সুপার মোমেন্টাম কৌশল

সংক্ষিপ্ত বিবরণ

সুপার মোমেন্টাম স্ট্র্যাটেজি একাধিক মোমেন্টাম ইন্ডিকেটর সমন্বিতভাবে ব্যবহার করে। যখন একাধিক মোমেন্টাম ইন্ডিকেটর একসাথে বুলিশ বা বিয়ারিশ সিগন্যাল দেয়, তখন ক্রয় বা বিক্রয় করা হয়। এই কৌশলটি একাধিক মোমেন্টাম ইন্ডিকেটর সংমিশ্রণ করে মূল্যের ট্রেন্ড আরও নির্ভুলভাবে ধরতে পারে এবং একক ইন্ডিকেটরের কারণে ভুল সিগন্যাল এড়াতে সাহায্য করে।

কৌশলের মূলনীতি

এই কৌশলটি একইসাথে ৪টি এভারগেটের RMI ইন্ডিকেটর এবং ১টি চান্ডে মোমেন্টাম অসিলেটর ব্যবহার করে। RMI ইন্ডিকেটর মূল্যের মোমেন্টামের ভিত্তিতে গণনা করা হয় এবং এটি মূল্যের ঊর্ধ্বমুখী ও নিম্নমুখী গতিশক্তি নির্ধারণ করতে পারে। চান্ডে MO মূল্যের পরিবর্তন গণনা করে বাজারের ওভারবট বা ওভারসেল অবস্থা নির্ণয় করে।

যখন RMI5 তার ক্রয় লাইন উপরে ক্রস করে, RMI4 তার ক্রয় লাইন নিচে ক্রস করে, RMI3 তার ক্রয় লাইন নিচে ক্রস করে, RMI2 তার ক্রয় লাইন নিচে ক্রস করে, RMI1 তার ক্রয় লাইন নিচে ক্রস করে এবং চান্ডে MO তার ক্রয় লাইন উপরে ক্রস করে, তখন ক্রয় অপারেশন করা হয়।

যখন RMI5 তার বিক্রয় লাইন নিচে ক্রস করে, RMI4 তার বিক্রয় লাইন উপরে ক্রস করে, RMI3 তার বিক্রয় লাইন উপরে ক্রস করে, RMI2 তার বিক্রয় লাইন উপরে ক্রস করে, RMI1 তার বিক্রয় লাইন উপরে ক্রস করে এবং চান্ডে MO তার বিক্রয় লাইন নিচে ক্রস করে, তখন বিক্রয় অপারেশন করা হয়।

RMI5 অন্যগুলোর বিপরীত দিকে সেট করা হয়, যা ট্রেন্ড শনাক্তকরণ এবং পিরামিড অপারেশনে সহায়তা করে।

সুবিধা বিশ্লেষণ

- একাধিক ইন্ডিকেটর যুক্ত হওয়ায় ট্রেন্ড আরও নির্ভুলভাবে শনাক্ত করা যায় এবং একক ইন্ডিকেটরের ভুল সিগন্যাল এড়ানো যায়

- একাধিক সময়কালের ইন্ডিকেটর অন্তর্ভুক্ত, যা বড় স্তরের ট্রেন্ড শনাক্ত করতে পারে

- বিপরীতমুখী RMI ইন্ডিকেটর ট্রেন্ড শনাক্তকরণ এবং পিরামিড অপারেশনে সহায়তা করে

- চান্ডে MO ওভারবট/ওভারসেল অবস্থায় ভুল ট্রেড এড়াতে সহায়তা করে

ঝুঁকি বিশ্লেষণ

- অনেক ইন্ডিকেটরের সংমিশ্রণ এবং জটিল প্যারামিটার সেটিংসের জন্য সতর্ক পরীক্ষা-নিরীক্ষা ও অপ্টিমাইজেশন প্রয়োজন

- একাধিক ইন্ডিকেটর একসাথে পরিবর্তিত হলে ভুল সিগন্যাল তৈরি হতে পারে

- একাধিক ইন্ডিকেটর ব্যবহারের ফলে ট্রেডিং ফ্রিকোয়েন্সি কম হতে পারে

- বিভিন্ন পণ্য ও বাজার পরিবেশের জন্য ইন্ডিকেটর প্যারামিটার উপযুক্ত কিনা তা লক্ষ্য রাখতে হবে

অপ্টিমাইজেশনের দিকনির্দেশনা

- ইন্ডিকেটর প্যারামিটার সেটিংস পরীক্ষা করে স্থিতিশীলতা বৃদ্ধির জন্য অপ্টিমাইজ করা

- কিছু ইন্ডিকেটর যোগ বা বাদ দিয়ে সিগন্যাল মানের উপর প্রভাব মূল্যায়ন করা

- নির্দিষ্ট বাজার পরিস্থিতিতে ভুল সিগন্যাল এড়ানোর জন্য কিছু ফিল্টার শর্ত যোগ করা

- ইন্ডিকেটরের ক্রয়/বিক্রয় লাইন অবস্থান সামঞ্জস্য করে সর্বোত্তম প্যারামিটার সংমিশ্রণ খুঁজে বের করা

