Multi-Period Supertrend Dynamic Pyramiding Trading Strategy

Overview

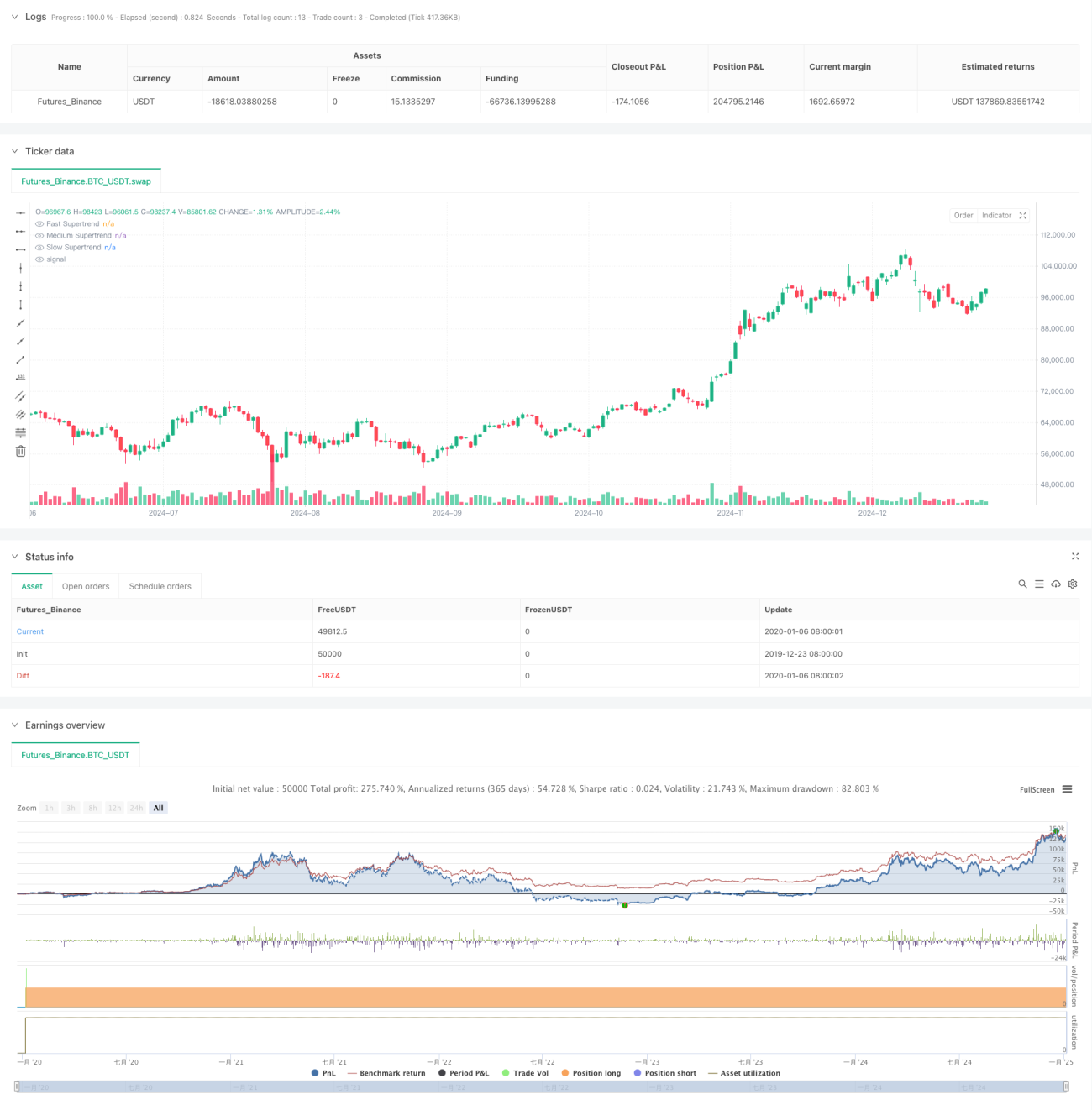

This is a pyramiding trading strategy based on multiple Supertrend indicators. It identifies high-probability trading opportunities using three Supertrend indicators with different periods and multipliers. The strategy employs dynamic pyramiding entries allowing up to three positions, combined with dynamic stop-loss and flexible exit conditions to maximize profits while controlling risks.

Strategy Principles

The strategy utilizes three Supertrend indicators with different parameter settings: fast, medium, and slow. Entry signals are based on the crossovers and trend directions of these indicators, implementing a three-layer pyramiding approach: first entry when fast indicator points down while medium points up and slow points down; second entry through breakout when both fast and medium indicators point down; third entry through breakout when price makes new highs. Exits are managed through multiple mechanisms including dynamic stop-loss, average price stop, and overall trend reversal.

Strategy Advantages

- Multiple confirmation mechanism improves trading accuracy

- Pyramiding approach significantly amplifies profits in trending markets

- Dynamic stop-loss mechanism protects profits while allowing trends to develop

- Flexible exit mechanisms adapt well to different market conditions

- Percentage-based position sizing adapts to different capital sizes

Strategy Risks

- May generate frequent false signals in ranging markets

- Pyramiding can lead to larger drawdowns during sudden trend reversals

- Multiple indicators may result in delayed signals

- Parameter optimization faces overfitting risks

It's recommended to implement strict money management and backtesting to control these risks.

Optimization Directions

- Add market environment filters to dynamically adjust parameters based on volatility

- Optimize entry spacing and position size allocation

- Introduce additional technical indicators to filter false signals

- Develop adaptive parameter mechanisms to adapt to market changes

- Enhance exit mechanisms by adding profit targets and time-based stops

Summary

The strategy captures trending opportunities through multiple Supertrend indicators and pyramiding entries, while controlling risks with dynamic stop-loss and flexible exit mechanisms. Despite certain limitations, with continuous optimization and strict risk control, the strategy shows good practical application value.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('4Vietnamese 3x Supertrend', overlay=true, max_bars_back=1000, initial_capital = 10000000000, slippage = 2, commission_type = strategy.commission.percent, commission_value = 0.013, default_qty_type=strategy.percent_of_equity, default_qty_value = 33.33, pyramiding = 3, margin_long = 0, margin_short = 0)

///////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////- 1