বহুমাত্রিক সূচকের ভিত্তিতে সিদ্ধান্তগ্রহণকারী স্বল্পমেয়াদী ট্রেন্ড কৌশল

সারসংক্ষেপ

এই কৌশলটি তিনটি ভিন্ন মাত্রার প্রযুক্তিগত সূচককে একত্রিত করে, যেমন সাপোর্ট-রেজিস্ট্যান্স লেভেল, মুভিং এভারেজ সিস্টেম এবং ওভারবট-ওভারসোল্ড সূচক। তাদের সম্মিলিত সংকেতের ভিত্তিতে স্বল্পমেয়াদী ট্রেন্ডের দিক নির্ণয় করে উচ্চতর সাফল্যের হার অর্জন করা হয়।

কৌশলের নীতি

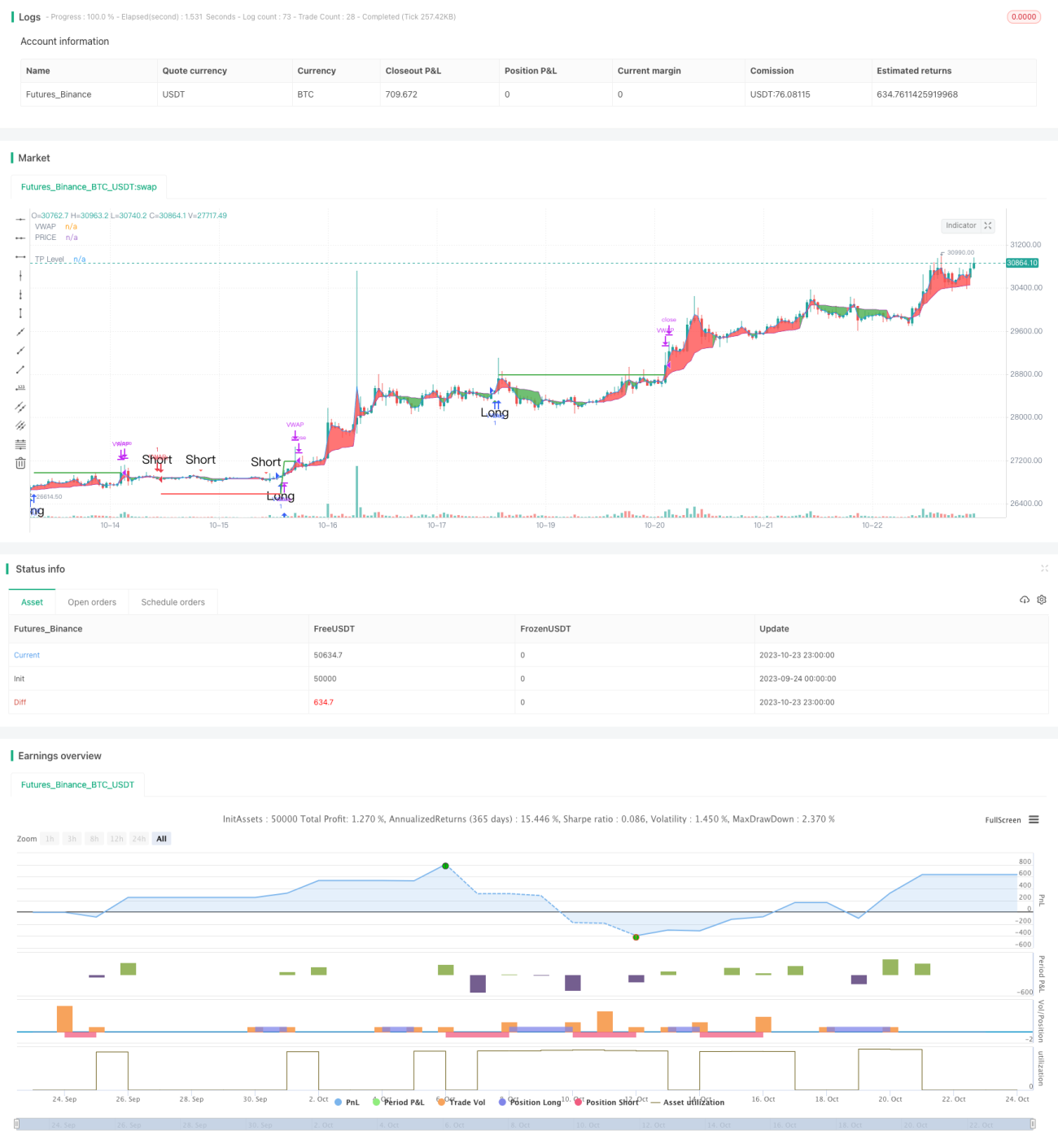

কোডে প্রথমে দামের সাপোর্ট-রেজিস্ট্যান্স লেভেল গণনা করা হয়, যার মধ্যে স্ট্যান্ডার্ড অসিলেটর অক্ষ এবং ফিবোনাচ্চি সাপোর্ট-রেজিস্ট্যান্স লেভেল অন্তর্ভুক্ত, এবং এগুলি চার্টে অঙ্কিত করা হয়। যখন দাম এই গুরুত্বপূর্ণ স্তরগুলি ভেঙে যায়, তখন এটিকে একটি গুরুত্বপূর্ণ ট্রেন্ড সিগন্যাল হিসেবে বিবেচনা করা হয়।

এরপর ওয়েটেড মুভিং এভারেজ VWAP এবং গড় মূল্য গণনা করা হয় এবং তাদের গোল্ডেন ক্রস ও ডেড ক্রস সিগন্যাল নির্ণয় করা হয়। এটি মধ্যম থেকে দীর্ঘমেয়াদী ট্রেন্ড নির্ণয়ের অন্তর্গত।

