RSI এবং মুভিং অ্যাভারেজের ভিত্তিতে মাল্টি-টাইমফ্রেম ট্রেডিং কৌশল

সারসংক্ষেপ

এই কৌশলের মূল ধারণা হলো একইসাথে রিলেটিভ স্ট্রেংথ ইনডেক্স (RSI) এবং ভিন্ন সময়কালের মুভিং এভারেজ ব্যবহার করে ট্রেন্ড রিভার্সাল পয়েন্ট চিহ্নিত করা, যাতে মধ্যম ও দীর্ঘমেয়াদী ট্রেন্ড অনুসরণ করার পাশাপাশি স্বল্পমেয়াদী ট্রেডিং করা যায়। এই কৌশলটি বিভিন্ন ট্রেডিং সিগন্যালকে একত্রিত করে, যার লক্ষ্য ট্রেডিংয়ের সাফল্যের হার বাড়ানো।

কৌশলের নীতি

- RSI সূচক, ফাস্ট লাইন EMA এবং স্লো লাইন WMA মুভিং এভারেজ গণনা করা।

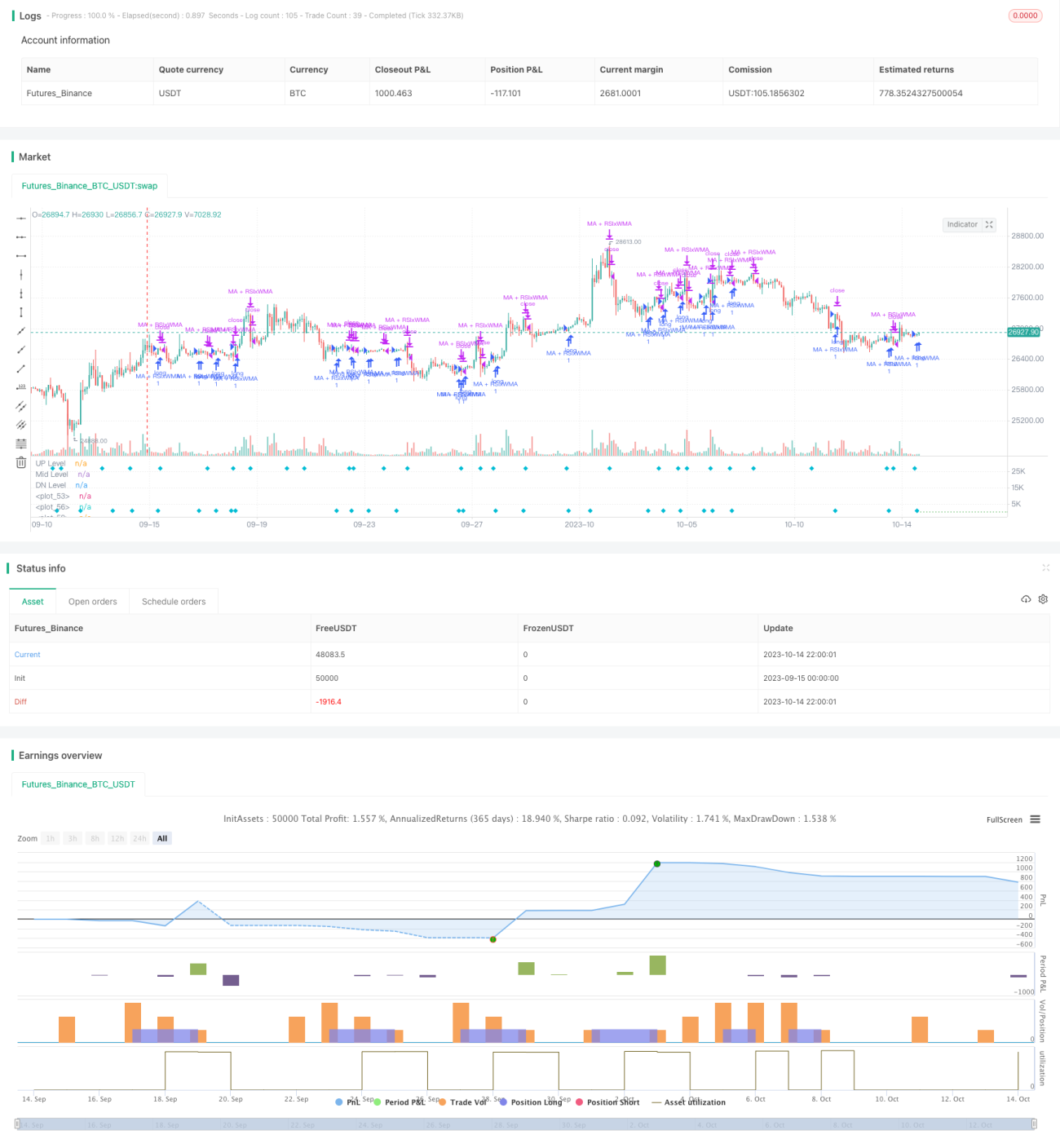

- যখন RSI সূচক রেখা WMA মুভিং এভারেজ রেখাকে অতিক্রম করে, তখন কেনা/বেচার সিগন্যাল তৈরি হয়।

- যখন EMA ফাস্ট লাইন WMA স্লো লাইনকে অতিক্রম করে, তখন কেনা/বেচার সিগন্যাল তৈরি হয়।

