Z-দূরত্ব ভিত্তিক VWAP কৌশল

সারসংক্ষেপ

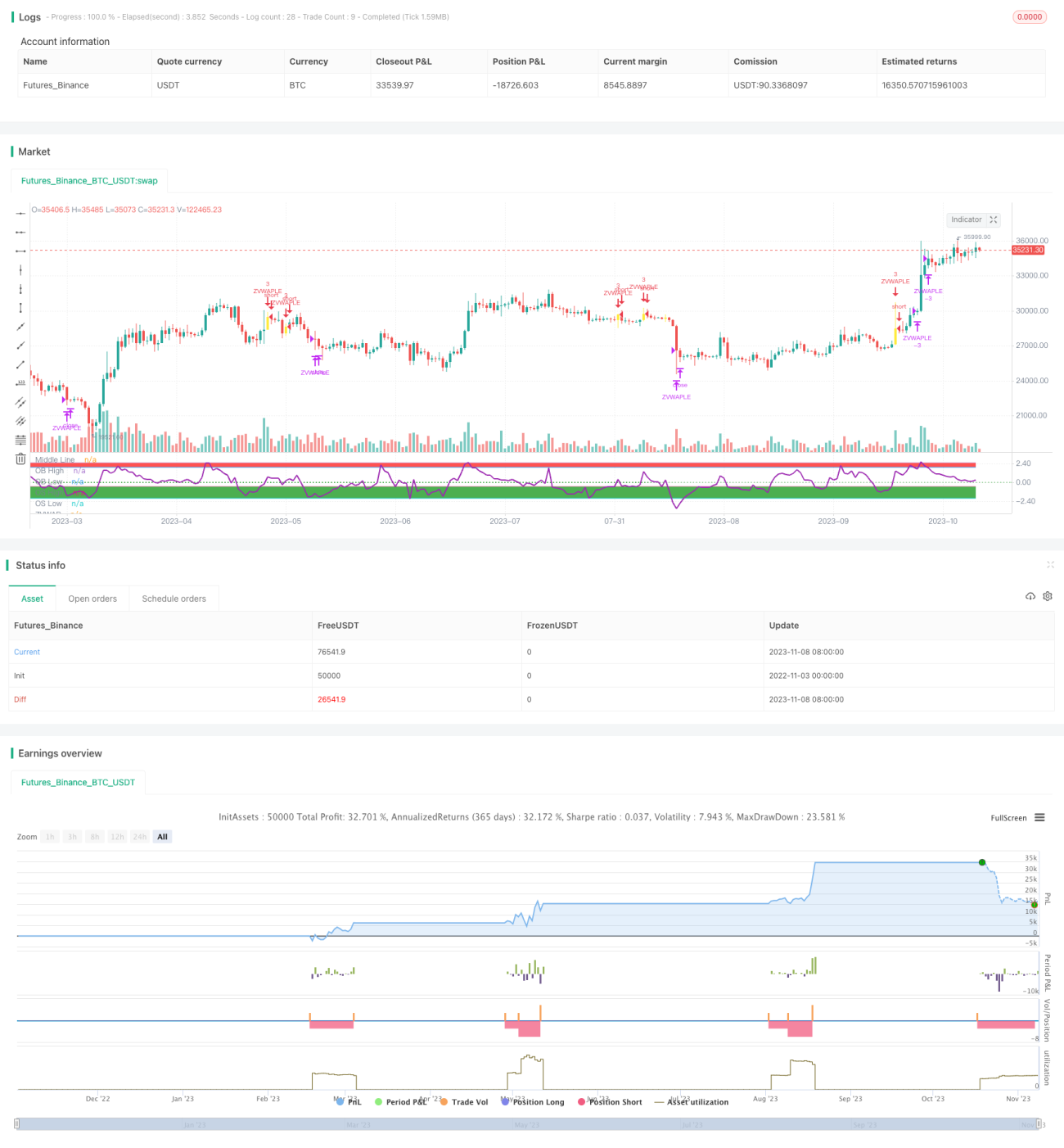

এই কৌশলটি LazyBear-এর Z দূরত্ব VWAP নির্দেশকের উপর ভিত্তি করে তৈরি। দাম ও VWAP-এর মধ্যে Z দূরত্ব গণনা করে এটি নির্ধারণ করে যে বাজারটি অতিরিক্ত কেনা বা বিক্রি হয়েছে কিনা এবং প্রবেশ ও প্রস্থানের সিদ্ধান্ত নেয়। কৌশলটিতে EMA মুভিং এভারেজ এবং Z দূরত্ব 0-এ ফিরে আসার শর্ত যুক্ত করা হয়েছে, যা কিছু নয়েজ সংকেত ফিল্টার করতে সাহায্য করে।