সবশেষে Stochastic RSI সূচক গণনা করা হয় এবং এর গোল্ডেন ক্রস ও ডেড ক্রস সিগন্যাল নির্ণয় করা হয়, যা ওভারবট-ওভারসোল্ড সূচকের অন্তর্গত।

এই তিনটি মাত্রার সূচককে একত্রিত করে, যদি সাপোর্ট-রেজিস্ট্যান্স লেভেল, VWAP মুভিং এভারেজ এবং Stochastic RSI একই সাথে ক্রয় সংকেত দেয়, তাহলে লং পজিশন খোলা হয়; আর যদি তিনটি একই সাথে বিক্রয় সংকেত দেয়, তাহলে শর্ট পজিশন খোলা হয়।

সুবিধা বিশ্লেষণ

এই কৌশলের সবচেয়ে বড় সুবিধা হলো তিনটি ভিন্ন মাত্রার সূচককে একত্রিত করা, যা নির্ণয়কে আরও ব্যাপক এবং নির্ভুল করে তোলে এবং সাফল্যের হার বেশি হয়। প্রথমত, সাপোর্ট-রেজিস্ট্যান্স লেভেল বড় ট্রেন্ড নির্ধারণ করে; দ্বিতীয়ত, VWAP মধ্যম থেকে দীর্ঘমেয়াদী ট্রেন্ড নির্ধারণ করে; এবং শেষ পর্যন্ত Stochastic RSI ওভারবট-ওভারসোল্ড অবস্থা নির্ণয় করে। তিন মাত্রার সূচক একই সাথে সংকেত দিলে ভুয়া সংকেতগুলি অনেকাংশে ফিল্টার হয়ে যায় এবং এন্ট্রির সাফল্যের হার বৃদ্ধি পায়।

অতিরিক্তভাবে, কৌশলটিতে টেক-প্রফিট ফাংশন যুক্ত করা হয়েছে, যা একটি নির্দিষ্ট শতাংশ মুনাফা লক করতে পারে এবং এটি মূলধন ব্যবস্থাপনায় সহায়ক।

