উচ্চস্তরের মুভিং এভারেজ ব্রেকআউট কৌশল

সংক্ষিপ্ত বিবরণ

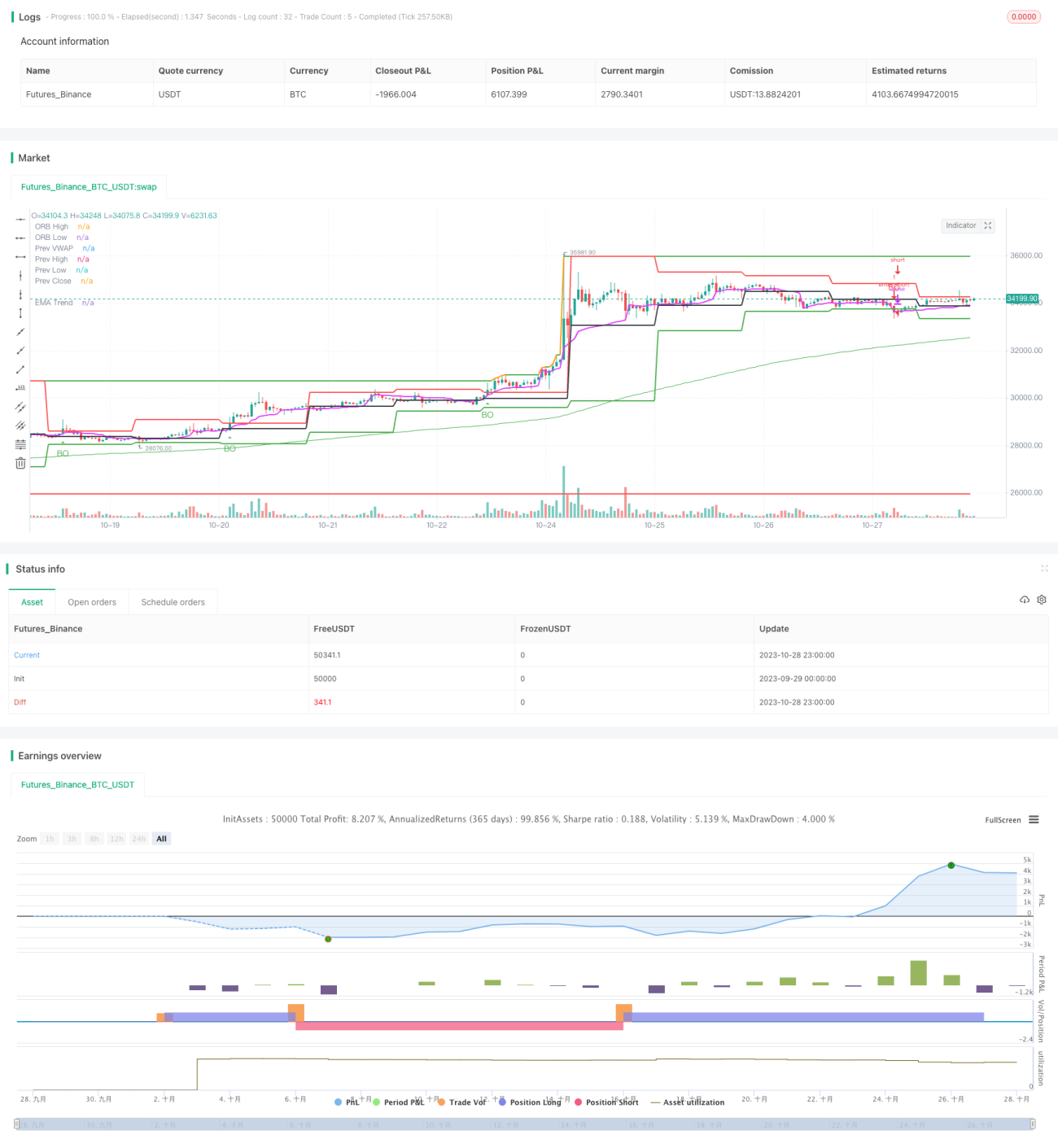

এই কৌশলের মূল ধারণা হল উচ্চ স্তরের মুভিং এভারেজের ব্রেকআউট ব্যবহার করে ট্রেন্ড ট্রেডিং করা। উচ্চ সময়সীমায়, যখন মূল্য উপরে বা নিচে মুভিং এভারেজ ভেঙে যায়, তখন ট্রেন্ডের শুরু সনাক্ত করা যায় এবং সেই অনুযায়ী উপযুক্ত দিক বেছে নিয়ে ট্র্যাকিং করা যায়।

কৌশলের নীতি

এই কৌশলটি Pine Script ভাষায় তৈরি, প্রধানত নিম্নলিখিত অংশ নিয়ে গঠিত:

-

ইনপুট প্যারামিটার

মুভিং এভারেজ পিরিয়ড প্যারামিটার

periodসংজ্ঞায়িত করা হয়েছে, ডিফল্ট মান 200; ক্যান্ডেলস্টিক সময় প্যারামিটারtimeframeসংজ্ঞায়িত করা হয়েছে, ডিফল্ট মান দৈনিক "D"। -

মুভিং এভারেজ গণনা

ta.emaফাংশন ব্যবহার করে এক্সপোনেনশিয়াল মুভিং এভারেজ (EMA) গণনা করা হয়। -

ব্রেকআউট নির্ধারণ

ta.crossoverএবংta.crossunderফাংশন ব্যবহার করে মূল্য মুভিং এভারেজ ভেঙে উপরে বা নিচে যাচ্ছে কিনা তা নির্ধারণ করা হয়। -

