গড় প্রত্যাবর্তন মোমেন্টাম কৌশল

সারসংক্ষেপ

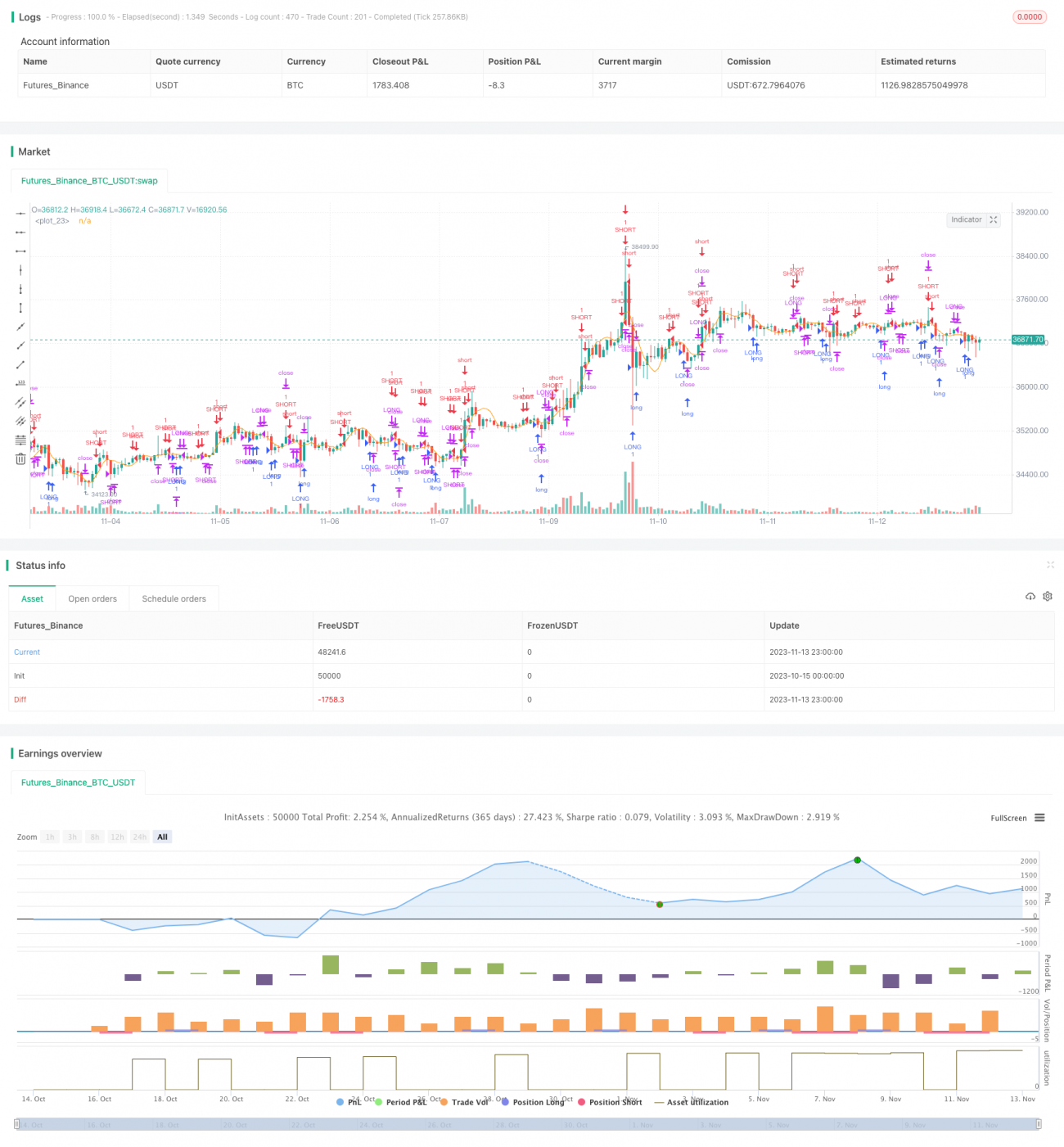

মিন রিভার্সন মোমেন্টাম কৌশল একটি ট্রেন্ড ট্রেডিং কৌশল যা স্বল্পমেয়াদী মূল্যের গড় অনুসরণ করে। এটি মিন রিভার্সন সূচক এবং মোমেন্টাম সূচককে একত্রিত করে বাজারের মধ্যমেয়াদী ট্রেন্ড নির্ণয় করে।

