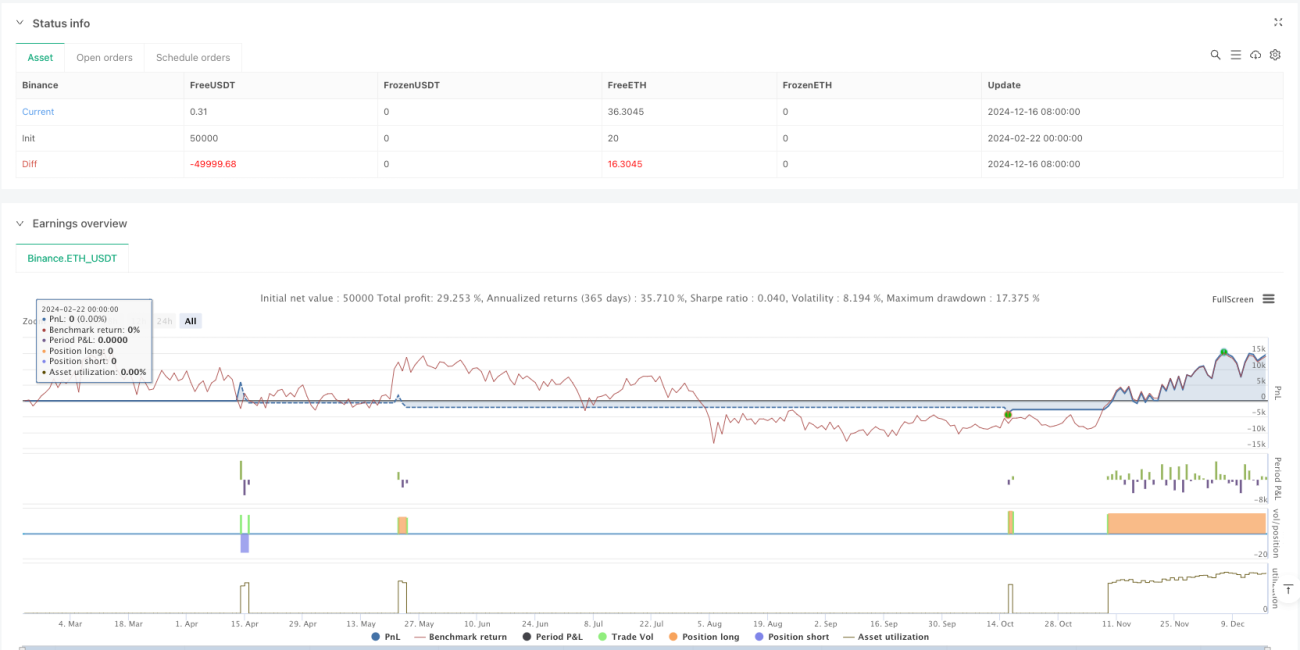

Overview

This is a quantitative trading strategy based on multiple moving average crossovers combined with volume filtering. The strategy utilizes three different period moving averages (fast EMA, slow EMA, and trend SMA) as core indicators, along with a volume filter to confirm signal validity. The strategy also integrates stop-loss and take-profit functions for effective risk control.

Strategy Principles

The strategy is based on several core elements:

- Uses 9-period and 21-period exponential moving averages (EMA) for crossover signals

- Incorporates a 50-period simple moving average (SMA) as a trend filter to ensure trade direction aligns with the main trend

- Uses 1.5 times the 20-period average volume as a volume filter condition

- Confirms signal validity through price breakouts combined with volume expansion

- Sets 1% stop-loss and 400% take-profit to control risk-reward ratio

Strategy Advantages

- Multiple confirmation mechanism: Greatly improves signal reliability through fast/slow MA crossover, trend line filtering, and volume confirmation

- Comprehensive risk control: Sets reasonable stop-loss and take-profit ratios for effective drawdown control

- Strong trend-following capability: Ensures trade direction aligns with main trend through long-term moving average filtering

- High signal quality: Volume filtering effectively prevents false breakouts

- Flexible parameters: All indicator parameters can be optimized for different market characteristics

Strategy Risks

- Sideways market risk: May generate frequent trading signals in range-bound markets, increasing transaction costs

- Slippage risk: May face significant slippage in low liquidity conditions

- False breakout risk: Despite volume filtering, false breakouts may still occur

- Parameter optimization risk: Over-optimization may lead to overfitting

- Market environment dependency: Strategy performs better in trending markets but may underperform in other market conditions

Strategy Optimization Directions

- Introduce volatility indicators: Consider adding ATR indicator for dynamic stop-loss adjustment

- Optimize volume filtering: Consider using relative volume instead of absolute volume as filtering condition

- Add trend strength confirmation: Introduce indicators like ADX to confirm trend strength

- Improve take-profit mechanism: Design dynamic take-profit to better secure profits

- Add time filtering: Avoid trading during low volatility periods

Summary

The strategy constructs a relatively comprehensive trading system through the combination of multiple technical indicators. Its core advantages lie in its multiple confirmation mechanisms and comprehensive risk control, but it still requires parameter optimization and strategy improvements based on actual market conditions. Through proper optimization and risk control, this strategy has the potential to achieve stable returns in trending markets.

/*backtest

start: 2024-02-22 00:00:00

end: 2024-12-17 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("Optimized Moving Average Crossover Strategy with Volume Filter", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Inputs for Moving Averages- 1