T3 মুভিং এভারেজ এবং ATR এর উপর ভিত্তি করে ট্রেডিং কৌশল

ওভারভিউ

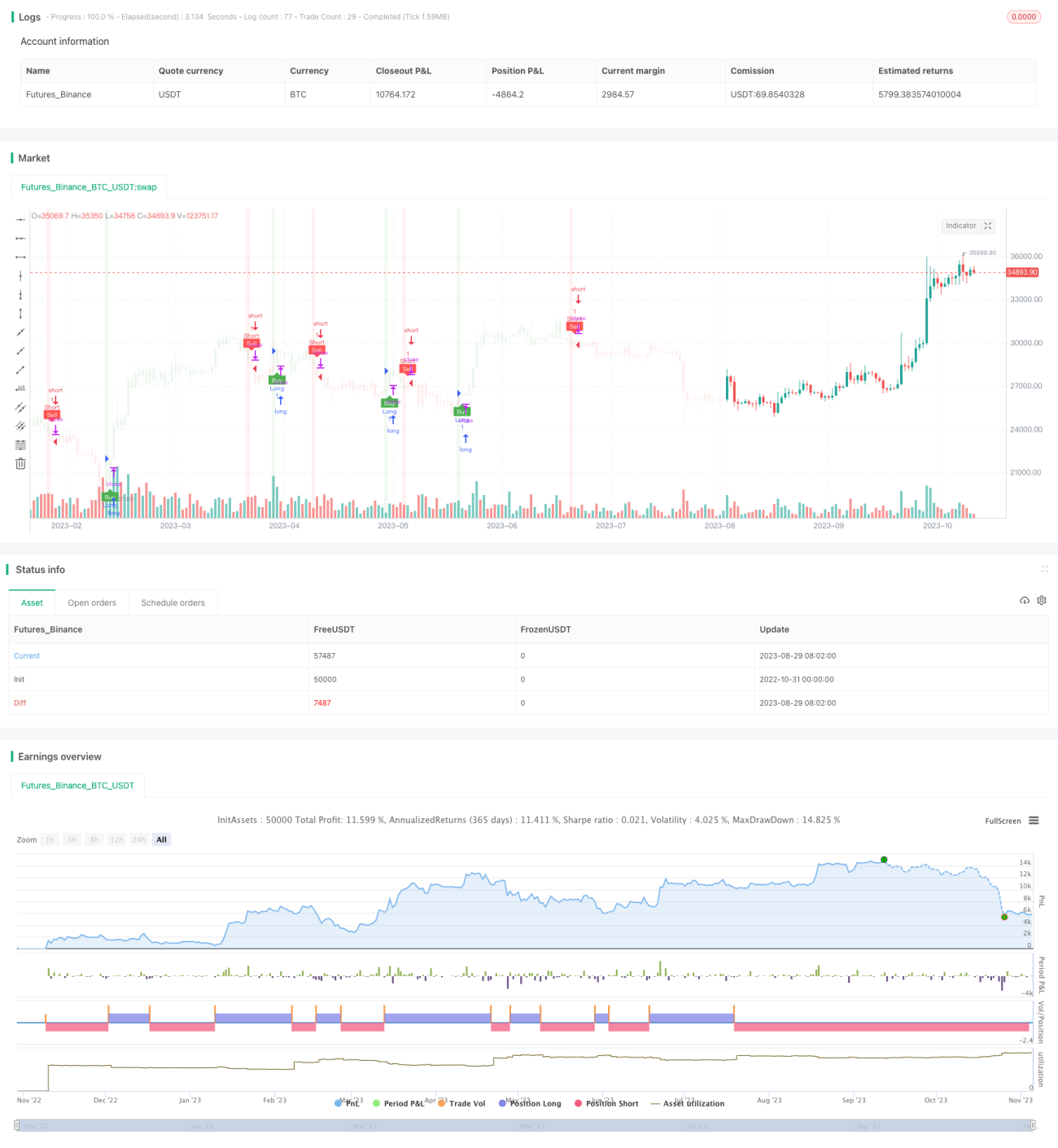

এই কৌশলটি T3 মুভিং এভারেজ, ATR ইন্ডিকেটর এবং হেইকেন আশির সমন্বয় ব্যবহার করে ক্রয় ও বিক্রয় সংকেত চিহ্নিত করে এবং ATR-এর ভিত্তিতে স্টপ লস ও টেক প্রফিট অবস্থান গণনা করে ট্রেন্ড ফলোয়িং ট্রেডিং বাস্তবায়ন করে। কৌশলটির সুবিধা হলো এটি দ্রুত প্রতিক্রিয়া দেখায় এবং একই সাথে ট্রেডিং ঝুঁকি নিয়ন্ত্রণ করে।