কৌশলের নীতি

কৌশলটি প্রথমে মূল্যের মিন রিভার্সন লাইন এবং স্ট্যান্ডার্ড ডেভিয়েশন গণনা করে। তারপর Upper Threshold এবং Lower Threshold প্যারামিটার দ্বারা নির্ধারিত থ্রেশহোল্ডের সাথে মিলিয়ে, মূল্য মিন রিভার্সন লাইন থেকে এক স্ট্যান্ডার্ড ডেভিয়েশনের বাইরে গেছে কিনা তা গণনা করে। যদি বাইরে যায়, তাহলে ট্রেডিং সিগন্যাল তৈরি হয়।

লং সিগন্যালের জন্য, মূল্য মিন রিভার্সন লাইন থেকে এক স্ট্যান্ডার্ড ডেভিয়েশন নিচে হতে হবে, ক্লোজ মূল্য LENGTH পিরিয়ডের SMA লাইনের নিচে হতে হবে, এবং TREND SMA লাইনের উপরে হতে হবে, এই তিনটি শর্ত পূরণ হলে লং পজিশন খোলা হবে। পজিশন বন্ধ করার শর্ত হলো মূল্য LENGTH পিরিয়ডের SMA লাইনের উপরে ক্রস করা।

শর্ট সিগন্যালের জন্য, মূল্য মিন রিভার্সন লাইন থেকে এক স্ট্যান্ডার্ড ডেভিয়েশন উপরে হতে হবে, ক্লোজ মূল্য LENGTH পিরিয়ডের SMA লাইনের উপরে হতে হবে, এবং TREND SMA লাইনের নিচে হতে হবে, এই তিনটি শর্ত পূরণ হলে শর্ট পজিশন খোলা হবে। পজিশন বন্ধ করার শর্ত হলো মূল্য LENGTH পিরিয়ডের SMA লাইনের নিচে ক্রস করা।

কৌশলটি একই সাথে Percent Profit Target এবং Percent Stop Loss ব্যবহার করে লাভ টার্গেট এবং স্টপ লস ম্যানেজমেন্ট বাস্তবায়ন করে।

এক্সিট পদ্ধতি হিসেবে মুভিং এভারেজ ব্রেকআউট বা লিনিয়ার রিগ্রেশন ব্রেকআউট নির্বাচন করা যায়।

লং এবং শর্ট উভয় দিকের ট্রেডিং, ট্রেন্ড ফিল্টারিং, লাভ টার্গেট এবং স্টপ লস ইত্যাদির সংমিশ্রণের মাধ্যমে বাজারের মধ্যমেয়াদী ট্রেন্ড নির্ণয় এবং অনুসরণ করা সম্ভব হয়েছে।

কৌশলের সুবিধা

-

মিন রিভার্সন সূচক কার্যকরভাবে মূল্য মান কেন্দ্র থেকে বিচ্যুত হয়েছে কিনা তা নির্ণয় করতে পারে

-

মোমেন্টাম সূচক SMA স্বল্পমেয়াদী বাজারের শব্দ ফিল্টার করতে পারে

-

লং এবং শর্ট উভয় দিকের ট্রেডিং, সামগ্রিকভাবে ট্রেন্ড সুযোগ ধারণ করতে পারে

-

লাভ টার্গেট এবং স্টপ লস প্রক্রিয়া কার্যকরভাবে ঝুঁকি নিয়ন্ত্রণ করতে পারে

-

নির্বাচনযোগ্য এক্সিট পদ্ধতি বাজারের পরিবেশের সাথে নমনীয়ভাবে খাপ খাইয়ে নিতে পারে