সিগন্যাল অঙ্কন

ব্রেকআউট ঘটলে ক্যান্ডেলস্টিকে উপরে বা নিচের তীর চিহ্ন অঙ্কন করা হয়।

-

ট্রেড খোলা ও বন্ধ

ব্রেকআউট ঘটলে দিক নির্বাচন করে পজিশন খোলা হয় এবং দ্বিগুণ স্টপ লস দূরত্ব পৌঁছালে পজিশন বন্ধ করা হয়।

এই কৌশলটি মূলত উচ্চ স্তরের মুভিং এভারেজের ট্রেন্ড নির্ধারণ ক্ষমতার উপর নির্ভর করে এবং সাধারণ ব্রেকআউট অপারেশনের মাধ্যমে ট্রেন্ড ট্র্যাকিং করে, যা একটি ঐতিহ্যবাহী ব্রেকআউট কৌশল।

সুবিধা বিশ্লেষণ

এই কৌশলের নিম্নলিখিত সুবিধা রয়েছে:

-

ধারণা সহজ, বোঝা এবং আয়ত্ত করা সহজ।

-

শুধুমাত্র একটি মুভিং এভারেজ সূচক ব্যবহার করে, প্যারামিটার সমন্বয় সহজ।

-

ব্রেকআউট অপারেশন সহজেই ট্রেন্ড তৈরি করে, ঘন ঘন ট্রেড হয় না।

-

উচ্চ স্তরের সময়সীমা স্পষ্টভাবে বড় ট্রেন্ড প্রদর্শন করে, স্বল্পমেয়াদী ওঠানামায় সহজে প্রভাবিত হয় না।

-

বিভিন্ন সময়সীমার কম্বিনেশন কনফিগার করা যায়, বিভিন্ন সম্পদের সাথে মানিয়ে যায়।

-

সহজেই একাধিক সম্পদ ট্র্যাক করা যায়, একসঙ্গে আটকা পড়ার সম্ভাবনা কম।

ঝুঁকি বিশ্লেষণ

এই কৌশলে কিছু ঝুঁকিও রয়েছে:

-

ব্রেকআউট সিগন্যাল মিথ্যা ব্রেকআউট হতে পারে, বাজারের দোলন কার্যকরভাবে ফিল্টার করতে পারে না।

-

স্বল্পমেয়াদী সুযোগ লাভের জন্য কার্যকরভাবে ব্যবহার করা যায় না।

-

বড় দিক ভুল হলে লোকসান গুরুতর হতে পারে।

-

মুভিং এভারেজের সময়কাল এবং ট্রেডিং সময়কাল মেলে না, তখন অতিরিক্ত ট্রেডিং বা লিকেজ হতে পারে।

-

রিয়েল-টাইম স্টপ লস না থাকায় লোকসান বড় হওয়ার সম্ভাবনা বেশি।

ঝুঁকির সমাধানের মধ্যে রয়েছে: ট্রেন্ড সূচক যুক্ত করা, ফিল্টার শর্ত বৃদ্ধি করা, পজিশন হোল্ডিং সময় যথাযথভাবে সংক্ষিপ্ত করা, স্টপ লস অবস্থান গতিশীলভাবে সমন্বয় করা ইত্যাদি।

অপ্টিমাইজেশনের দিক

এই কৌশলটি নিম্নলিখিত দিক থেকে অপ্টিমাইজ করা যেতে পারে:

-

ট্রেন্ড সূচকের সংমিশ্রণ বৃদ্ধি করা, যেমন MACD, KD ইত্যাদি, ব্রেকআউটের নির্ভরযোগ্যতা বাড়ানো।

-

ভলিউম বা বলিঙ্গার ব্যান্ড চ্যানেলের মতো ফিল্টার শর্ত যুক্ত করা, মিথ্যা ব্রেকআউট এড়ানো।

-

প্যারামিটার সময়ের মিল অপ্টিমাইজ করা, পজিশন হোল্ডিং সময় এবং ট্রেন্ড সময়ের মধ্যে সমন্বয় উন্নত করা।

-

রিয়েল-টাইম স্টপ লস কৌশল যুক্ত করা, ট্রেলিং স্টপের মাধ্যমে একক ট্রেডের লোকসান নিয়ন্ত্রণ করা।

-

মেশিন লার্নিং প্রযুক্তির সংমিশ্রণ বিবেচনা করা, প্যারামিটারের গতিশীল অপ্টিমাইজেশন অর্জন করা।

-

একাধিক সম্পদ বরাদ্দ পোর্টফোলিও পরীক্ষা করা, সামগ্রিক স্থিতিশীলতা বৃদ্ধি করা।

সারসংক্ষেপ

সামগ্রিকভাবে এই কৌশলটি সহজ এবং ব্যবহারিক, সাধারণ মুভিং এভারেজ ব্রেকআউটের মাধ্যমে ট্রেন্ড ট্র্যাকিং করে, সহজে আয়ত্ত করা যায় এবং কোয়ান্ট ট্রেডিংয়ের একটি প্রাথমিক কৌশল হিসেবে ব্যবহার করা যেতে পারে। তবে কিছু সমস্যা রয়েছে, যা সূচক সমন্বয়, প্যারামিটার অপ্টিমাইজেশন, ডায়নামিক স্টপ লস ইত্যাদির মাধ্যমে উন্নত করা প্রয়োজন, যাতে কৌশলটি আরও স্থিতিশীল এবং কার্যকর হয়। অপ্টিমাইজেশনের এবং সম্প্রসারণের যথেষ্ট সুযোগ রয়েছে।

- 1