অতি-ইচিমোকু ট্রেন্ড কৌশল

সারসংক্ষেপ

চাও ই স্ট্র্যাটেজি হল একটি ট্রেন্ড অনুসরণকারী ট্রেডিং কৌশল যা চাও ই ইন্ডিকেটরের উপর ভিত্তি করে ট্রেডিং সিদ্ধান্ত নেয়। এই কৌশলটি চাও ই ইন্ডিকেটরের কনভার্সন লাইন, বেস লাইন এবং ক্লাউড ব্যান্ডের সম্পর্ক ব্যবহার করে বর্তমান ট্রেন্ডের দিক নির্ণয় করে এবং মূল্যের রিট্রেসমেন্টের সাথে একত্রে এন্ট্রি করে।

চাও ই স্ট্র্যাটেজি মূলত মধ্যম থেকে দীর্ঘমেয়াদী ট্রেন্ড ট্রেডিংয়ের জন্য উপযুক্ত, যা বড় ট্রেন্ডে লাভ অর্জন করতে পারে। এই কৌশলটির ট্রেন্ড শনাক্তকরণ ক্ষমতাও বেশ শক্তিশালী।

কৌশলের নীতি

চাও ই স্ট্র্যাটেজি ট্রেডিং দিক নির্ধারণের জন্য নিম্নলিখিত উপাদানগুলি মূল্যায়ন করে:

-

কনভার্সন লাইন এবং বেস লাইনের সম্পর্ক: কনভার্সন লাইন উপরে থাকলে বুলিশ, নিচে থাকলে বিয়ারিশ।

-

ক্লাউড ব্যান্ডের রঙ: ক্লাউড ব্যান্ড সবুজ হলে বুলিশ, লাল হলে বিয়ারিশ।

-

মূল্যের রিট্রেসমেন্ট: মূল্যকে কনভার্সন লাইন এবং বেস লাইনের বাইরে ফিরে আসতে হবে, তবেই এন্ট্রি করা যাবে।

বিশেষভাবে, কৌশলের ট্রেডিং সিগন্যাল হলো:

লং সিগন্যাল:

- কনভার্সন লাইন বেস লাইনের উপরে

- মূল্য কনভার্সন লাইন এবং বেস লাইনের উপরে

- কনভার্সন লাইন এবং বেস লাইন ক্লাউড ব্যান্ডের উপরে

- মূল্য কনভার্সন লাইন এবং বেস লাইনের নিচে ফিরে আসে

শর্ট সিগন্যাল:

- কনভার্সন লাইন বেস লাইনের নিচে

- মূল্য কনভার্সন লাইন এবং বেস লাইনের নিচে

- কনভার্সন লাইন এবং বেস লাইন ক্লাউড ব্যান্ডের নিচে

- মূল্য কনভার্সন লাইন এবং বেস লাইনের উপরে ফিরে আসে

যখন লং/শর্ট সিগন্যাল একসাথে পূরণ হয়, তখন পজিশনের অবস্থা অনুযায়ী অর্ডার খোলা হয়।

সুবিধা বিশ্লেষণ

চাও ই স্ট্র্যাটেজির নিম্নলিখিত সুবিধা রয়েছে:

-

চাও ই ইন্ডিকেটরের সংমিশ্রণ ব্যবহার করে ট্রেন্ডের দিক নির্ণয় করা হয়, যার নির্ভুলতা বেশি।

-

কনভার্সন লাইন এবং বেস লাইন স্বল্প থেকে মধ্যমেয়াদী ট্রেন্ড স্পষ্টভাবে নির্ধারণ করতে পারে, আর ক্লাউড ব্যান্ড দীর্ঘমেয়াদী ট্রেন্ড নির্ধারণ করে।

-

শর্ত হিসেবে মূল্যকে টার্নিং লাইনের বাইরে ফিরে আসতে হবে, যা ভুয়া ব্রেকআউটের কারণে ক্ষতি এড়াতে সাহায্য করে।

-

ঝুঁকি নিয়ন্ত্রণের জন্য সাম্প্রতিক সময়ের সর্বোচ্চ ও সর্বনিম্ন মূল্য স্তর ব্যবহার করে স্টপ লস নির্ধারণ করা হয়, যা একক ট্রেডের ক্ষতি কার্যকরভাবে নিয়ন্ত্রণ করতে পারে।

-

ঝুঁকি-লাভের অনুপাত যুক্তিসঙ্গত, যা স্থিতিশীল মুনাফা অর্জনের লক্ষ্য রাখে।

-

বিভিন্ন টাইমফ্রেমে প্রয়োগ করা যায়, যা মধ্যম থেকে দীর্ঘমেয়াদী ট্রেন্ড ট্রেডিংয়ের জন্য উপযুক্ত।

