বহু-সূচক ট্রেন্ড অনুসরণ কৌশল

সারসংক্ষেপ

এই কৌশলটি ৩ টি ওপেন সোর্স ইন্ডিকেটরকে একত্রিত করে একাধিক টাইমফ্রেমে ট্রেন্ড নির্ধারণ করে এবং স্টপ লস ও টেক প্রফিট সেট করে লাভ লক করতে সহায়তা করে। বিশেষ করে, কৌশলটি স্বল্পমেয়াদী ট্রেন্ডের দিক নির্ধারণের জন্য AK MACD BB ইন্ডিকেটর ব্যবহার করে, কিছু ভুয়া সিগন্যাল ফিল্টার করার জন্য SSL ইন্ডিকেটর ব্যবহার করে এবং অবশেষে ভলিউম ইন্ডিকেটর VSF ব্যবহার করে প্রকৃত ক্রয়-বিক্রয় চাপ নির্ধারণ করে এন্ট্রির সময় নির্ধারণ করে। একইসাথে, কৌশলটি লাভ লক করতে পূর্বনির্ধারিত স্টপ লস ও টেক প্রফিট পয়েন্ট সেট করে, যা একটি একক ট্রেডের ক্ষতির ঝুঁকি উল্লেখযোগ্যভাবে হ্রাস করে।

কৌশলের মূলনীতি

-

AK MACD BB ইন্ডিকেটর

এই ইন্ডিকেটরটি MACD ইন্ডিকেটরে বলিঙ্গার ব্যান্ড প্রয়োগ করে। MACD ইন্ডিকেটর লাইন বলিঙ্গার ব্যান্ডের উপরের ব্যান্ড ভেঙে গেলে ক্রয় সিগন্যাল এবং নিচের ব্যান্ড ভেঙে গেলে বিক্রয় সিগন্যাল তৈরি হয়।

-

SSL ইন্ডিকেটর

SSL ইন্ডিকেটর মূল্য মুভিং এভারেজ ভেঙেছে কিনা তা নির্ধারণ করে এবং রিটেস্ট সিগন্যাল শনাক্ত করে। মূল্য মুভিং এভারেজের উপরে উঠলে এবং SSL ইন্ডিকেটর নীল হলে এটি ঊর্ধ্বমুখী ট্রেন্ড, আর মূল্য মুভিং এভারেজের নিচে নামলে এবং SSL ইন্ডিকেটর লাল হলে এটি নিম্নমুখী ট্রেন্ড নির্দেশ করে এবং ট্রেডিং সিগন্যাল তৈরি করে।

-

VSF ইন্ডিকেটর

VSF ইন্ডিকেটর ক্রেতা ও বিক্রেতার শক্তি নির্ধারণ করে। কৌশলটি শুধুমাত্র তখনই সিগন্যাল দেয় যখন ক্রেতা বা বিক্রেতার শক্তি ৫০% এর বেশি হয়, যাতে অকার্যকর ব্রেকআউট এড়ানো যায়।

-

স্টপ লস ও টেক প্রফিট

কৌশলটিতে ১.৫ গুণ থেকে ৩ গুণ পর্যন্ত ব্যবধানে ৪ স্তরের প্রগ্রেসিভ টেক প্রফিট রয়েছে। একইসাথে ২% ফিক্সড স্টপ লস সেট করা আছে, যা একটি একক ট্রেডের সর্বোচ্চ ক্ষতি কার্যকরভাবে নিয়ন্ত্রণ করে।

সুবিধা বিশ্লেষণ

-

একাধিক ইন্ডিকেটরের সমন্বয়, নির্ভুল সিদ্ধান্ত

বিভিন্ন ইন্ডিকেটরের মাধ্যমে একাধিক টাইমফ্রেমের ট্রেন্ড নির্ধারণ করে ভুয়া সিগন্যাল ফিল্টার করা যায় এবং সিদ্ধান্ত আরও নির্ভুল হয়।

-

স্বয়ংক্রিয় টেক প্রফিট ও স্টপ লস, ঝুঁকি নিয়ন্ত্রণযোগ্য

কৌশলে অন্তর্নির্মিত টেক প্রফিট ও স্টপ লস সেটিংস একটি একক ট্রেডের ক্ষতি প্রায় ২% এ সীমাবদ্ধ করতে পারে, বড় ক্ষতি এড়াতে সহায়তা করে।

