Overview

This is an innovative quantitative trading strategy that provides a structured approach to trading by integrating liquidity zone entries, ATR volatility thresholds, and dynamic risk management. The strategy combines multiple technical analysis indicators to identify high-probability trading opportunities and automatically calculate take profit and stop loss levels.

Strategy Principles

The core principles of the strategy are based on the following key elements:

- Liquidity Zone Analysis: Identifying potential support and resistance areas by calculating the lowest and highest points over a specific period.

- ATR Volatility Filtering: Using Average True Range (ATR) as a dynamic threshold for entry and risk management.

- Trend Filtering: Combining 50-period Exponential Moving Average (EMA) and Relative Strength Index (RSI) to confirm market trend and momentum.

- Dynamic Risk Management: Automatically calculating take profit and stop loss levels based on ATR, with flexible risk/reward ratio adjustment.

Strategy Advantages

- Multi-Dimensional Signal Generation: Combining liquidity, volatility, and trend filtering to improve signal quality.

- Adaptive Risk Management: Dynamically adjusting take profit and stop loss to effectively control trading risk.

- Flexible Parameter Configuration: Customizable ATR length, liquidity period, and trading session.

- Visualization Support: Providing visualization of liquidity lines and first candle level.

- Performance Tracking: Built-in trading statistics table displaying win rate and trade outcomes directly on the chart.

Strategy Risks

- Parameter Sensitivity: Strategy performance highly depends on parameter selection, requiring continuous backtesting and optimization.

- Market Adaptability: Potential instability in markets with unclear trends or high volatility.

- False Breakout Risk: Potential for misreported liquidity zone breakouts.

- Trading Frequency: Session filtering and multiple conditions may reduce trading opportunities.

- Backtest Bias: The 64% historical win rate may not fully represent future performance.

Strategy Optimization Directions

- Machine Learning Integration: Introducing machine learning algorithms for dynamic parameter and signal generation adjustment.

- Multi-Market Adaptability: Developing more universal parameter settings applicable to different markets and instruments.

- Advanced Risk Management: Implementing more complex position sizing and risk allocation algorithms.

- Signal Confirmation Mechanism: Adding additional confirmation indicators like volume or other technical indicators.

- Real-Time Performance Monitoring: Developing real-time performance assessment and adaptive adjustment modules.

Summary

The ThinkTech AI Trading Strategy provides traders with a powerful quantitative trading tool through an innovative multi-factor approach. By leveraging liquidity analysis, volatility filtering, and dynamic risk management, the strategy aims to identify high-quality trading opportunities. However, traders must continuously backtest, optimize, and apply the strategy cautiously to fully realize its potential.

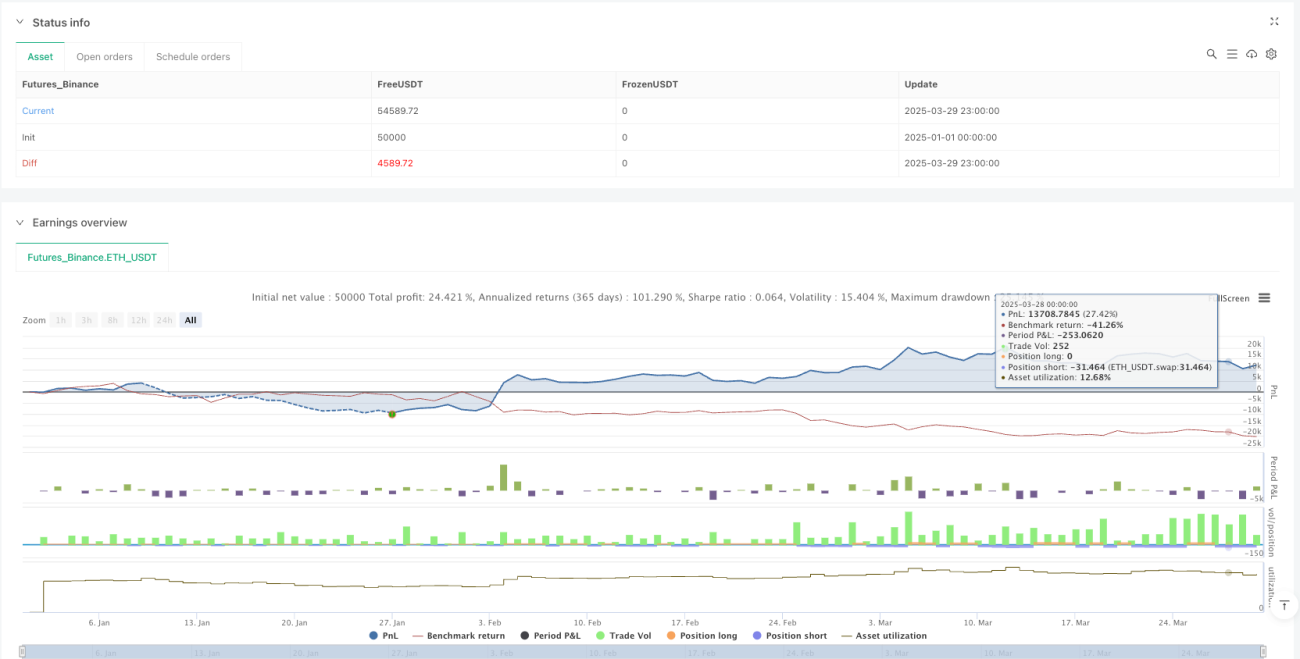

/*backtest

start: 2025-01-01 00:00:00

end: 2025-03-30 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

if high > ta.highest(high[1], 5)

strategy.entry("Enter Long", strategy.long)

else if low < ta.lowest(low[1], 5)

strategy.entry("Enter Short", strategy.short)//@version=6- 1