-

কৌশলের চিন্তাধারা স্পষ্ট এবং সহজে বোধগম্য, প্যারামিটার অপটিমাইজেশনের সুযোগ বেশি।

-

বিভিন্ন বাজার পরিবেশে কার্যকরী হতে পারে।

ঝুঁকি বিশ্লেষণ

চাও ই স্ট্র্যাটেজির নিম্নলিখিত ঝুঁকিও রয়েছে:

-

রেঞ্জবাউন্ড বাজারে স্টপ লস ঘন ঘন ট্রিগার হতে পারে, যা লাভজনকতাকে প্রভাবিত করে।

-

ট্রেন্ড দ্রুত পরিবর্তিত হলে সময়মতো পজিশন রিভার্স করা যায় না, যা ক্ষতির কারণ হতে পারে।

-

নির্ধারিত ঝুঁকি-লাভের অনুপাত সব সম্পদের জন্য উপযুক্ত নয়, বিভিন্ন লক্ষ্যের জন্য প্যারামিটার সমন্বয় করতে হবে।

-

ক্লাউড ব্রেকআউটের পর উর্ধ্বগতির জায়গা সীমিত হলে লাভ সীমিত হতে পারে।

-

ইন্ডিকেটর প্যারামিটার বারবার টেস্ট এবং অপটিমাইজ করতে হয়, যা ঘন ঘন প্যারামিটার পরিবর্তন করতে হয় এমন সম্পদের জন্য উপযুক্ত নয়।

নিম্নলিখিত পদ্ধতিতে ঝুঁকি কমানো যেতে পারে:

-

প্যারামিটার অপটিমাইজ করে বিভিন্ন টাইমফ্রেম ও সম্পদের বৈশিষ্ট্যের সাথে আরও সঙ্গতিপূর্ণ করা।

-

অন্যান্য ইন্ডিকেটরের সাথে মিলিয়ে এন্ট্রি সিগন্যাল ফিল্টার করা, রেঞ্জবাউন্ড বাজারে ভুয়া ব্রেকআউট এড়ানো।

-

ডাইনামিক স্টপ লস পজিশন অ্যাডজাস্ট করে স্টপ লস ট্রিগার হওয়ার সম্ভাবনা কমানো।

-

বিভিন্ন ঝুঁকি-লাভের অনুপাত সেটিংস টেস্ট করা।

-

চার্ট প্যাটার্ন ইত্যাদি পদ্ধতি ব্যবহার করে ট্রেন্ড সিগন্যালের শক্তি নির্ধারণ করা।

অপটিমাইজেশনের দিকনির্দেশনা

চাও ই স্ট্র্যাটেজি নিম্নলিখিত দিক থেকে অপটিমাইজ করা যেতে পারে:

-

কনভার্সন লাইন এবং বেস লাইনের প্যারামিটার অপটিমাইজ করা, যাতে ট্রেড করা সম্পদের বৈশিষ্ট্যের সাথে সঙ্গতিপূর্ণ হয়।

-

ক্লাউড ব্যান্ডের প্যারামিটার অপটিমাইজ করা, যাতে ক্লাউড ব্যান্ড দীর্ঘমেয়াদী ট্রেন্ড আরও নির্ভুলভাবে শনাক্ত করতে পারে।

-

স্টপ লস অ্যালগরিদম অপটিমাইজ করা, যেমন ATR ভিত্তিক স্টপ লস বা ডাইনামিক স্টপ লস ব্যবহার করা।

-

অন্যান্য ইন্ডিকেটরের সাথে সিগন্যাল ফিল্টার করে আরও বেশি ফিল্টারিং কন্ডিশন যুক্ত করা, যাতে ভুল এন্ট্রির সম্ভাবনা কমানো যায়।

-

ঝুঁকি-লাভের অনুপাত অপটিমাইজ করে বিভিন্ন সম্পদ ও টাইমফ্রেমের বৈশিষ্ট্যের সাথে খাপ খাওয়ানো।

-

মার্টিংগেল পদ্ধতি ব্যবহার করে পজিশন ম্যানেজমেন্ট করা, যা বিভিন্ন বাজারের ওঠানামার ফ্রিকোয়েন্সির সাথে খাপ খায়।

-

মেশিন লার্নিং পদ্ধতি ব্যবহার করে প্যারামিটার অপটিমাইজ করা, যা আরও স্থিতিশীলতা অর্জন করতে সাহায্য করে।

-

বিভিন্ন ট্রেডিং সময়সীমা সেট করা, নাইট সেশন ও ইন্ট্রাডে সেশনের বাজার বৈশিষ্ট্যের সাথে সমন্বয় করা।