-

ব্যাকটেস্ট ডেটা চমৎকার

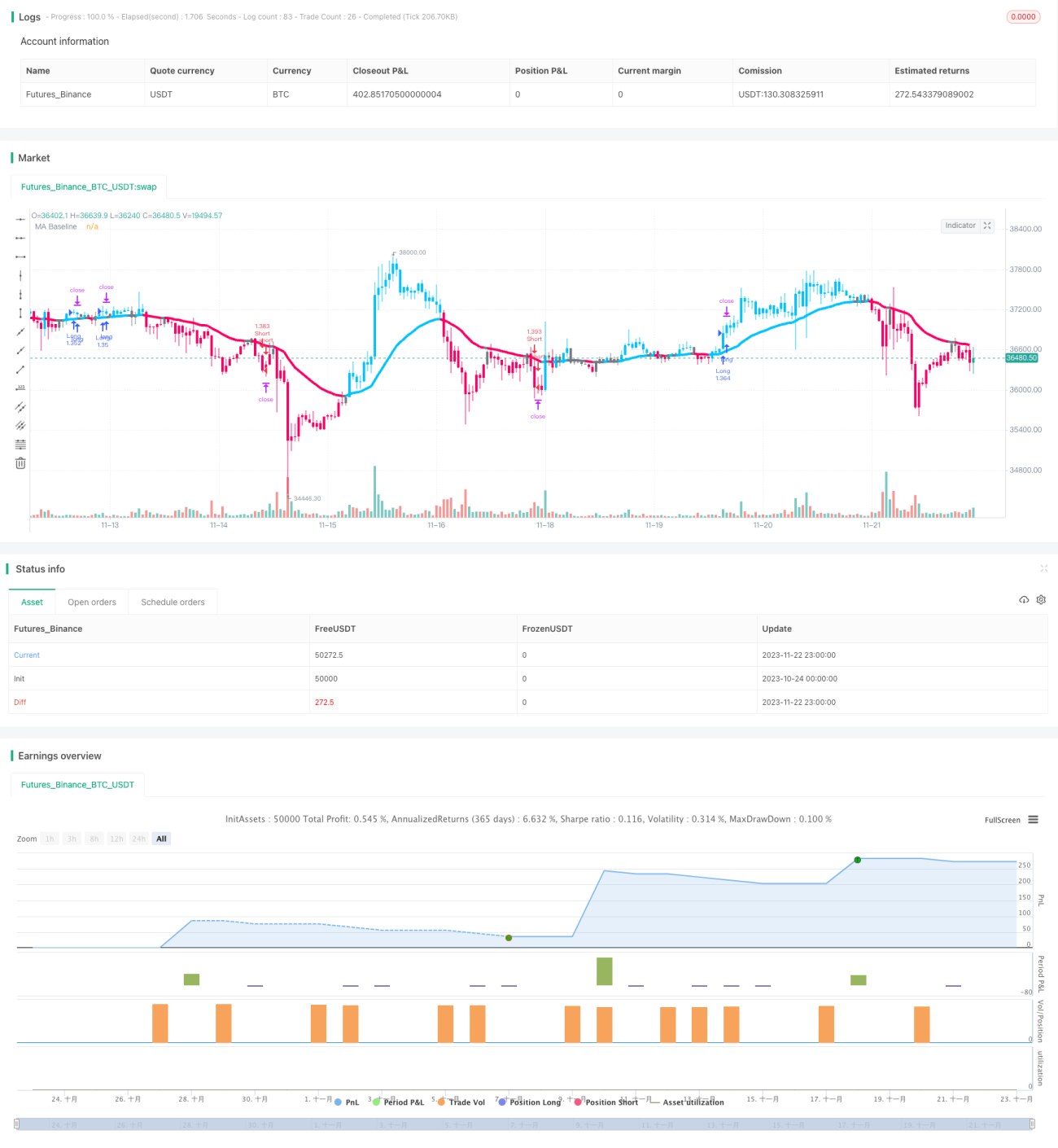

প্রকাশকের ব্যাকটেস্ট অনুযায়ী, ১০০ টি ট্রেডের মধ্যে ৭৪% লাভজনক ট্রেড এবং মোট লাভ ৪২৭%।