- ঝুঁকি নিয়ন্ত্রণের জন্য স্টপ-লস মেকানিজম যোগ করার কথা বিবেচনা করা

সারসংক্ষেপ

এই কৌশলটি একাধিক মোমেন্টাম ইন্ডিকেটর ব্যবহার করে বাজারের ট্রেন্ড বিচারের ক্ষমতা বাড়ায়। তবে প্যারামিটার সেটিংস জটিল, তাই সতর্ক পরীক্ষা-নিরীক্ষা, অপ্টিমাইজেশন এবং ক্রমাগত উন্নতি ও সমন্বয় প্রয়োজন। সঠিকভাবে ব্যবহার করলে এটি উন্নত ট্রেডিং সিগন্যাল দিতে পারে এবং ট্রেন্ড অনুসরণে কিছু সুবিধা দেয়। তবে ব্যবসায়ীদের ঝুঁকির দিকে নজর রাখতে হবে, সর্বোত্তম প্যারামিটার সংমিশ্রণ খুঁজে বের করতে হবে এবং স্থিতিশীল ট্রেডিংয়ের জন্য ঝুঁকি নিয়ন্ত্রণ প্রক্রিয়া যুক্ত করতে হবে।

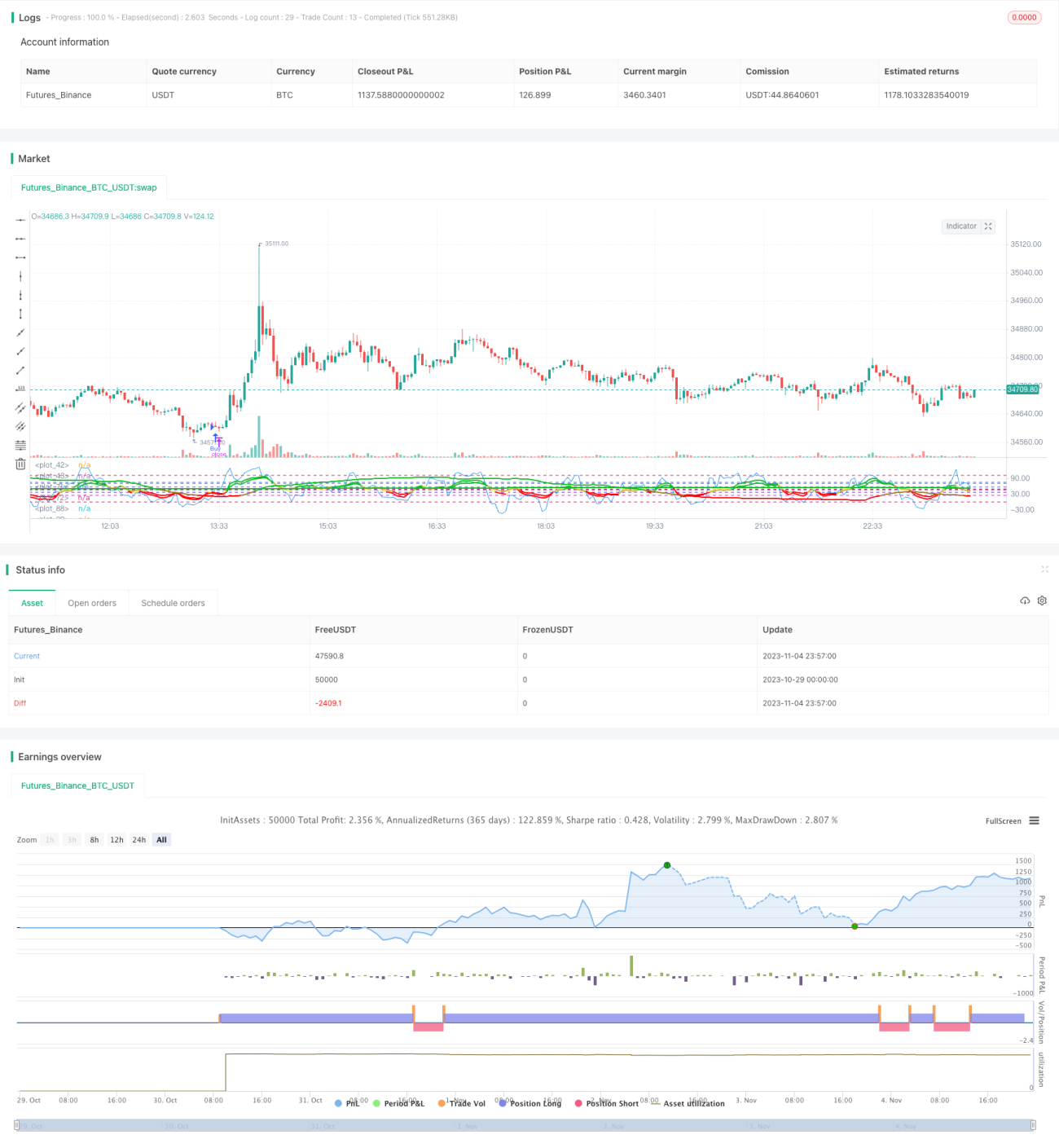

/*backtest

start: 2023-10-29 00:00:00

end: 2023-11-05 00:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="Super Momentum Strat", shorttitle="SMS", format=format.price, precision=2)

//* Backtesting Period Selector | Component *//- 1