Statistical Dual Standard Deviation VWAP Breakout Trading Strategy

Overview

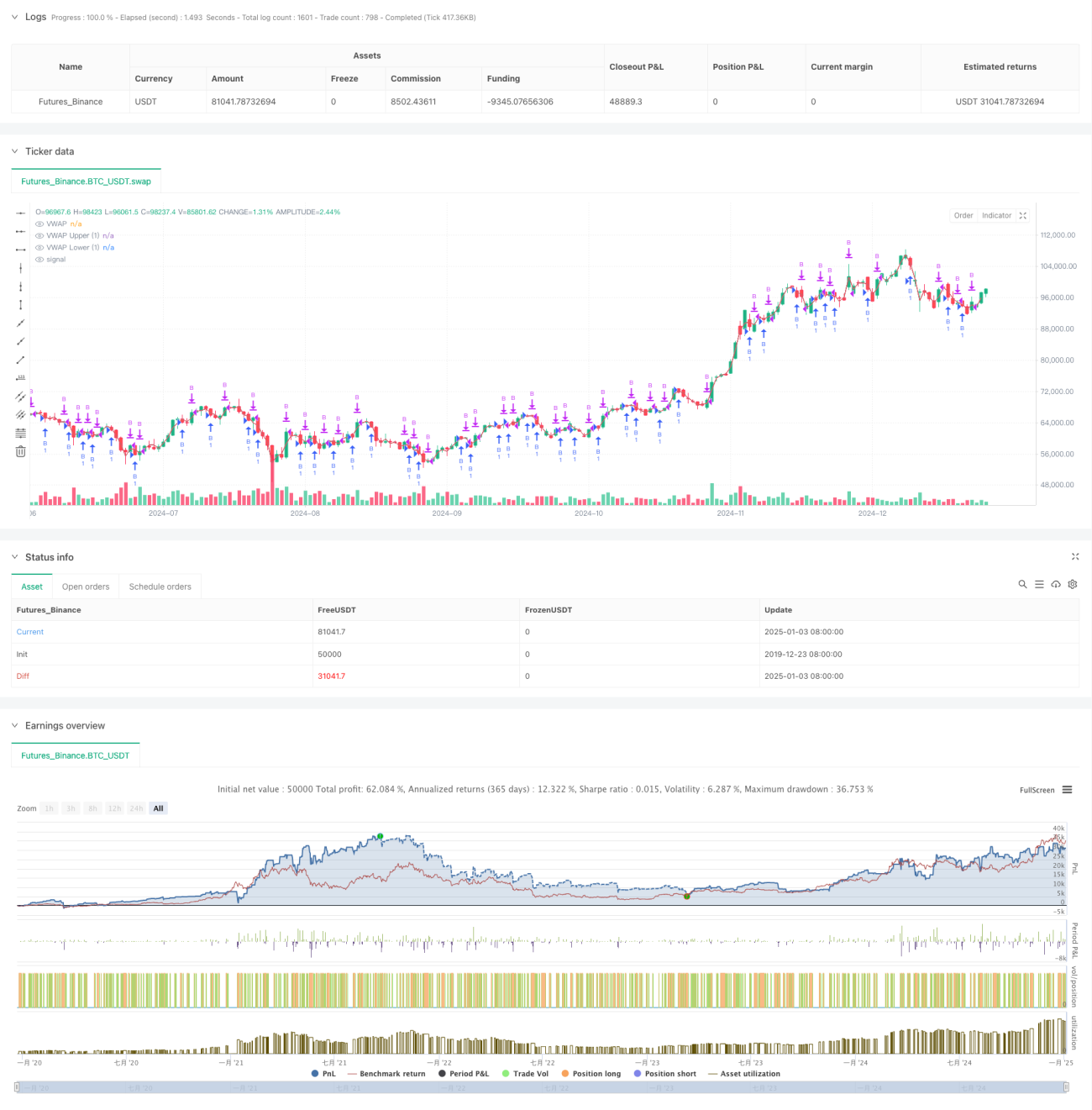

This strategy is a trend breakout system based on VWAP (Volume Weighted Average Price) and standard deviation channels. It constructs a dynamic price range by calculating VWAP and standard deviation bands to capture upward breakout opportunities. The strategy mainly relies on standard deviation band breakthrough signals for trading, with profit targets and order intervals to control risk.

Strategy Principles

- Core Indicator Calculation:

- Calculate VWAP using intraday HL2 prices and volume

- Compute standard deviation based on price volatility

- Set 1.28 times standard deviation upper and lower bands

- Trading Logic:

- Entry condition: price crosses below lower band then rises above it

- Exit condition: reaches preset profit target

- Minimum order interval to avoid frequent trading

Strategy Advantages

- Statistical Foundation

- VWAP-based price center reference

- Volatility measurement using standard deviation

- Dynamic trading range adjustment

- Risk Control

- Fixed profit target setting

- Trading frequency control

- Long-only strategy reduces risk

Strategy Risks

- Market Risks

- False breakouts during high volatility

- Difficulty in accurately timing trend reversals

- Increased losses in downtrend markets

- Parameter Risks

- Sensitivity to standard deviation multiplier settings

- Profit target optimization needed

- Trading interval affects performance

Optimization Directions

- Signal Optimization

- Add trend filter

- Incorporate volume change confirmation

- Include additional technical indicators

- Risk Management Optimization

- Dynamic stop-loss placement

- Position sizing based on volatility

- Enhanced order management system

Summary

This is a quantitative trading strategy combining statistical principles and technical analysis. Through the combination of VWAP and standard deviation bands, it builds a relatively reliable trading system. The core advantages lie in its scientific statistical foundation and comprehensive risk control mechanisms, but continuous optimization of parameters and trading logic is still needed in practical applications.

- 1