2

关注

502

关注者

概述

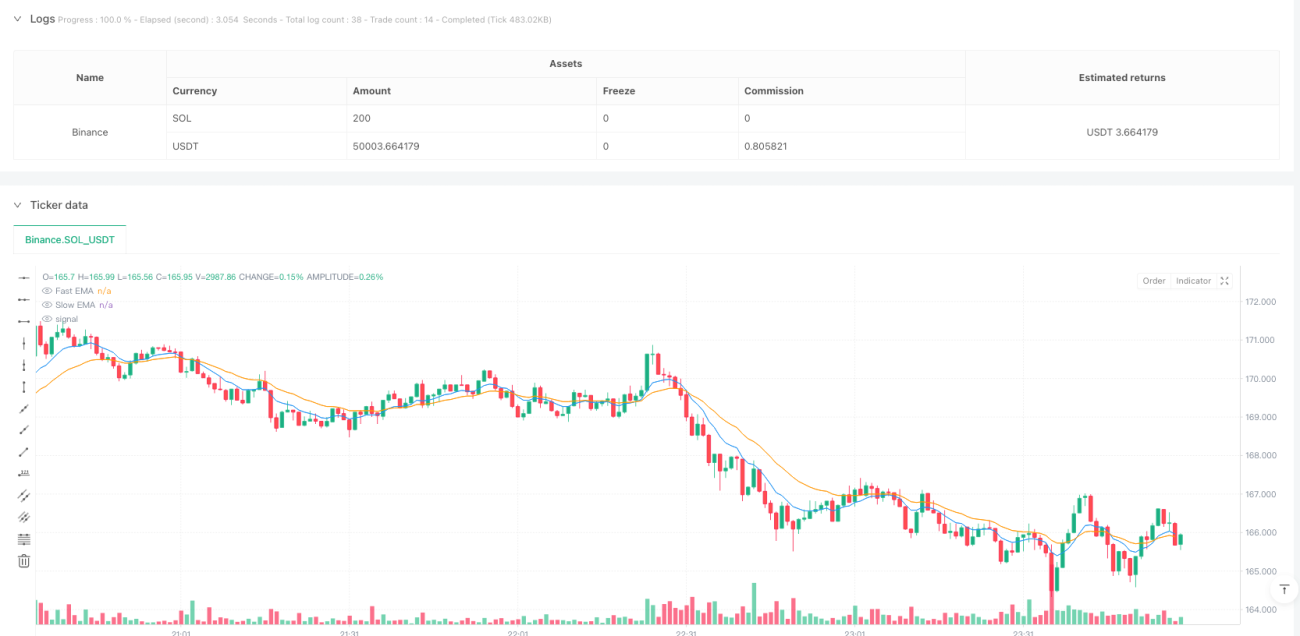

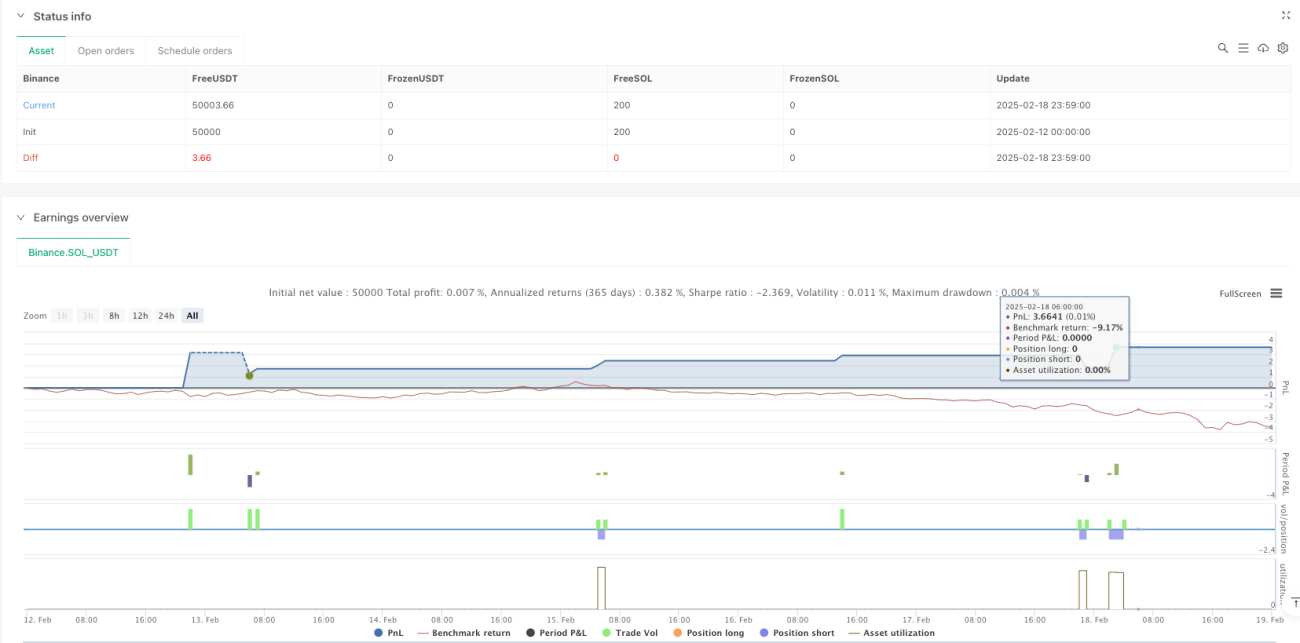

这是一个基于多重技术指标确认的趋势交易策略,结合了移动平均线、动量指标和成交量分析进行交易信号的筛选。策略采用三层过滤机制,包括趋势方向判断(EMA交叉)、动量强度确认(RSI与MACD)以及成交量验证(量能突破与OBV趋势),并配备了基于ATR的风险控制系统。

策略原理

策略运作基于三重确认机制:

- 趋势确认层: 使用9和21周期的指数移动平均线(EMA)交叉来确定总体趋势方向,快线上穿慢线视为上升趋势,反之为下降趋势。

- 动量确认层: 结合RSI和MACD两个动量指标。当RSI大于50且MACD金叉时确认多头动量,当RSI小于50且MACD死叉时确认空头动量。

- 成交量确认层: 要求成交量出现1.8倍于均线的放量,同时通过OBV趋势来验证量价配合的合理性。

风险管理采用1.5倍ATR作为止损标准,默认1:2的风险收益比设置获利目标。

策略优势

- 多层过滤机制显著提高了交易信号的可靠性,减少了虚假信号。

- 将趋势、动量和成交量三个维度结合,全面评估市场状态。