কৌশলের নীতি

- VWAP-এর মান গণনা করা।

- দাম ও VWAP-এর মধ্যে Z দূরত্ব গণনা করা।

- অতিরিক্ত কেনার রেখা (2.5) এবং অতিরিক্ত বিক্রির রেখা (-0.5) নির্ধারণ করা।

- যখন দ্রুত রেখা ধীর রেখার চেয়ে বেশি হয়, Z দূরত্ব অতিরিক্ত বিক্রির রেখার নিচে থাকে এবং Z দূরত্ব 0 রেখা অতিক্রম করে উপরে যায়, তখন লং পজিশন খোলা হয়।

- যখন Z দূরত্ব অতিরিক্ত কেনার রেখা অতিক্রম করে, তখন পজিশন বন্ধ করা হয়।

- স্টপ-লস লজিক যুক্ত করা হয়েছে।

মূল ফাংশন:

- calc_zvwap: দাম ও VWAP-এর মধ্যে Z দূরত্ব গণনা করে।

- VWAP মান: vwap(hlc3)

- দ্রুত রেখা: ema(close, fastEma)

- ধীর রেখা: ema(close, slowEma)

সুবিধার বিশ্লেষণ

- Z দূরত্ব ব্যবহার করে অতিরিক্ত কেনা/বিক্রি আরও সহজে শনাক্ত করা যায়।

- EMA-এর সাথে একত্রিত করে মিথ্যা ব্রেকআউট ফিল্টার করা যায় এবং ফাঁদে পড়ার ঝুঁকি কমানো যায়।

- পজিশনে যোগ করার (এড) সুযোগ থাকে, যা ট্রেন্ড থেকে লাভ করতে সাহায্য করে।

- স্টপ-লস লজিক থাকায় ঝুঁকি নিয়ন্ত্রণ করা যায়।

ঝুঁকি বিশ্লেষণ

- প্যারামিটার সঠিকভাবে সেট করা প্রয়োজন, যেমন অতিরিক্ত কেনা/বিক্রির রেখার অবস্থান, EMA পিরিয়ড ইত্যাদি।

- Z দূরত্ব নির্দেশকে কিছুটা পিছিয়ে থাকে, তাই গুরুত্বপূর্ণ কেনা/বেচার পয়েন্ট মিস হতে পারে।

- পজিশনে যোগ করার অনুমতি থাকায় ক্ষতির ঝুঁকি বেড়ে যায়।

- স্টপ-লসের অবস্থান সঠিকভাবে নির্ধারণ করতে হবে।

সমাধান:

- ব্যাকটেস্টের মাধ্যমে প্যারামিটার অপ্টিমাইজ করা।

- অতিরিক্ত নির্দেশক যুক্ত করে সংকেত ফিল্টার করা।

- পজিশন যোগ করার শর্ত সঠিকভাবে নির্ধারণ করা।

- স্টপ-লস অবস্থান গতিশীলভাবে সামঞ্জস্য করা।

অপ্টিমাইজেশনের দিকনির্দেশনা

- EMA পিরিয়ড প্যারামিটার অপ্টিমাইজ করা।

- অতিরিক্ত কেনা/বিক্রি নির্ণয়ের বিভিন্ন মান পরীক্ষা করা।

- অন্যান্য নির্দেশক যুক্ত করে সংকেতের নয়েজ কমানো।

- বিভিন্ন স্টপ-লস পদ্ধতি পরীক্ষা করা।

- প্রবেশ, পজিশন যোগ এবং স্টপ-লস লজিক অপ্টিমাইজ করা।

উপসংহার

এই কৌশলটি Z দূরত্ব ব্যবহার করে দাম ও VWAP-এর সম্পর্ক নির্ণয় করে এবং EMA-এর সাহায্যে নয়েজ ফিল্টার করে ট্রেন্ডের সুযোগ ধরে। কৌশলটি ট্রেন্ড অনুসরণ করতে পজিশন যোগ করার অনুমতি দেয় এবং ঝুঁকি নিয়ন্ত্রণের জন্য স্টপ-লস সেট করে। প্যারামিটার অপ্টিমাইজেশন ও অন্যান্য নির্দেশক যুক্ত করলে কৌশলের স্থিতিশীলতা বাড়ানো যায়। তবে Z দূরত্ব নির্দেশকে পিছিয়ে থাকার সমস্যা রয়েছে, যা অপ্টিমাইজেশনের সময় বিবেচনা করতে হবে। সামগ্রিকভাবে, কৌশলটি সরল ও পরিষ্কার যুক্তিতে ট্রেন্ড ধরে এবং পর্যাপ্ত অপ্টিমাইজেশনের পর এটি একটি কার্যকর ট্রেন্ড ফলোয়িং কৌশল হয়ে উঠতে পারে।

- 1