Delta SMA Historical High/Low Based Trend Capture Strategy

Overview

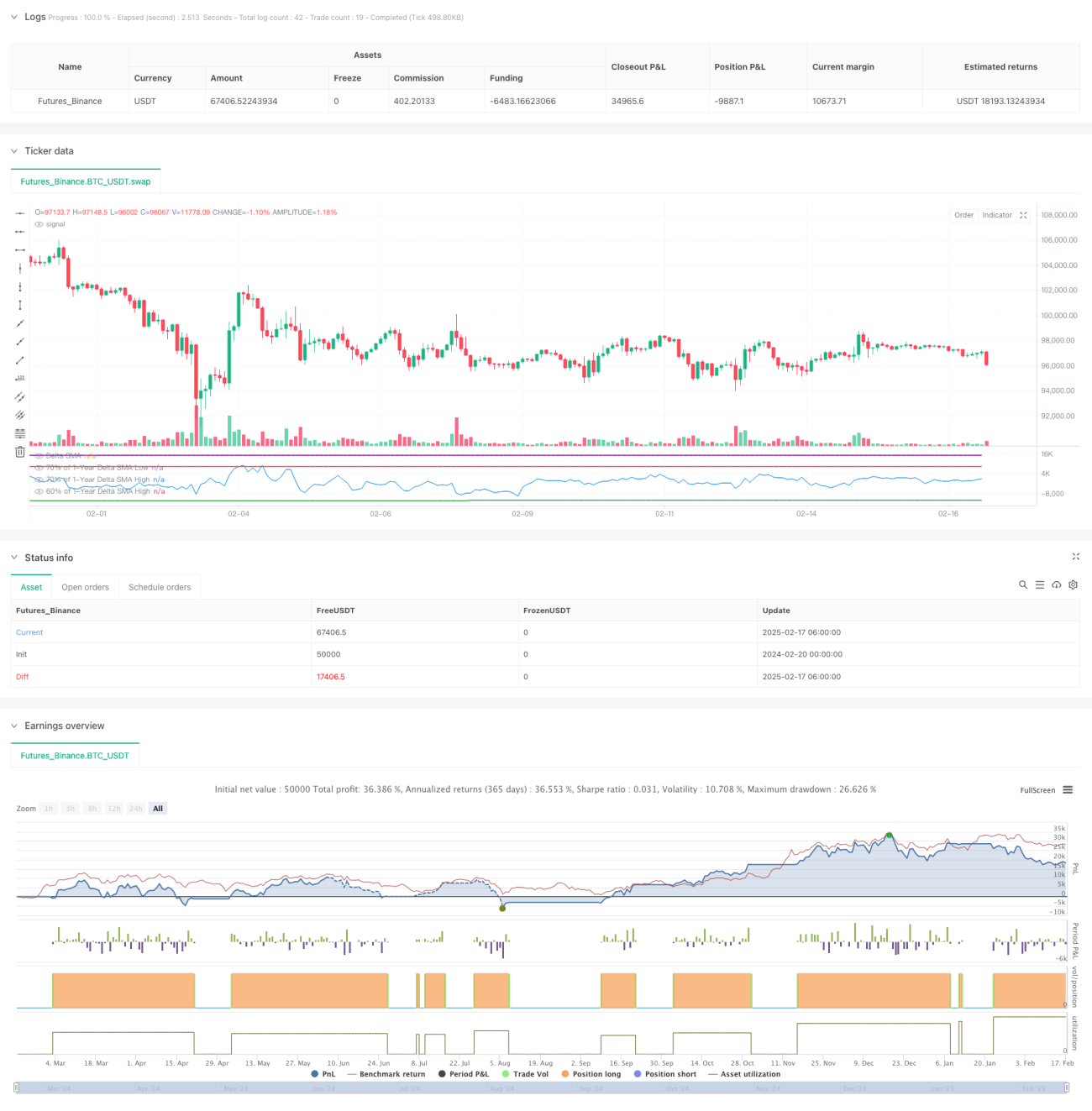

This is a trading strategy based on analyzing the historical highs and lows of the Delta SMA (Simple Moving Average) of buy/sell volumes over a one-year period. The strategy identifies potential trading signals by comparing the Delta SMA with historical threshold values. It employs a long-term lookback period, making it suitable for medium to long-term trend trading.

Strategy Principles

The core logic of the strategy is based on the following key steps:

- Delta Calculation: Calculate the difference between buy and sell volumes based on price movement. Volume is recorded as buy volume when closing price is above opening price, and vice versa.

- SMA Smoothing: Apply a 14-period moving average to the Delta value to reduce noise.

- One-Year High/Low Determination: Calculate the highest and lowest values of Delta SMA over the past year.

- Signal Trigger Conditions:

- Buy Signal: Triggered when Delta SMA crosses above 0 after falling below 70% of the yearly low

- Sell Signal: Triggered when Delta SMA falls below 60% after crossing above 90% of the yearly high

Strategy Advantages

- Strong Long-term Trend Capture: Effectively captures major trends through one-year historical data analysis.

- Excellent Noise Filtering: Uses SMA smoothing and multiple threshold conditions to effectively reduce false signals.

- Reasonable Risk Control: Sets clear entry and exit conditions to avoid overtrading.

- High Adaptability: Strategy parameters can be adjusted for different market conditions.

Strategy Risks

- Lag Risk: Use of SMA and long lookback period may lead to delayed signals.

- False Breakout Risk: May generate false signals in ranging markets.

- Market Environment Dependency: May underperform in markets without clear trends.

- Parameter Sensitivity: Threshold settings significantly impact strategy performance.

Strategy Optimization Directions

- Dynamic Threshold Adjustment: Dynamically adjust high/low thresholds based on market volatility.

- Additional Indicators: Incorporate other technical indicators to improve signal reliability.

- Stop-Loss Implementation: Implement dynamic stop-loss mechanisms for risk control.

- Market Environment Filtering: Add market environment assessment logic to run the strategy in suitable conditions.

Summary

This is a medium to long-term trend following strategy based on volume analysis, capturing market trends by analyzing historical highs and lows of buy/sell volume differences. The strategy is well-designed with proper risk control, but attention needs to be paid to market environment adaptability and parameter optimization. Through the proposed optimization directions, there is room for further strategy improvement.

- 1