RSI MA Crossover Swing Trading Strategy with Trailing Stop System

Overview

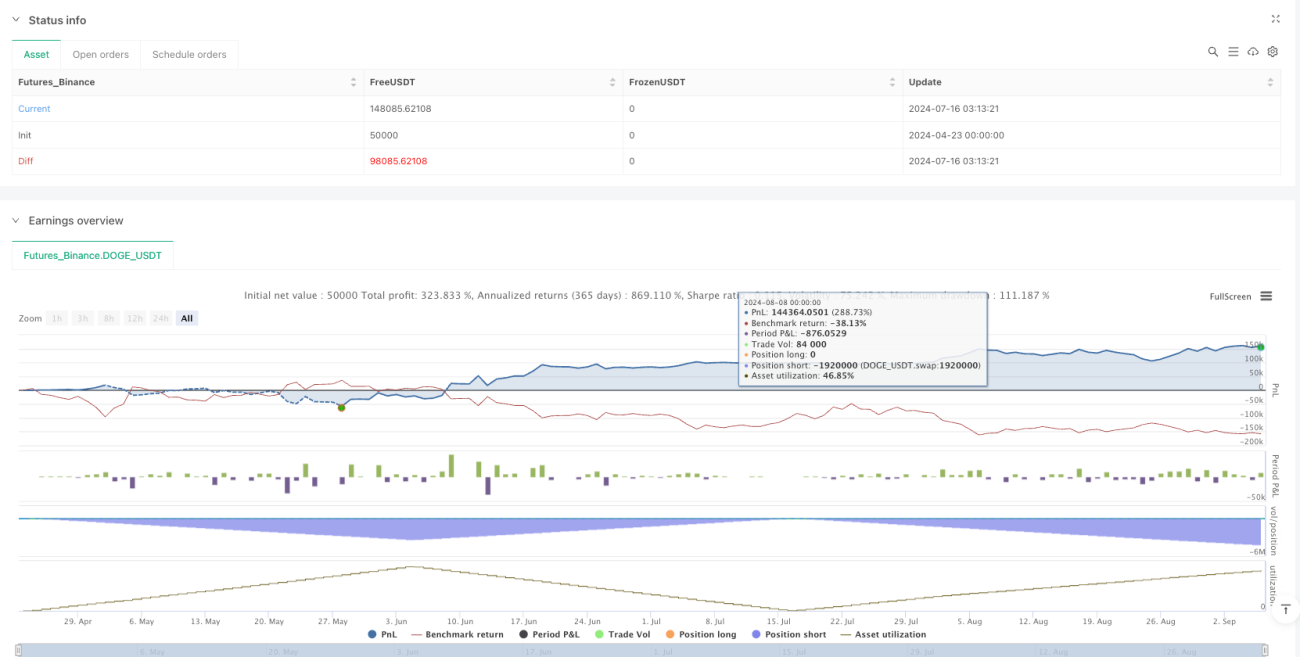

This strategy is a swing trading approach based on the crossover between RSI (Relative Strength Index) and its moving average (MA), designed for 4-hour charts. It generates trading signals through RSI-MA crossovers and incorporates multiple risk management tools, including fixed stop-loss/take-profit, trailing stop-loss, and reversal exit mechanisms. The strategy also imposes a consecutive loss limit, pausing trading after two consecutive losses until a daily reset.

Strategy Logic

- Timeframe Enforcement: The strategy operates exclusively on 4-hour charts to ensure signal alignment with the designed period.

- Indicator Calculation: Uses RSI (default length 14) and its MA (SMA or EMA, default length 14) for signals.

- Golden cross (RSI above MA) triggers long entries.

- Death cross (RSI below MA) triggers short entries.

- Position Sizing: Calculates position size based on allocated capital per trade and current price.

- Exit Mechanisms:

- Fixed SL/TP: Percentage-based stop-loss (default 1.5%) and take-profit (default 2.5%).

- Trailing Stop-Loss: Exits when price retracts by a specified points (default 10) from the peak.

- Reversal Exit: Closes positions on opposing signals.

- Risk Control:

- Pauses trading after two consecutive losses, with a daily reset at 9:15 AM.

Advantages

- Multi-Layered Signal Validation: Combines RSI and MA for reduced false signals.

- Dynamic Risk Management: Trailing stop-locks profits, fixed SL limits losses.

- Strict Capital Allocation: Position sizing prevents over-leverage.

- Disciplinary Control: Loss count mechanism avoids emotional trading.

- Visual Markers: Clear chart annotations for quick signal identification.

Risks

- Parameter Sensitivity: RSI and MA lengths significantly impact signal quality.

- Trend Market Performance: RSI may lag in strong trends due to prolonged overbought/oversold conditions.

- Timeframe Limitation: Requires revalidation for other periods.

- Consecutive Loss Risk: May miss opportunities during pause periods.

Solutions:

- Optimize parameters via backtesting.

- Add trend filters (e.g., ADX).

- Implement dynamic loss count thresholds.

Optimization Directions

- Multi-Indicator Confirmation: Integrate MACD or Bollinger Bands.

- Dynamic Parameters: Adjust RSI length and SL ratios based on market volatility.

- Timeframe Expansion: Test performance on higher/lower timeframes (e.g., daily/1-hour).

- Machine Learning: Train models to optimize entry/exit conditions.

- Advanced Capital Management: Dynamically adjust capital allocation based on equity.

Conclusion

The strategy leverages RSI-MA crossovers for swing trading, balancing profitability and risk through multi-tiered management tools. Its strengths lie in clear logic and discipline, though further optimizations (e.g., multi-indicator integration) could enhance adaptability. Future improvements should focus on dynamic adjustments and broader market validation.

- 1