মূলনীতি বিশ্লেষণ

ইন্ডিকেটর গণনা

-

T3 মুভিং এভারেজ: একটি মসৃণ প্যারামিটার T3 (ডিফল্ট 100) ব্যবহার করে T3 মুভিং এভারেজ গণনা করা হয়, যা ট্রেন্ডের দিক নির্ধারণে ব্যবহৃত হয়।

-

ATR: গড় প্রকৃত পরিসীমা (ATR) গণনা করা হয়, যা স্টপ লস ও টেক প্রফিট অবস্থানের আকার নির্ধারণে ব্যবহৃত হয়।

-

ATR ট্রেলিং স্টপ: ATR-এর ভিত্তিতে একটি ট্রেলিং স্টপ লাইন গণনা করা হয়, যা দাম পরিবর্তন এবং অস্থিরতা অনুযায়ী সমন্বয় করা যায়, ফলে ট্রেন্ড ফলোয়িং সম্ভব হয়।

ট্রেডিং লজিক

-

ক্রয় সংকেত: যখন ক্লোজিং প্রাইস ATR ট্রেলিং স্টপ লাইনের উপরে উঠে যায় এবং T3 এভারেজের নিচে থাকে, তখন ক্রয় সংকেত তৈরি হয়।

-

বিক্রয় সংকেত: যখন ক্লোজিং প্রাইস ATR ট্রেলিং স্টপ লাইনের নিচে নেমে যায় এবং T3 এভারেজের উপরে থাকে, তখন বিক্রয় সংকেত তৈরি হয়।

-

স্টপ লস ও টেক প্রফিট: পজিশনে প্রবেশের পর, ATR মান এবং ব্যবহারকারীর নির্ধারিত ঝুঁকি-পুরস্কার অনুপাতের ভিত্তিতে স্টপ লস ও টেক প্রফিট মূল্য গণনা করা হয়।

কৌশল প্রবেশ ও প্রস্থান

-

ক্রয়ের পর, স্টপ লস মূল্য = প্রবেশ মূল্য - ATR মান; টেক প্রফিট মূল্য = প্রবেশ মূল্য + (ATR মান × ঝুঁকি-পুরস্কার অনুপাত)।

-

বিক্রয়ের পর, স্টপ লস মূল্য = প্রবেশ মূল্য + ATR মান; টেক প্রফিট মূল্য = প্রবেশ মূল্য - (ATR মান × ঝুঁকি-পুরস্কার অনুপাত)।

-

যখন দাম স্টপ লস বা টেক প্রফিট স্তর স্পর্শ করে, তখন পজিশন বন্ধ করা হয়।

সুবিধা বিশ্লেষণ

দ্রুত প্রতিক্রিয়া

T3 এভারেজের ডিফল্ট প্যারামিটার 100, যা সাধারণ মুভিং এভারেজের তুলনায় বেশি সংবেদনশীল, ফলে দাম পরিবর্তনে দ্রুত সাড়া দেওয়া সম্ভব।

ঝুঁকি নিয়ন্ত্রণ

ATR-ভিত্তিক ট্রেলিং স্টপ বাজারের অস্থিরতা অনুযায়ী দাম ট্র্যাক করতে পারে, ফলে স্টপ লস ভেঙে যাওয়ার ঝুঁকি হ্রাস পায়। স্টপ লস ও টেক প্রফিট অবস্থান ATR-এর উপর ভিত্তি করে হওয়ায় প্রতিটি ট্রেডের ঝুঁকি-পুরস্কার অনুপাত নিয়ন্ত্রণ করা যায়।