- যখন RSI এবং EMA একইসাথে WMA-কে অতিক্রম করে, তখন শক্তিশালী কেনা/বেচার সিগন্যাল তৈরি হয়।

- একইসাথে, যখন দাম সহায়ক মুভিং এভারেজকে অতিক্রম করে, তখন মূল সিগন্যাল আরও শক্তিশালী হয়।

- স্টপ-লস এবং টেক-প্রফিটের শর্ত নির্ধারণ করা হয়।

এই কৌশলটি বিভিন্ন প্রযুক্তিগত সূচকের ব্রেকআউট সিগন্যালকে একত্রিত করে, বিভিন্ন প্যারামিটার সেটিংসের মুভিং এভারেজ ব্যবহার করে বিভিন্ন চক্রের ট্রেন্ড শনাক্ত করে, যার ফলে কৌশলের নির্ভরযোগ্যতা বৃদ্ধি পায়। RSI সূচক ওভারবট/ওভারসোল্ড অবস্থা নির্ধারণ করে, EMA ফাস্ট লাইন স্বল্পমেয়াদী ট্রেন্ড নির্ধারণ করে, WMA স্লো লাইন মধ্যমেয়াদী ট্রেন্ড নির্ধারণ করে এবং দামের সহায়ক মুভিং এভারেজ ব্রেকআউট ট্রেন্ড যাচাই করে। বিভিন্ন সিগন্যালের সমন্বয় কৌশলের কার্যকারিতা বাড়ায়।

সুবিধা বিশ্লেষণ

- RSI সূচকের রিভার্সাল বৈশিষ্ট্য ব্যবহার করে ওভারবট/ওভারসোল্ড এলাকায় রিভার্সালের সুযোগ নেওয়া যায়।

- সহায়ক মুভিং এভারেজ ট্রেন্ড ফিল্টার হিসেবে কাজ করে, ভুল ব্রেকআউট এড়ায়।

- একাধিক সময়কালের সমন্বয় দীর্ঘমেয়াদী ট্রেন্ড ট্র্যাক করার পাশাপাশি স্বল্পমেয়াদী সুযোগও ক্যাপচার করতে সহায়তা করে।

- একাধিক সূচকের সিগন্যাল একত্রিত করে ট্রেডিংয়ের সাফল্যের হার বাড়ানো যায়।

- স্টপ-লস এবং টেক-প্রফিট কৌশল নির্ধারণ করে ঝুঁকি সক্রিয়ভাবে নিয়ন্ত্রণ করা যায়।

ঝুঁকি বিশ্লেষণ

- RSI সূচকে সহজেই ভুল সিগন্যাল তৈরি হতে পারে, তাই সহায়ক মুভিং এভারেজ দিয়ে ফিল্টার করা প্রয়োজন।

- বড় চক্রের ট্রেন্ডে প্রত্যাবর্তন বিপরীতমুখী ট্রেড সিগন্যাল তৈরি করতে পারে, সাবধান থাকা দরকার।

- প্যারামিটার সেটিংস যেমন RSI পিরিয়ডের দৈর্ঘ্য, মুভিং এভারেজ পিরিয়ড ইত্যাদি অপ্টিমাইজ করা প্রয়োজন।

- স্টপ-লস পয়েন্ট নির্ধারণে সতর্কতা অবলম্বন করা জরুরি, যাতে ফাঁদে পড়া এড়ানো যায়।

প্যারামিটার অপ্টিমাইজেশন, কঠোর স্টপ-লস কৌশল এবং বড় চক্রের ট্রেন্ড বিবেচনার মাধ্যমে ঝুঁকি কমানো সম্ভব।

অপ্টিমাইজেশনের দিকনির্দেশনা

- RSI প্যারামিটার অপ্টিমাইজ করে সর্বোত্তম পিরিয়ডের দৈর্ঘ্য খুঁজে বের করা।

- বিভিন্ন ধরনের মুভিং এভারেজ কম্বিনেশন পরীক্ষা করা।

- ATR-এর মতো অস্থিরতা সূচক যুক্ত করে স্টপ-লস ও টেক-প্রফিট পয়েন্ট গতিশীলভাবে সামঞ্জস্য করা।

- ট্রেডিং ভলিউম ম্যানেজমেন্ট মডিউল যোগ করা।

- প্যারামিটার অপ্টিমাইজেশন এবং সিগন্যাল গুণমান মূল্যায়নের জন্য মেশিন লার্নিং কৌশল ব্যবহার করা।

সারসংক্ষেপ

এই কৌশলটি ট্রেন্ড ফলোয়িং এবং এক্সট্রিম পয়েন্ট রিভার্সাল ট্রেডিং ধারণাকে একীভূত করে, একাধিক টাইমফ্রেম বিশ্লেষণ ও বিভিন্ন সূচকের সমন্বিত ব্যবহার যোগ করে, যার লক্ষ্য ট্রেডিং জয়ের হার বৃদ্ধি করা। মূল বিষয় হলো ঝুঁকি নিয়ন্ত্রণ, প্যারামিটার সেটিংস অপ্টিমাইজ করা এবং ট্রেডের উপর বড় চক্রের ট্রেন্ডের প্রভাব যথাসময়ে বিবেচনা করা। সামগ্রিকভাবে, এই কৌশলটির ব্যবহারিকতা এবং ফিটিং ক্ষমতা বেশ ভালো। পরবর্তীতে আরও উন্নত প্রযুক্তি ব্যবহার করে কৌশলের গুণমান আরও বাড়ানো যেতে পারে।

- 1