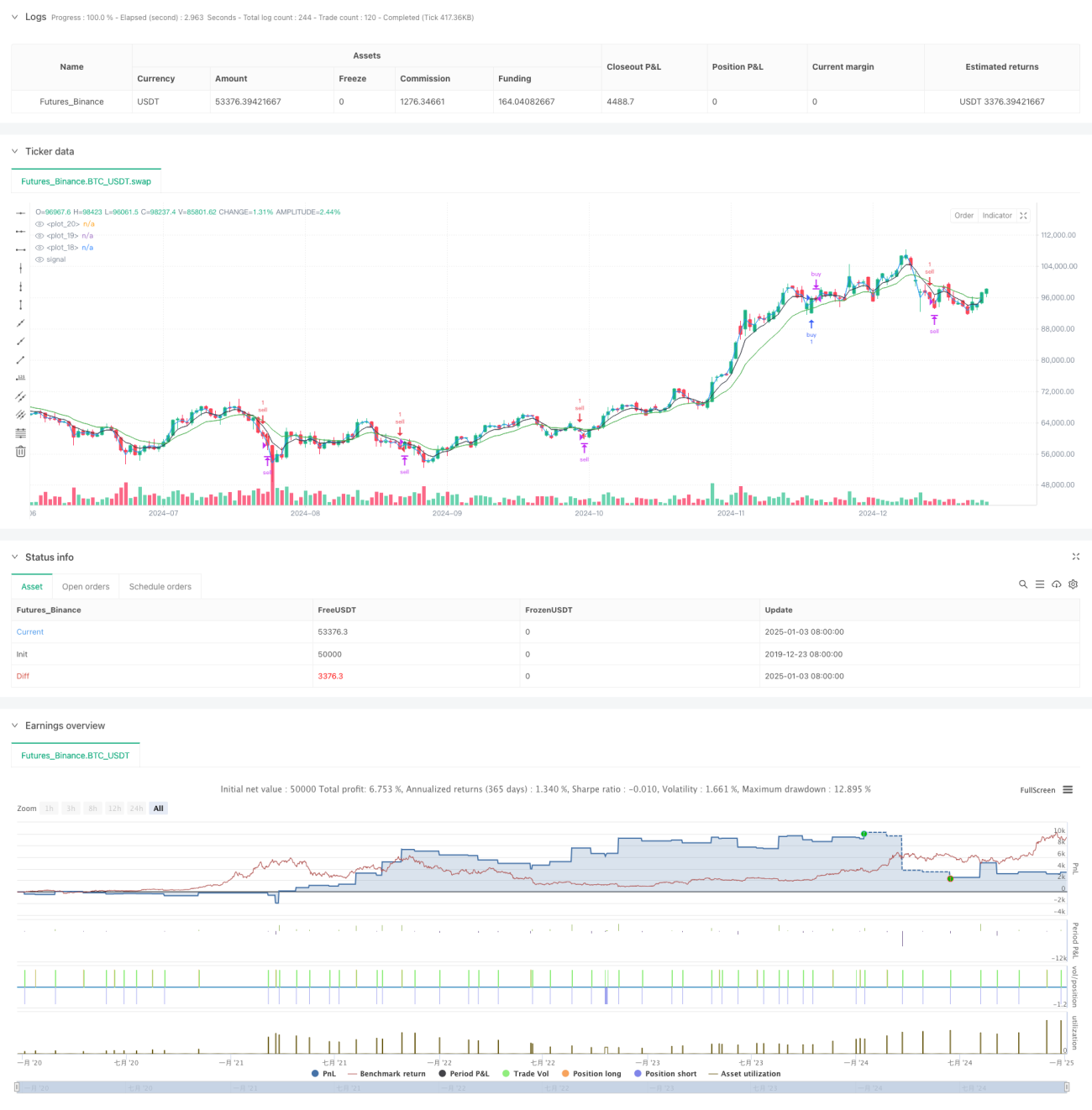

This is a comprehensive momentum trading strategy based on multiple exponential moving average (EMA) crossovers and volume-price indicators. The strategy generates trading signals by combining various indicators including fast and slow EMAs, Volume Weighted Average Price (VWAP), and SuperTrend, while incorporating intraday trading windows and price movement thresholds to control entry and exit points.

Strategy Principles

The strategy utilizes 5-day and 13-day EMAs as primary trend indicators. Long positions are triggered when the fast EMA crosses above the slow EMA with closing price above VWAP, while short positions are triggered when the fast EMA crosses below the slow EMA with closing price below VWAP. The strategy also incorporates the SuperTrend indicator for trend confirmation and stop-loss determination. Different entry conditions are set for different trading days, including price movement relative to the previous day's close and the day's high-low range.

Strategy Advantages

- Multiple technical indicators enhance trading signal reliability

- Differentiated entry conditions for different trading days better adapt to market characteristics

- Dynamic profit-taking and stop-loss mechanisms effectively control risk

- Intraday trading window restrictions avoid high volatility periods

- Previous high-low points and price movement constraints reduce the risk of chasing highs and lows

Strategy Risks

- False signals may occur in rapidly fluctuating markets

- Potential lag during initial trend reversals

- Parameter optimization may face overfitting risks

- Trading costs may impact strategy returns

- Significant drawdowns possible during highly volatile market periods

Strategy Optimization Directions

- Consider incorporating volume analysis indicators to further confirm trend strength

- Optimize parameters for different trading days to improve strategy adaptability

- Add more market sentiment indicators to enhance predictive accuracy

- Refine profit-taking and stop-loss mechanisms to improve capital efficiency

- Consider adding volatility indicators to optimize position management

Summary

This strategy achieves a combination of trend following and momentum trading through the comprehensive use of multiple technical indicators. The strategy design fully considers market diversity by adopting differentiated trading rules for different trading days. Through strict risk control and flexible profit-taking and stop-loss mechanisms, the strategy demonstrates good practical application value. Future improvements can enhance strategy stability and profitability by introducing additional technical indicators and optimizing parameter settings.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=6

strategy("S1", overlay=true)

fastEMA = ta.ema(close, 5)- 1