প্রবণতা বিপরীত ট্রেলিং স্টপ কৌশল

সারসংক্ষেপ

কৌশলটি ট্রেন্ড রিভার্সাল ইন্ডিকেটরের উপর ভিত্তি করে তৈরি, যা ট্রেন্ড ট্র্যাকিং স্টপ লস মেকানিজমের সাথে মিলিত হয়ে ট্রেন্ডিং মার্কেটে ট্রেন্ড অনুসরণ করে এবং রেঞ্জ বাউন্ড মার্কেটে লোকসান কমাতে সহায়তা করে।

কৌশলের নীতি

কৌশলটি প্রধান ট্রেন্ড নির্ধারণের সূচক হিসেবে হাল মুভিং এভারেজ ব্যবহার করে। যখন দাম হাল এভারেজের উপরে উঠে যায়, তখন লং পজিশন নেওয়া হয়; যখন দাম হাল এভারেজের নিচে নেমে যায়, তখন শর্ট পজিশন নেওয়া হয়। একই সাথে, ট্রেন্ড নিশ্চিত করতে ম্যাকগিনলি মুভিং এভারেজ ব্যবহার করা হয়।

পজিশন খোলার পর, যদি দাম বিপরীত দিকে চলে যায়, অর্থাৎ হাল এভারেজের ক্রসওভার যাচাই হয়, তাহলে ট্রেন্ড পরিবর্তনের লজিক প্রয়োগ করে বর্তমান পজিশন বন্ধ করা হয়।

কৌশলটিতে ট্রেন্ড ট্র্যাকিং স্টপ লস মেকানিজমও অন্তর্ভুক্ত রয়েছে। পজিশন খোলার পর ATR-এর ভিত্তিতে ডায়নামিক স্টপ লস লেভেল নির্ধারণ করা হয়। দামের গতিবিধির সাথে সাথে স্টপ লস লাইনও ডায়নামিকভাবে সামঞ্জস্য হয়, যা লাভের ট্রেলিং স্টপ লস নিশ্চিত করে।

কৌশলের সুবিধা

- হাল মুভিং এভারেজ ব্যবহার করে ট্রেন্ড রিভার্সাল পয়েন্ট চিহ্নিত করা; হাল এভারেজ ব্রেকআউট সিগন্যালের প্রতি অত্যন্ত সংবেদনশীল

- ম্যাকগিনলি মুভিং এভারেজের সাথে ট্রেন্ড নিশ্চিতকরণ মিথ্যা ব্রেকআউট的部分 ফিল্টার করতে সহায়তা করে

- ডায়নামিক ট্রেলিং স্টপ লস মেকানিজম ব্যবহার করে, যা বাজারের অস্থিরতা অনুযায়ী স্টপ লসের আকার সামঞ্জস্য করতে পারে এবং কার্যকরভাবে লোকসান নিয়ন্ত্রণ করে

- হাল এভারেজ যাচাইয়ের সময় ট্রেন্ড রিভার্সালে দ্রুত সাড়া দেয়, যাতে লোকসান আরও বাড়তে না পারে

- বিভিন্ন প্যারামিটার কম্বিনেশন সহজেই পরিবর্তন করে পরীক্ষা করা যায় এবং সর্বোত্তম প্যারামিটার খুঁজে পাওয়া যায়

ঝুঁকি ও সমাধান

-

রেঞ্জ বাউন্ড বাজারে স্টপ লস ট্রিগার হওয়ার সম্ভাবনা থাকে

- স্টপ লসের আকার适当 বাড়ানো যেতে পারে এবং স্টপ লস বাফার যোগ করা যেতে পারে

-

তীব্র বাজার আন্দোলনে ট্রেলিং স্টপ লস দামের পরিবর্তনের সাথে তাল মেলাতে পারে না

- স্মুথিং পিরিয়ড সংক্ষিপ্ত করে স্টপ লসকে দ্রুত দামের সাথে সামঞ্জস্য করা যেতে পারে

-

মিথ্যা ব্রেকআউট অপ্রয়োজনীয় লোকসানের কারণ হতে পারে

- অন্যান্য ইন্ডিকেটর যোগ করে নিশ্চিত হওয়া যায়, যাতে মিথ্যা ব্রেকআউট এড়ানো যায়

-

প্যারামিটার যথাযথ না হলে কৌশলের পারফরম্যান্স খারাপ হতে পারে

- বিভিন্ন বাজার চক্রে ব্যাকটেস্ট করে সর্বোত্তম প্যারামিটার খুঁজে বের করা যেতে পারে

অপ্টিমাইজেশনের ধারণা

-

অন্যান্য ইন্ডিকেটর যেমন ক্যান্ডেলস্টিক প্যাটার্ন, বলিঞ্জার ব্যান্ড, আরএসআই ইত্যাদির সাথে মিলিয়ে সিগন্যালের গুণগত মান উন্নত করা যায়

-

বিভিন্ন পণ্য, সময়কালের প্যারামিটার অপ্টিমাইজ করে সেরা প্যারামিটার কম্বিনেশন খুঁজে বের করা যায়

-

মেশিন লার্নিং ইত্যাদির মাধ্যমে প্যারামিটার অ্যাডাপটিভ অপ্টিমাইজেশন চেষ্টা করা যেতে পারে

-

স্টপ লস অ্যালগরিদম অপ্টিমাইজ করে স্টপ লস নিশ্চিত করার পাশাপাশি অপ্রয়োজনীয় স্টপ লস কমানো যায়