- 基于ATR的动态止损设置,能够根据市场波动性自适应调整。

- 策略包含视觉化工具,便于交易者直观判断入场时机。

- 针对不同波动性资产提供了优化参数建议。

策略风险

- 多重过滤条件可能导致错过部分行情机会。

- 在横盘震荡市场中可能产生频繁的假突破信号。

- 固定的风险收益比可能在某些市场环境下不够灵活。

- 对成交量的依赖可能在低流动性期间产生误导信号。

- EMA参数需要根据不同市场状态进行调整。

策略优化方向

- 引入自适应的指标参数:可根据市场波动率动态调整EMA和RSI的周期。

- 优化成交量判断:考虑引入相对成交量指标,减少异常成交量的影响。

- 改进风险管理:实现基于市场波动性的动态风险收益比调整。

- 增加市场环境过滤:加入趋势强度指标,在强趋势期间采用追踪止损。

- 完善出场机制:结合更多技术指标制定更灵活的出场条件。

总结

这是一个设计完善的多层确认交易策略,通过结合多个技术指标提供了相对可靠的交易信号。策略的风险管理体系较为完善,但仍需要交易者根据具体市场环境进行参数优化。该策略最适合在波动性适中、流动性充足的市场中使用,并且需要交易者具备一定的技术分析基础。

策略源码

Pine

策略参数

评论

全部评论 (0)

暂无数据

- 1