2

关注

502

关注者

概述

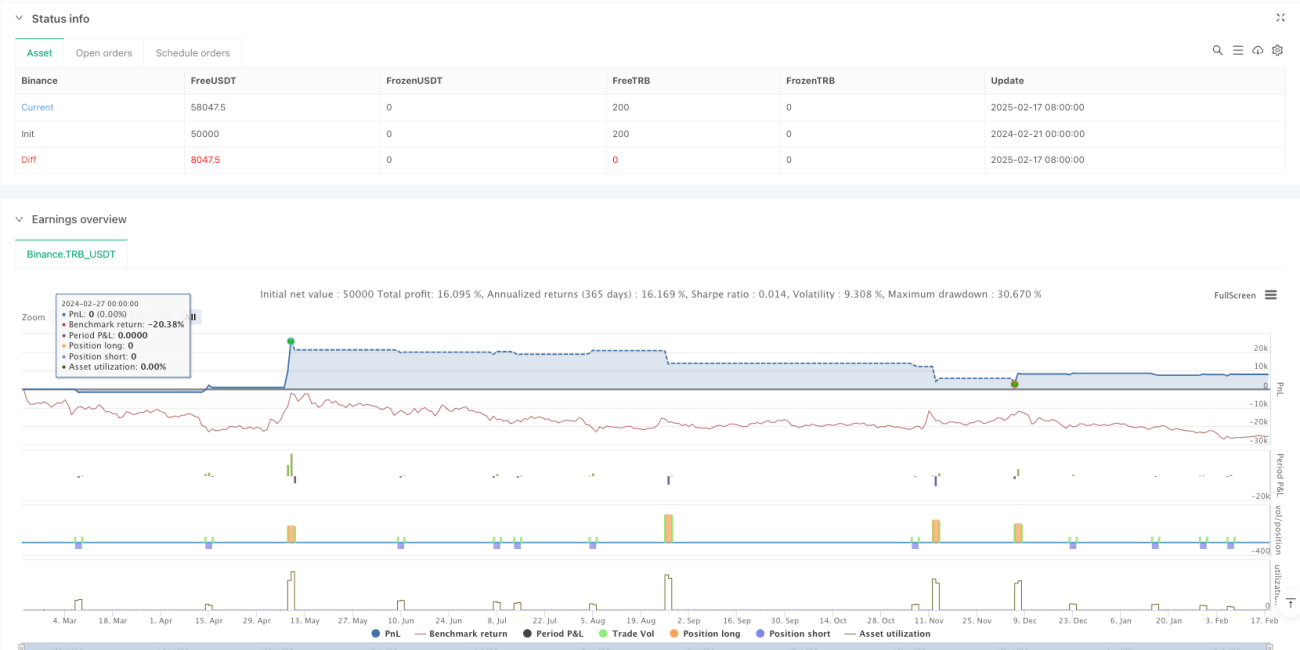

该策略是一个基于价格突破和动态追踪止损的交易系统。它通过监控过去N个周期的最高价和最低价,在价格突破这些关键水平时进行交易。策略采用了智能的止损机制,只有在达到1%的盈利后才激活追踪止损,这样可以让盈利充分发展。同时通过设置1小时的冷却时间来避免过度交易,提高每笔交易的质量。

策略原理

策略的核心逻辑包括以下几个关键部分:

- 入场信号:通过计算过去N个周期的最高价和最低价,当当前价格突破这些水平时触发交易信号。多头入场要求价格突破前期高点一定百分比,空头则需突破前期低点。

- 交易管理:实施1小时交易冷却期,避免在波动剧烈时频繁交易。

- 风险控制:采用动态追踪止损,只在获得1%盈利后激活,可以更好地保护利润。

- 参数优化:关键参数如回看周期、突破阈值、止损百分比等都可以根据不同市场情况进行调整。

策略优势

- 动态风险管理:通过追踪止损机制,策略可以在保护盈利的同时让利润持续增长。

- 灵活适应性:策略可以适应不同的市场条件,通过调整参数来优化表现。

- 过滤机制:使用交易冷却期来避免过度交易,提高交易质量。

- 简单有效:策略逻辑清晰,容易理解和执行,同时保持了较好的可扩展性。

策略风险

- 假突破风险:市场可能出现假突破,导致错误信号。建议增加成交量确认。

- 滑点影响:在高波动期间,可能面临较大滑点,影响策略表现。

- 参数敏感性:策略表现对参数设置较为敏感,需要careful优化。

- 市场环境依赖:在低波动率环境下可能表现不佳。

策略优化方向

- 引入成交量指标:通过成交量确认来提高突破信号的可靠性。

- 增加趋势过滤:结合长期趋势指标,只在趋势方向交易。

- 动态参数调整:根据市场波动率自动调整突破阈值和止损参数。

- 多重时间周期:整合多个时间周期的信号来提高准确率。

总结

这是一个设计合理的趋势跟踪策略,通过价格突破和动态止损相结合,既能捕捉大趋势又能有效控制风险。策略的可定制性强,通过参数优化可以适应不同市场环境。建议在实盘中从小仓位开始,逐步验证策略在不同市场条件下的表现。

策略源码

Pine

策略参数

评论

全部评论 (0)

暂无数据

- 1