সারসংক্ষেপ

চাও ই স্ট্র্যাটেজি সামগ্রিকভাবে একটি খুব উপযুক্ত কৌশল যা মধ্যম থেকে দীর্ঘমেয়াদী ট্রেন্ড ট্রেডিংয়ের জন্য আদর্শ। এটি চাও ই ইন্ডিকেটর ব্যবহার করে ট্রেন্ডের দিক নির্ণয়ের স্পষ্ট সুবিধা রয়েছে, এবং মূল্যের রিট্রেসমেন্টের সাথে মিলিয়ে এন্ট্রি করায় ভুল এন্ট্রি এড়ানো যায়। প্যারামিটার সেটিংস অপটিমাইজ করে কৌশলটি আরও বেশি সম্পদ ও টাইমফ্রেমে স্থিতিশীল মুনাফা অর্জন করতে সক্ষম হয়। এই কৌশলটি সহজে বোধগম্য এবং অপটিমাইজেশনের অনেক সুযোগ রয়েছে, যা কৌশল গবেষণা ও শেখার জন্য একটি মৌলিক কৌশল হিসেবে ব্যবহারের উপযোগী।

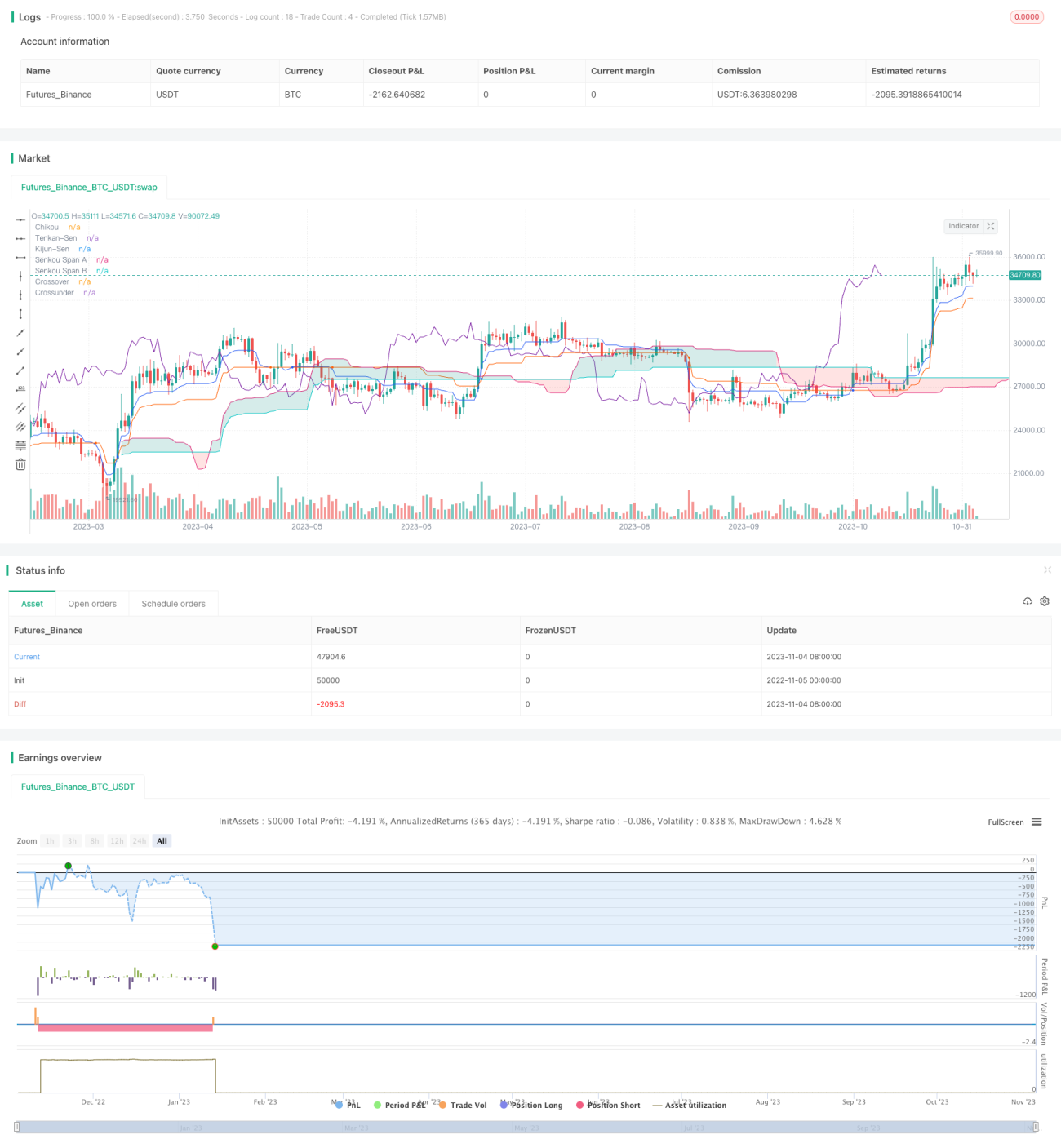

/*backtest

start: 2022-11-05 00:00:00

end: 2023-11-05 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// Strategy based on the the SuperIchi indicator.

//

// Strategy was designed for the purpose of back testing.

// See strategy documentation for info on trade entry logic.- 1