ডাবল মুভিং এভারেজ আরবিট্রেজ কৌশল

সংক্ষিপ্ত বিবরণ

এই কৌশলটি একটি ডাবল মুভিং এভারেজ প্যাটার্ন ব্যবহার করে আর্বিট্রেজ অপারেশন চালানোর জন্য ডিজাইন করা হয়েছে। এটি দুটি উপ-কৌশলকে একত্রিত করে: ১২৩ প্যাটার্ন রিভার্সাল এবং ফিনিট ভলিউম এলিমেন্ট (FVE)। যখন উভয়ই একইসাথে ক্রয় বা বিক্রয় সংকেত দেয়, তখন আর্টবিট্রেজ করা হয়।

কৌশলের নীতি

১২৩ প্যাটার্ন রিভার্সাল

এই উপ-কৌশলটি উলফ জেনসেনের বই "আমি ফিউচার্স বাজারে কীভাবে তিনগুণ লাভ করলাম" থেকে উদ্ভূত। এটি নিম্নলিখিত শর্তে সংকেত দেয়:

- যখন ক্লোজিং প্রাইস টানা ২ দিন বাড়ে এবং ৯ দিনের স্লো স্টোক্যাস্টিক সূচক ৫০-এর নিচে থাকে, তখন লং পজিশন নিন;

- যখন ক্লোজিং প্রাইস টানা ২ দিন কমে এবং ৯ দিনের ফাস্ট স্টোক্যাস্টিক সূচক ৫০-এর উপরে থাকে, তখন শর্ট পজিশন নিন।

ফিনিট ভলিউম এলিমেন্ট (FVE)

FVE একটি বিশুদ্ধ ভলিউম সূচক। এটি দামের ওঠানামার মাত্রা এবং ভলিউমের আকারের ভিত্তিতে অর্থের প্রবাহ বা বহির্গমন নির্ধারণ করে।

যখন সাম্প্রতিক দুটি বারের FVE সূচক একসাথে বাড়ে বা কমে, তখন এটি সংকেত দেয়।

সুবিধার বিশ্লেষণ

এই কৌশলটি বাজারের প্রবণতা এবং অর্থের প্রবাহ বিচার করতে দুটি সূচককে একত্রিত করে, যা ভুল সংকেত এড়াতে কার্যকর। এছাড়াও উভয় উপ-কৌশলেরই কিছু রিভার্সাল বৈশিষ্ট্য রয়েছে, তাই লাভের জন্য আর্টবিট্রেজ করা সম্ভব।

অধিকন্তু, যখন ডাবল মুভিং এভারেজ প্যাটার্ন দেখা দেয়, তখন এটি স্বল্পমেয়াদী এবং মধ্যমেয়াদী প্রবণতার সামঞ্জস্য নির্দেশ করে, তাই এটি বেশ শক্তিশালী।

ঝুঁকির বিশ্লেষণ

এই কৌশলটি মুভিং এভারেজ প্যাটার্নের উপর নির্ভরশীল। বাজারে যখন অস্থিরতা থাকে, তখন ভুল সংকেতের কারণে লোকসান হতে পারে। তাছাড়া, রিভার্সাল ব্যর্থ হওয়াও একটি সাধারণ ঝুঁকি।

পরামিতি যথাযথভাবে সামঞ্জস্য করে কৌশলটিকে আরও শক্তিশালী করা যায়, অথবা ঝুঁকি নিয়ন্ত্রণের জন্য স্টপ-লস সেট করা যেতে পারে।

অপটিমাইজেশনের দিকনির্দেশনা

সর্বোত্তম মিল খুঁজে পেতে বিভিন্ন ধরনের মুভিং এভারেজ সূচক পরীক্ষা করা যেতে পারে। ভুল সংকেত এড়াতে আরএসআই বা অস্থিরতা সূচকের মতো অন্যান্য সহায়ক সূচকও যুক্ত করা যেতে পারে।

এছাড়া, বাজারের অবস্থার ভিত্তিতে প্যারামিটার গতিশীলভাবে সামঞ্জস্য করার উপায় নিয়ে গবেষণা করা যেতে পারে, যাতে কৌশলটি আরও অভিযোজিত হয়। প্যারামিটার স্ব-অভিযোজনের জন্য মেশিন লার্নিং এবং নিউরাল নেটওয়ার্ক অ্যালগরিদমও অন্বেষণ করা যেতে পারে।