-

সম্পূর্ণ ট্রেন্ড ট্রেডিং কৌশল, ভালোভাবে মধ্যমেয়াদী ট্রেন্ড ধারণ করতে পারে

কৌশলের ঝুঁকি

-

মিন রিভার্সন সূচক প্যারামিটার সেটিংয়ের প্রতি সংবেদনশীল, ভুল থ্রেশহোল্ড নির্ধারণ ভুয়া সিগন্যালের কারণ হতে পারে

-

বড় ওঠানামার বাজারে স্টপ লস খুব ঘন ঘন ট্রিগার হতে পারে

-

ওঠানামা ট্রেন্ডে লেনদেনের ফ্রিকোয়েন্সি বেশি হতে পারে, যা ট্রেডিং ফি এবং স্লিপেজ ঝুঁকি বাড়ায়

-

ট্রেডিং যন্ত্রের তারল্য কম হলে স্লিপেজ নিয়ন্ত্রণ আদর্শ নাও হতে পারে

-

লং এবং শর্ট উভয় দিকের ট্রেডিং ঝুঁকি বেশি, সতর্কতার সাথে তহবিল ব্যবস্থাপনা প্রয়োজন

প্যারামিটার অপ্টিমাইজেশন, স্টপ লস পদ্ধতি সমন্বয়, তহবিল ব্যবস্থাপনা ইত্যাদি পদ্ধতির মাধ্যমে এই ঝুঁকিগুলি নিয়ন্ত্রণ করা যেতে পারে।

কৌশল অপ্টিমাইজেশনের দিকনির্দেশনা

-

মিন রিভার্সন এবং মোমেন্টাম সূচকের প্যারামিটার সেটিং অপ্টিমাইজ করা, যাতে তা বিভিন্ন যন্ত্রের বৈশিষ্ট্যের সাথে আরও সামঞ্জস্যপূর্ণ হয়

-

ট্রেন্ড নির্ণয়ের সূচক যোগ করা, ট্রেন্ড শনাক্ত করার ক্ষমতা বাড়ানো

-

স্টপ লস কৌশল অপ্টিমাইজ করা, যাতে তা বাজারের বড় ওঠানামার সাথে আরও খাপ খাইয়ে নিতে পারে

-

পজিশন ম্যানেজমেন্ট মডিউল যোগ করা, বাজারের অবস্থা অনুযায়ী পজিশনের আকার সমন্বয় করা

-

আরও ঝুঁকি নিয়ন্ত্রণ মডিউল যোগ করা, যেমন সর্বোচ্চ ড্রডাউন নিয়ন্ত্রণ, নেট ভ্যালু কার্ভ নিয়ন্ত্রণ ইত্যাদি

-

মেশিন লার্নিং পদ্ধতি যুক্ত করার কথা বিবেচনা করা, যাতে কৌশলের প্যারামিটার স্বয়ংক্রিয়ভাবে অপ্টিমাইজ হয়

সারসংক্ষেপ

সারসংক্ষেপে, মিন রিভার্সন মোমেন্টাম কৌশলটি সরল ও কার্যকর সূচক ডিজাইনের মাধ্যমে মধ্যমেয়াদী মান ফিরে আসার ট্রেন্ড ধারণ করতে সক্ষম হয়েছে। কৌশলটির শক্তিশালী অভিযোজনযোগ্যতা এবং সার্বজনীনতা রয়েছে, তবে কিছু ঝুঁকিও রয়েছে। ক্রমাগত অপ্টিমাইজেশন এবং অন্যান্য কৌশলের সাথে সমন্বয়ের মাধ্যমে আরও ভালো কর্মক্ষমতা অর্জন করা সম্ভব। কৌশলটি সামগ্রিকভাবে সম্পূর্ণ এবং এটি একটি বিবেচনাযোগ্য ট্রেন্ড ট্রেডিং পদ্ধতি।

/*backtest

start: 2023-10-15 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © GlobalMarketSignals

//@version=4- 1