-

মানি ম্যানেজমেন্টের সাথে পজিশন ম্যানেজমেন্ট কৌশল অপ্টিমাইজ করা যায়

-

অটো টেক-প্রফিট মেকানিজম যোগ করার বিষয়টি বিবেচনা করা যেতে পারে

উপসংহার

সামগ্রিকভাবে কৌশলটি একটি মোটামুটি স্থিতিশীল ট্রেন্ড ট্র্যাকিং কৌশল। ফিক্সড স্টপ লসের তুলনায়, এটি ডায়নামিক স্টপ লস মেকানিজম ব্যবহার করে, যা বাজারের অস্থিরতা অনুযায়ী স্টপ লসের আকার সামঞ্জস্য করতে পারে এবং স্টপ লসে ফেঁসে যাওয়ার সম্ভাবনা কমায়। একই সাথে, হাল এভারেজ এবং ট্রেন্ড পরিবর্তনের লজিক প্রবর্তনের ফলে ট্রেন্ড রিভার্সালে দ্রুত সাড়া দেওয়া যায়। তবে কৌশলটির কিছু নির্দিষ্ট ঝুঁকিও রয়েছে, যেমন রেঞ্জ বাউন্ড বাজারে স্টপ লসের ঝুঁকি, মিথ্যা ব্রেকআউটের ঝুঁকি ইত্যাদি। ইন্ডিকেটর প্যারামিটার, স্টপ লস অ্যালগরিদম, পজিশন ম্যানেজমেন্ট ইত্যাদি আরও অপ্টিমাইজ করলে কৌশলটি বিভিন্ন বাজারে আরও স্থিতিশীল পারফরম্যান্স অর্জন করতে পারে।

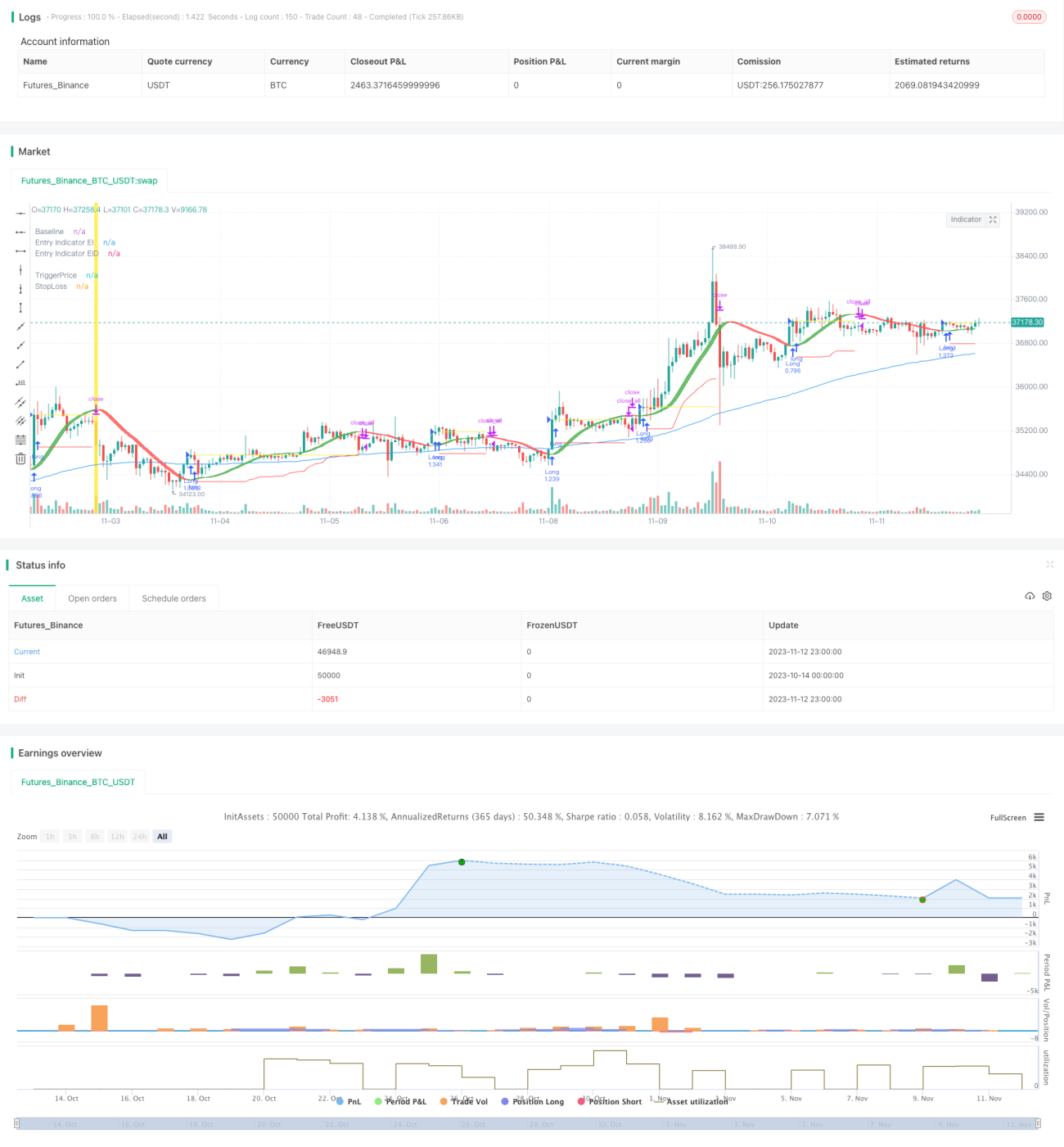

/*backtest

start: 2023-10-14 00:00:00

end: 2023-11-13 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © Milleman

//@version=4

strategy("MilleMachine", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.06)

- 1