সারসংক্ষেপ

এই ডাবল মুভিং এভারেজ আর্বিট্রেজ কৌশল দুটি রিভার্সাল-ভিত্তিক সূচককে একত্রিত করে সিদ্ধান্ত নেয়, যা কিছুটা ঝুঁকি এড়াতে পারে। তবে মুভিং এভারেজ প্যাটার্নের উপর নির্ভরশীল হওয়ায় কৌশলটিকে আরও শক্তিশালী করতে আরও অপটিমাইজেশন প্রয়োজন। সামগ্রিকভাবে, এই কৌশলটি স্বল্পমেয়াদী আর্টবিট্রেজ ট্রেডিংয়ের জন্য একটি মৌলিক কাঠামো সরবরাহ করে, যা আরও গবেষণার যোগ্য।

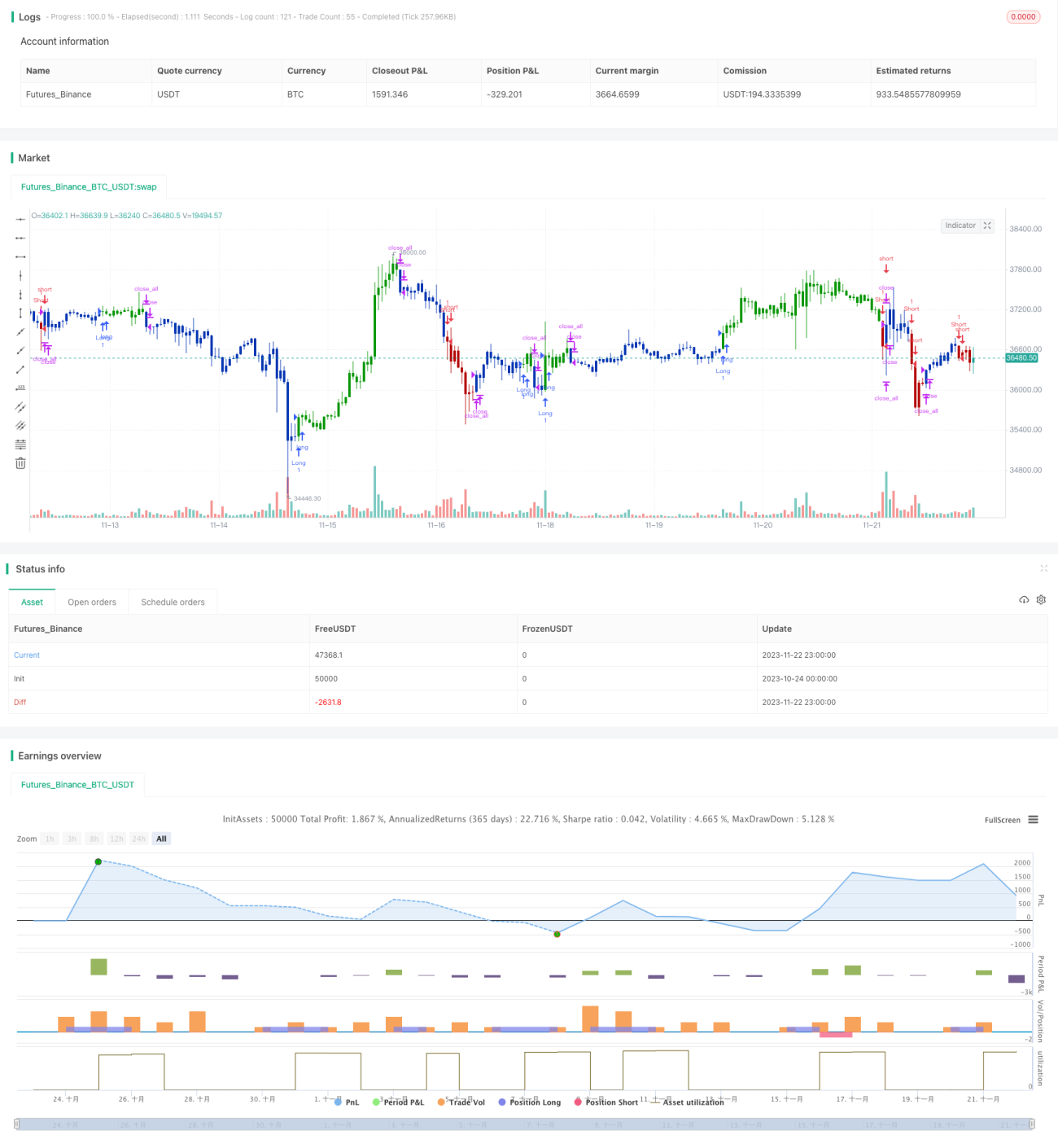

/*backtest

start: 2023-10-24 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 25/08/2020

// This is combo strategies for get a cumulative signal. - 1