概述

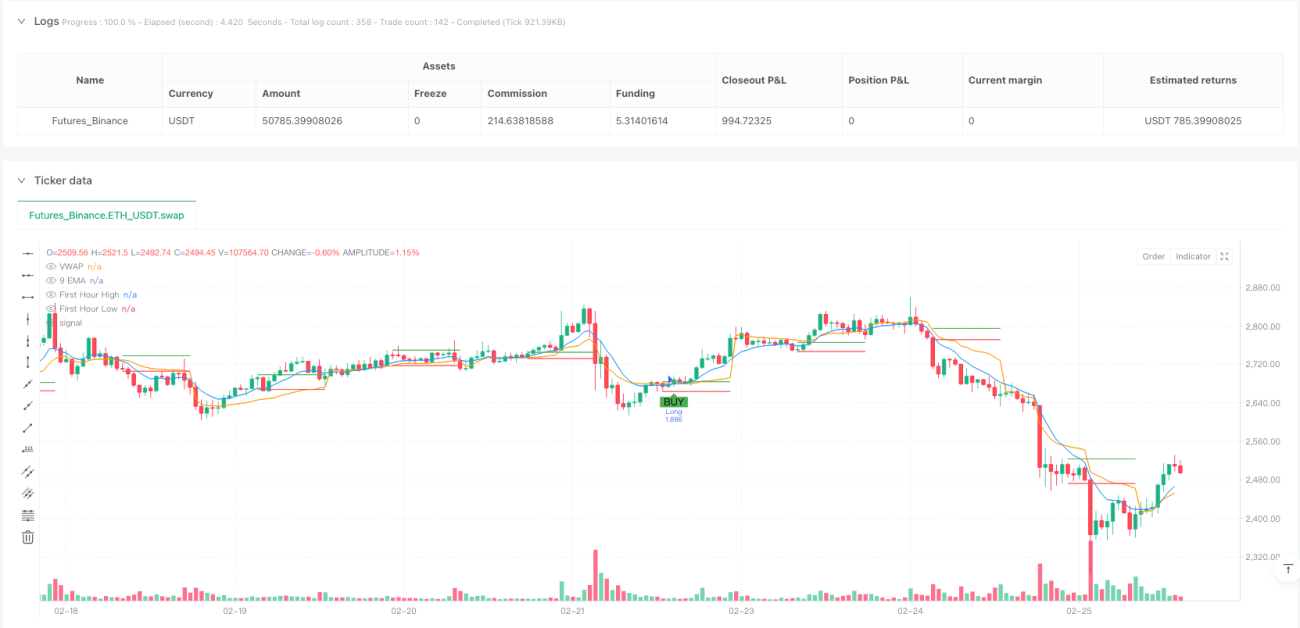

该策略是一种专为日内交易设计的量化交易系统,核心思想围绕市场首个小时的价格行为展开。策略通过识别市场开盘首小时的高低点作为关键突破水平,结合EMA(指数移动平均线)、VWAP(成交量加权平均价格)和动态ATR(平均真实范围)止损机制,构建了一个完整的交易体系。该策略特别注重入场时机的选择,只在市场首小时结束后才允许交易信号触发,这有助于避开早盘的波动和假突破。此外,策略还利用EMA的斜率作为趋势确认工具,确保交易方向与短期趋势一致,从而提高交易的成功率。

策略原理

策略核心逻辑可分为几个关键部分:

-

首小时高低点确定:策略监控并记录市场开盘后首个小时(从9:15开始的60分钟)的最高价和最低价,这两个价格水平将作为潜在突破点。

-

技术指标计算:

- 9周期EMA:作为价格趋势的快速指标

- VWAP:作为市场整体价格水平的参考

- EMA斜率:计算当前EMA与前一周期EMA的差值,用于确认趋势方向

-

入场条件:

- 多头入场:价格突破首小时高点,同时9EMA上穿VWAP,且EMA斜率为正

- 空头入场:价格突破首小时低点,同时9EMA下穿VWAP,且EMA斜率为负

- 两种入场条件均要求首小时时间段已结束

-

出场策略:

- 止损:基于ATR的动态止损,默认为ATR的1倍

- 止盈:固定百分比目标,默认为1%的价格变动

-

资金管理:

- 策略默认使用账户资金的10%进行每次交易

这种设计理念结合了突破交易、趋势确认和动态风险管理,形成了一个完整且系统化的交易方法。通过要求价格突破与技术指标确认同时发生,策略有效降低了假突破的风险。

策略优势

深入分析该策略代码,可以总结出以下几个明显优势:

-

精准的入场时机:通过首小时高低点作为关键水平,策略能够捕捉日内重要的突破机会。市场首小时往往设定了当日的交易区间,突破这些水平通常意味着有强劲的动能推动。

-

多重确认机制:策略不仅依赖价格突破,还要求EMA与VWAP的交叉确认以及EMA斜率的方向一致性,这种多重过滤大大减少了假信号。

-

动态风险管理:使用ATR作为止损基础,策略能根据市场波动性自动调整止损距离,在波动较大时给予价格更多呼吸空间,在波动较小时收紧止损以保护利润。

-

明确的交易规则:策略定义了清晰的入场和出场条件,减少了主观判断,有助于维持交易纪律。

-

视觉辅助功能:代码包含了信号标记和关键水平的可视化,帮助交易者直观理解策略逻辑和实时监控交易机会。

-

适应市场节奏:通过仅在首小时结束后才允许入场,策略避开了开盘时常见的无序波动,专注于更有可能持续的移动。

策略风险

尽管该策略设计合理,但仍存在一些潜在风险和局限性:

-

过度依赖单一时间段:策略过度依赖首小时形成的高低点,如果这一时段不具代表性(例如异常低波动或受到临时新闻影响),可能导致后续交易信号质量下降。

-

固定止盈比例的局限性:1%的固定止盈目标可能无法适应不同市场环境和不同波动性资产。在强趋势日,这可能导致过早获利了结,错失更大潜在盈利。

-

EMA和VWAP延迟风险:作为滞后指标,EMA和VWAP的交叉信号可能出现在价格已经显著突破后,导致入场价格不理想。

-

没有考虑市场整体环境:策略没有纳入更广泛的市场环境评估(如整体市场趋势、波动性环境或相关性分析),可能在某些市场条件下表现欠佳。

-

日内策略的执行挑战:作为日内策略,要求较高的执行效率和较低的滑点,这在实际交易中可能面临挑战。

为降低这些风险,建议:

- 结合其他技术或基本面过滤条件

- 根据资产特性调整ATR倍数和止盈目标

- 考虑增加时间过滤,避免在低效率时段交易

- 定期回测并根据市场变化调整参数

策略优化方向

基于对策略逻辑和潜在风险的分析,以下是几个值得考虑的优化方向:

-

自适应参数调整:

- 根据历史波动性自动调整ATR倍数

- 基于资产特性或市场状态动态设置止盈目标

- 考虑实现自适应的EMA周期,以适应不同市场环境

-

增加市场环境过滤:

- 纳入整体市场趋势评估,如指数方向

- 增加波动性过滤器,在极高或极低波动期间调整策略行为

- 考虑时间过滤,避开特定的低效率交易时段

-

优化首小时逻辑:

- 测试不同的首小时定义(如30分钟、45分钟或90分钟)

- 考虑使用首小时的价格结构而非简单高低点

- 探索前一交易日收盘与当日开盘的关系作为额外过滤条件

-

改进出场机制:

- 实现追踪止损以保护利润并允许趋势延续

- 测试基于技术指标的动态出场(如EMA反向交叉)

- 考虑部分获利策略,在达到特定目标时平仓部分仓位

-

增强风险管理:

- 基于每日波动预期调整头寸规模

- 实现日亏损限制以控制总体风险

- 考虑基于过去交易结果的自适应风险管理

这些优化方向旨在保留策略核心逻辑的同时,提高其适应性和稳健性,使其能在更广泛的市场条件下保持有效。

总结

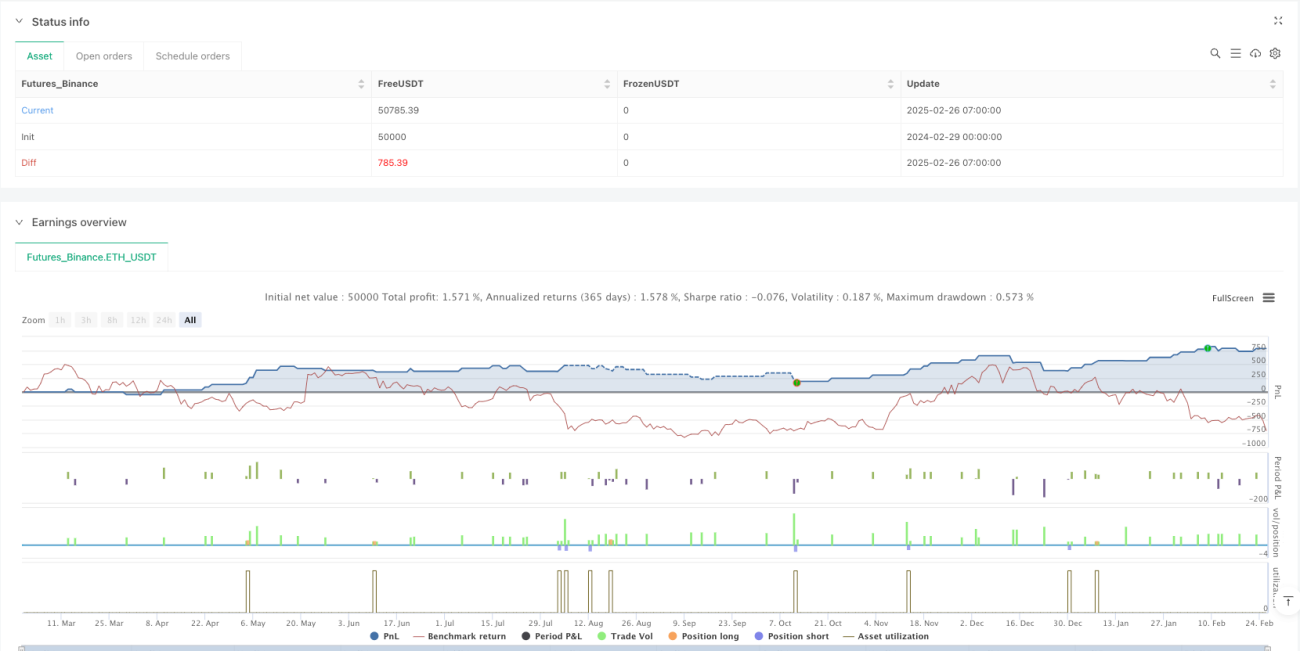

首时段ATR止损与EMA斜率优化策略是一种结构完善的日内量化交易系统,通过结合首小时高低点突破、技术指标确认和动态风险管理,为交易者提供了一种系统化的交易方法。该策略最大的优势在于其多重确认机制和清晰的交易规则,这有助于减少假信号并维持交易纪律。

然而,策略也存在一些局限性,如过度依赖单一时间段和固定止盈目标的适应性问题。通过实施建议的优化措施,如自适应参数调整、增加市场环境过滤和改进出场机制,交易者可以进一步提高策略的稳健性和适应性。

总体而言,这是一个基础扎实、思路清晰的交易策略,特别适合对日内交易感兴趣的量化交易者。通过适当的参数调整和优化,它有潜力成为交易组合中的有效工具。值得注意的是,任何交易策略都需要经过充分的回测和验证,并结合个人风险承受能力进行适当的资金管理。

/*backtest

start: 2024-02-29 00:00:00

end: 2025-02-26 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("FnO Intraday Strategy with ATR SL, EMA Slope & Signals", overlay=true, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// INPUTS- 1