1

关注

1802

关注者

概述

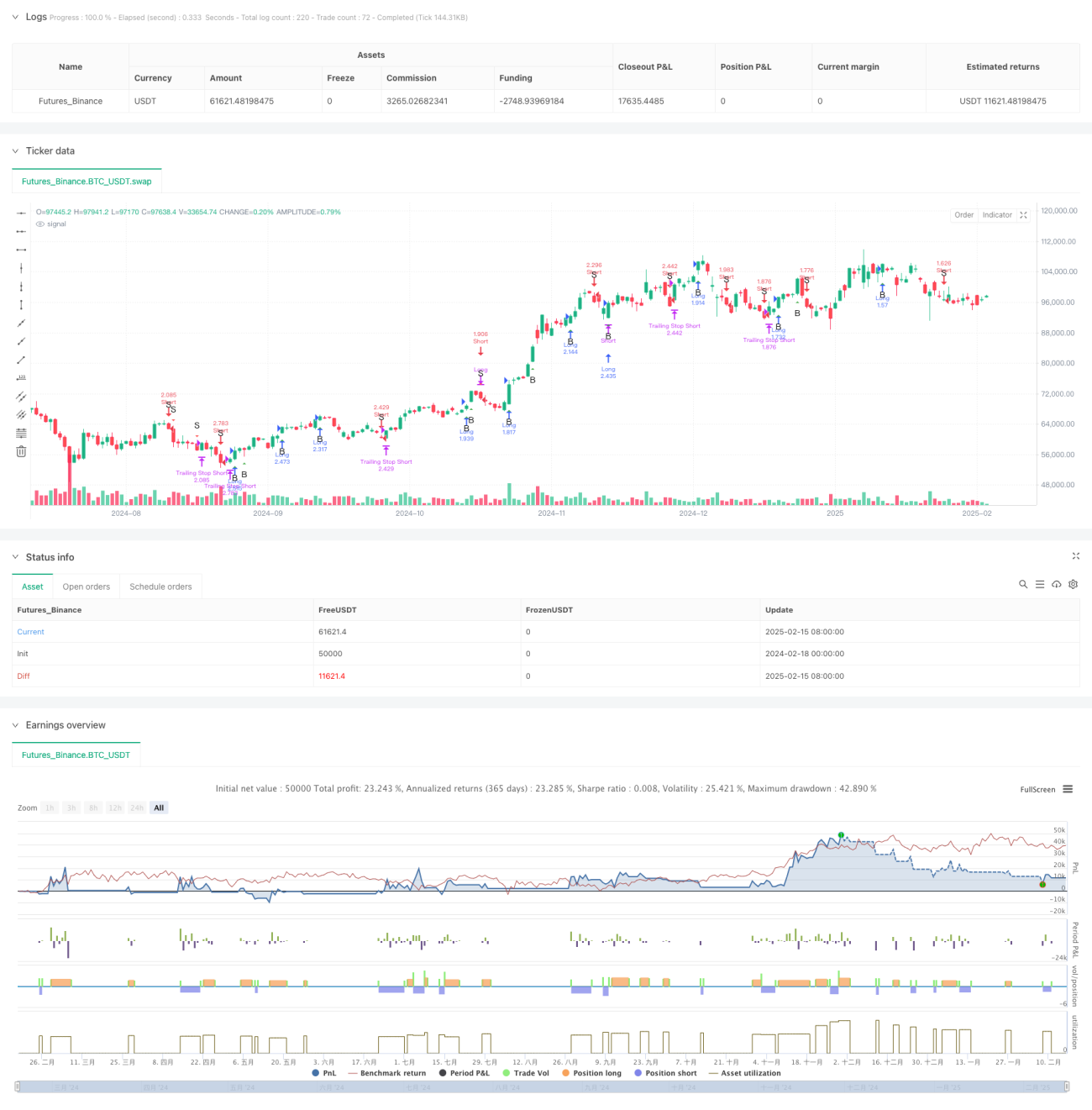

这是一个结合了比尔·威廉姆斯(Bill Williams)三分之一K线分析方法和动态跟踪止损功能的量化交易策略。该策略通过分析当前和前一根K线的结构特征来产生明确的多空信号,并利用可配置的跟踪止损机制来保护持仓,实现了精确的入场/出场和风险管理。

策略原理

策略的核心逻辑基于以下几个关键部分:

- K线三等分计算: 将每根K线的范围(最高价-最低价)分成三等份,得到上层区域和下层区域的边界值。

- K线形态分类: 根据开盘价和收盘价在三等分区域的位置,将K线分为多种类型。例如,当开盘价在下层区域而收盘价在上层区域时,被认为是强势上涨形态。

- 信号生成规则: 通过组合分析当前K线和前一根K线的形态,确定有效的交易信号。例如,当连续两根K线都显示强势特征时,触发做多信号。

- 动态跟踪止损: 在指定的时间周期内,使用前N根K线的最低价(多头)或最高价(空头)作为移动止损点位。

策略优势

- 逻辑清晰性: 策略使用直观的K线结构分析方法,交易规则明确且易于理解。

- 风险管理完善: 通过动态跟踪止损机制,能够在保留足够盈利空间的同时,有效控制回撤风险。

- 适应性强: 策略可以根据不同的市场环境调整跟踪止损参数,具有良好的适应性。

- 自动化程度高: 从信号生成到仓位管理都实现了完全自动化,减少了人为干预。

策略风险

- 震荡市场风险: 在横盘震荡行情下,可能会产生频繁的假突破信号,导致过度交易。

- 跳空风险: 在出现大幅跳空时,跟踪止损可能无法及时触发,造成超预期损失。

- 参数敏感性: 跟踪止损的参数选择对策略表现影响较大,不当的参数设置可能导致过早出场或者保护不足。

策略优化方向

- 增加市场环境过滤: 可以引入趋势指标或波动率指标,在不同市场环境下动态调整策略参数。

- 优化止损机制: 可以考虑结合ATR指标来设置更灵活的止损距离,提高止损的适应性。

- 引入仓位管理: 可以根据信号强度和市场波动性动态调整仓位大小,实现更精细的风险控制。

- 增加出场优化: 可以添加利润目标或者技术指标辅助判断,优化出场时机。

总结

这是一个结构完整、逻辑清晰的量化交易策略,通过组合使用经典的技术分析方法和现代风险管理技术,具有较好的实用性。策略的设计充分考虑了实盘交易的需求,包括信号生成、持仓管理和风险控制等关键环节。通过进一步优化和完善,该策略有望在实际交易中取得更好的表现。

策略源码

Pine

/*backtest

start: 2024-02-18 00:00:00

end: 2025-02-16 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("TrinityBar with Trailing Stop", overlay=true, initial_capital=100000,

default_qty_type=strategy.percent_of_equity, default_qty_value=250)

策略参数

评论

全部评论 (0)

暂无数据

- 1