ঝুঁকি ও প্রতিকার বিশ্লেষণ

-

বাজারের তীব্র ওঠানামার ঝুঁকি

বড় রেঞ্জে সাইডওয়ে মুভমেন্টের সময় কয়েকবার ছোট ছোট ক্ষতি হতে পারে। এই ক্ষেত্রে ফিক্সড স্টপ লসের সীমা সামঞ্জস্য করা বা ট্রেডিং বন্ধ রাখা যেতে পারে।

-

লং/শর্ট সীমাবদ্ধতার ঝুঁকি

বর্তমানে কৌশলটি লং এবং শর্ট উভয়ই করতে পারে। যদি শুধুমাত্র লং বা শুধুমাত্র শর্ট করার সীমাবদ্ধতা দেওয়া হয়, তাহলে লাভের সুযোগ অর্ধেক কমে যাবে।

-

ট্রেডিং সময়ের ঝুঁকি

কৌশলটি ৫ মিনিটের ডেটা ব্যবহার করে সিদ্ধান্ত নেয়। যদি একটি ট্রেডিং সেশনে কয়েক ঘন্টার ডেটা থাকে, তাহলে নমুনার পরিমাণ অপর্যাপ্ত হতে পারে এবং সিগন্যাল নির্ভরযোগ্য নাও হতে পারে।

কৌশল উন্নতির দিকনির্দেশনা

-

স্টপ লস ও টেক প্রফিট প্যারামিটার অপ্টিমাইজ করা

বিভিন্ন স্টপ লস ও টেক প্রফিট লেভেল পরীক্ষা করে সর্বোত্তম প্যারামিটার খুঁজে বের করা যেতে পারে। খুব ছোট স্টপ লস কার্যকরভাবে ঝুঁকি নিয়ন্ত্রণ করতে পারে না, আবার খুব বড় স্টপ লস বড় লাভ মিস করতে পারে।

-

স্বয়ংক্রিয় পজিশন অ্যাডজাস্টমেন্ট যোগ করা

লাভ লক করার জন্য ট্রেইলিং স্টপ লস বা মুভিং স্টপ লস সেট করা যেতে পারে। অথবা নির্দিষ্ট শর্তে বেশি লাভের জন্য পজিশন বাড়ানো যেতে পারে।

-

অন্যান্য ইন্ডিকেটরের সাথে সংযুক্ত করা

বিভিন্ন ইন্ডিকেটরের সমন্বয় পরীক্ষা করে দেখা যেতে পারে কোন কম্বিনেশন সবচেয়ে ভালো কাজ করে। আরও ইন্ডিকেটর যুক্ত করে ক্রস-ভেরিফিকেশন করা যেতে পারে।

-

প্যারামিটার অপ্টিমাইজেশন

বিভিন্ন প্যারামিটার দিয়ে ব্যাকটেস্ট করে প্যারামিটার অপ্টিমাইজেশনের দিক খুঁজে বের করা যেতে পারে। এই কৌশলে বলিঙ্গার ব্যান্ডের প্যারামিটার বা মুভিং এভারেজের প্যারামিটার পরিবর্তন করলে আরও ভালো ফলাফল পাওয়া যেতে পারে।

সারসংক্ষেপ

এই কৌশলটি একাধিক ইন্ডিকেটর একত্রিত করে ট্রেন্ডের দিক নির্ধারণ করে এবং স্বয়ংক্রিয় টেক প্রফিট ও স্টপ লস সেট করে শক্তিশালী ট্রেন্ডে লাভ করতে সক্ষম এবং একক ট্রেডের ক্ষতি খুব ছোট পরিসরে সীমাবদ্ধ রাখে। প্রকাশকের ব্যাকটেস্ট ডেটা অনুযায়ী এর লাভের হার এবং মুনাফার হার অত্যন্ত সন্তোষজনক। নির্দিষ্ট অপ্টিমাইজেশনের মাধ্যমে কৌশলটির স্থায়িত্ব এবং লাভজনকতা আরও উন্নত করার সম্ভাবনা রয়েছে।

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © myn

//@version=5

strategy('Strategy Myth-Busting #7 - MACDBB+SSL+VSF - [MYN]', max_bars_back=5000, overlay=true, pyramiding=0, initial_capital=1000, currency='USD', default_qty_type=strategy.percent_of_equity, default_qty_value=1.0, commission_value=0.075, use_bar_magnifier = false)

/////////////////////////////////////

//* Put your strategy logic below *//

/////////////////////////////////////

//nwVqTuPe6yo- 1