ট্রেন্ড ফলোয়িং

ATR ট্রেলিং স্টপ লাইন ট্রেন্ড অনুসরণ করতে সক্ষম, এমনকি দামের স্বল্পমেয়াদী প্রত্যাবর্তনের সময়েও এটি পজিশন বন্ধ করে না, ফলে ভুল সংকেত কম হয়।

প্যারামিটার অপ্টিমাইজেশন সুযোগ

T3 এভারেজ পিরিয়ড এবং ATR পিরিয়ড উভয়ই অপ্টিমাইজ করা যেতে পারে, ফলে বিভিন্ন বাজারের জন্য প্যারামিটার সমন্বয় করে কৌশলের স্থিতিশীলতা বাড়ানো সম্ভব।

ঝুঁকি বিশ্লেষণ

ব্রেকআউট ঝুঁকি

তীব্র বাজারের গতিবিধিতে দাম সরাসরি স্টপ লস লাইন ভেঙে দিয়ে ক্ষতি করতে পারে। ATR পিরিয়ড ও স্টপ দূরত্ব বাড়িয়ে এই ঝুঁকি কমানো যায়।

ট্রেন্ড বিপরীতমুখী হওয়ার ঝুঁকি

ট্রেন্ড বিপরীত হলে, দাম ট্রেলিং স্টপ লাইন অতিক্রম করলে ক্ষতি হতে পারে। অন্যান্য ইন্ডিকেটরের সাহায্যে ট্রেন্ডের দিক নির্ধারণ করে বিপরীতমুখী পয়েন্টের কাছে ট্রেডিং এড়ানো যায়।

প্যারামিটার অপ্টিমাইজেশন ঝুঁকি

প্যারামিটার অপ্টিমাইজেশনের জন্য প্রচুর ঐতিহাসিক ডেটা প্রয়োজন, ফলে অত্যধিক অপ্টিমাইজেশনের ঝুঁকি থাকে। একক ডেটাসেটের উপর নির্ভর না করে একাধিক বাজার ও টাইমফ্রেমের সমন্বয়ে প্যারামিটার অপ্টিমাইজ করা উচিত।

অপ্টিমাইজেশন দিকনির্দেশনা

-

বিভিন্ন T3 এভারেজ পিরিয়ড প্যারামিটার পরীক্ষা করে সংবেদনশীলতা ও স্থিতিশীলতার মধ্যে সর্বোত্তম সমন্বয় খুঁজে বের করা।

-

ATR পিরিয়ড প্যারামিটার পরীক্ষা করে ঝুঁকি নিয়ন্ত্রণ ও ট্রেন্ড ক্যাপচারের মধ্যে সর্বোত্তম ভারসাম্য খুঁজে বের করা।

-

RSI, MACD ইত্যাদি ইন্ডিকেটরের সাথে সমন্বয় করে ট্রেন্ড বিপরীতমুখী পয়েন্টে ভুল ট্রেডিং এড়ানো।

-

সর্বোত্তম প্যারামিটার প্রশিক্ষণের জন্য মেশিন লার্নিং পদ্ধতি ব্যবহার করে ম্যানুয়াল অপ্টিমাইজেশনের সীমাবদ্ধতা কমানো।

-

পজিশন ম্যানেজমেন্ট কৌশল যুক্ত করে ঝুঁকি আরও ভালোভাবে নিয়ন্ত্রণ করা।

সারসংক্ষেপ

এই কৌশলটি T3 মুভিং এভারেজ ও ATR ইন্ডিকেটরের সুবিধাগুলো একীভূত করে, যা দ্রুত দাম পরিবর্তনে সাড়া দেওয়ার পাশাপাশি ঝুঁকি নিয়ন্ত্রণ করে। প্যারামিটার অপ্টিমাইজেশন ও অন্যান্য ইন্ডিকেটরের সাথে সমন্বয়ের মাধ্যমে কৌশলের স্থিতিশীলতা ও ট্রেডিং দক্ষতা আরও বাড়ানো যায়। তবে ট্রেডারদের বিপরীতমুখী ও ব্রেকআউটের ঝুঁকির প্রতি সচেতন থাকতে হবে এবং ব্যাকটেস্ট ফলাফলের উপর অতিরিক্ত নির্ভর করা এড়িয়ে চলতে হবে।

- 1