ঝুঁকি বিশ্লেষণ

এই কৌশলের প্রধান ঝুঁকি হলো লং/শর্ট সিদ্ধান্ত সূচকগুলির একসাথে সংকেত দেওয়ার ওপর নির্ভরশীল। যদি কিছু সূচক ভুল সংকেত দেয়, তাহলে সিদ্ধান্ত ভুল হতে পারে। উদাহরণস্বরূপ, Stochastic RSI ওভারবট সংকেত দিতে পারে, কিন্তু VWAP এবং সাপোর্ট-রেজিস্ট্যান্স নির্ণয় এখনও বুলিশ থাকতে পারে, ফলে ক্রয়ের সুযোগ হাতছাড়া হতে পারে এবং পজিশন খোলা নাও যেতে পারে।

এছাড়া, সূচকের প্যারামিটার সঠিকভাবে সেট না করলেও সংকেত নির্ণয়ে ভুল হতে পারে এবং বারবার ব্যাকটেস্টের মাধ্যমে সর্বোত্তম প্যারামিটার খুঁজে বের করতে হবে।

এছাড়াও, শেয়ারবাজারে স্বল্পমেয়াদে প্রায়ই ব্ল্যাক সোয়ান ঘটনা ঘটে, যা সূচককে অকার্যকর করে দিতে পারে। এই ঝুঁকি এড়াতে স্টপ-লস কৌশল যোগ করা যেতে পারে, যাতে একক লেনদেনে বড় ক্ষতি না হয়।

উন্নতির দিকনির্দেশনা

এই কৌশলটি নিম্নলিখিত দিক থেকে উন্নত করা যেতে পারে:

- আরও সূচক সংকেত যোগ করা, যেমন ভলিউম সূচক, যা ট্রেন্ডের শক্তি নির্ণয় করতে এবং সিদ্ধান্তের নির্ভুলতা বাড়াতে সাহায্য করে।

- মেশিন লার্নিং মডেল যোগ করা, যা বহু-মাত্রিক সূচকের উপর প্রশিক্ষণ নিয়ে স্বয়ংক্রিয়ভাবে সর্বোত্তম ট্রেডিং কৌশল খুঁজে বের করতে পারে।

- বিভিন্ন পণ্যের প্যারামিটার অনুযায়ী অপ্টিমাইজ করা এবং অভিযোজিত প্যারামিটার সেট করা।

- স্টপ-লস কৌশল যোগ করা এবং রিট্রেসমেন্টের ভিত্তিতে পজিশনের আকার নিয়ন্ত্রণ করা, যাতে ঝুঁকি আরও ভালভাবে নিয়ন্ত্রণ করা যায়।

- পোর্টফোলিও অপ্টিমাইজেশন করা, যেখানে নিম্ন সম্পর্কযুক্ত পণ্যগুলি খুঁজে বের করে পোর্টফোলিও তৈরি করা যায় এবং পোর্টফোলিও রিট্রেসমেন্ট কমানো যায়।

সারমর্ম

সামগ্রিকভাবে এই কৌশলটি স্বল্পমেয়াদী ট্রেন্ড ট্রেডিংয়ের জন্য অত্যন্ত উপযোগী। এটি বহু-মাত্রিক সূচক ব্যবহার করে সিদ্ধান্ত গ্রহণ করে, যা প্রচুর নয়েজ ফিল্টার করতে পারে এবং সাফল্যের হার উচ্চ। তবে সূচকগুলির ভুল সংকেত দেওয়ার ঝুঁকির দিকে নজর রাখতে হবে। ক্রমাগত উন্নতির মাধ্যমে এই কৌশলটি একটি দক্ষ এবং স্থিতিশীল স্বল্পমেয়াদী কৌশলে পরিণত হতে পারে।

- 1