EMA মুভিং এভারেজ-ভিত্তিক ট্রেডিং কৌশল

সারসংক্ষেপ

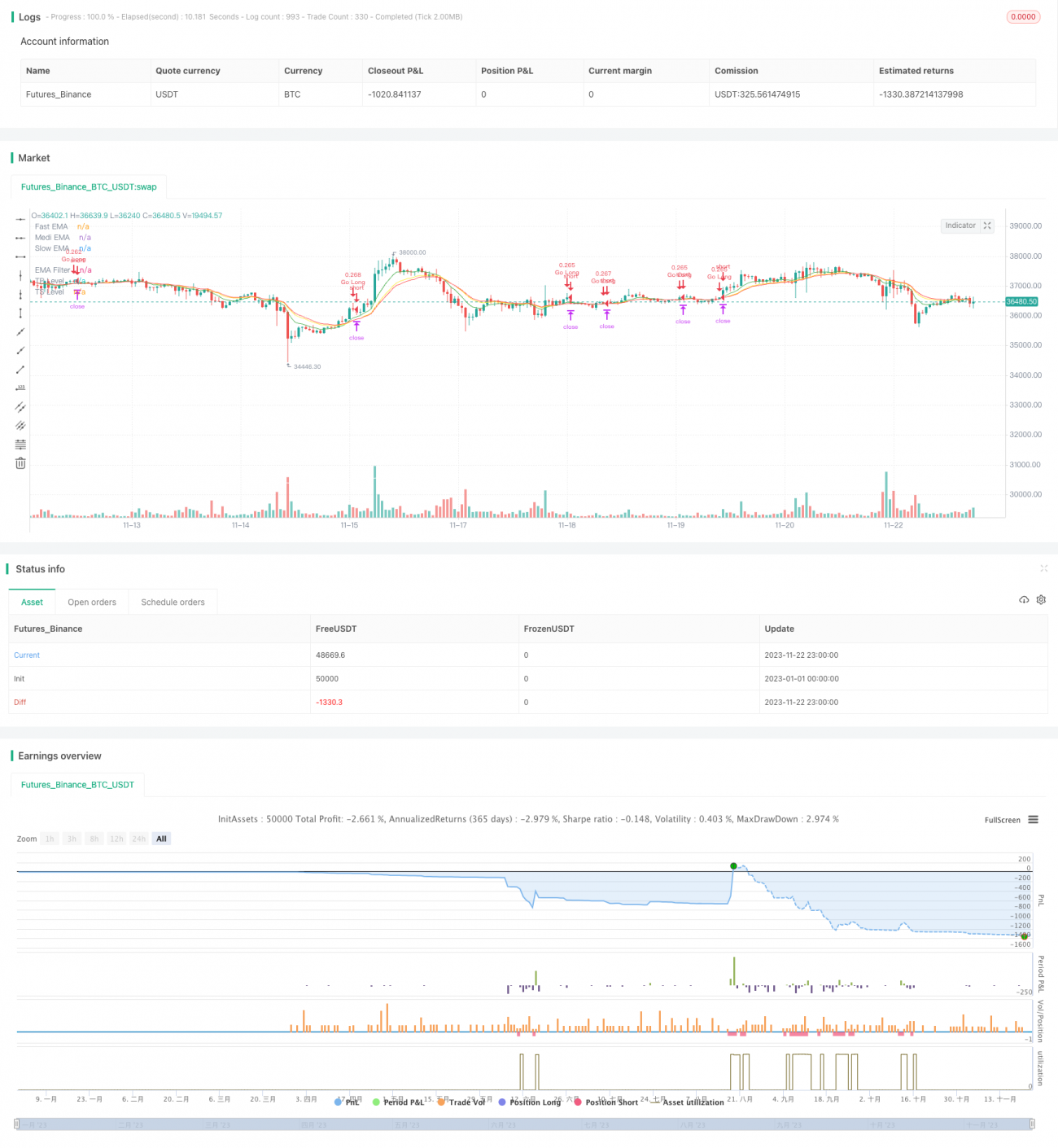

এই কৌশলটি ৪টি ভিন্ন সময়কালের EMA মূভিং এভারেজ ব্যবহার করে, তাদের বিন্যাসের ক্রম অনুসারে ট্রেডিং সিগন্যাল তৈরি করে, যা ট্রাফিক লাইটের লাল, হলুদ ও সবুজ আলোর মতো, তাই নামকরণ করা হয়েছে 'ট্রাফিক লাইট ট্রেডিং স্ট্র্যাটেজি'। এটি ট্রেন্ড ও রিভার্সাল উভয় দৃষ্টিকোণ থেকে বাজার বিশ্লেষণ করে, যাতে ট্রেডিং সিদ্ধান্তের নির্ভুলতা বৃদ্ধি পায়।

কৌশল নীতি

১. দ্রুত লাইন (৮ পিরিয়ড), মধ্যম লাইন (১৪ পিরিয়ড), ধীর লাইন (১৬ পিরিয়ড) — এই ৩টি EMA মূভিং এভারেজ সেট করা হয়, এবং একটি দীর্ঘ সময়কালের (১০০ পিরিয়ড) EMA মূভিং এভারেজ ফিল্টার হিসেবে অন্তর্ভুক্ত করা হয়।

২. দ্রুত, মধ্যম ও ধীর লাইনের বিন্যাস ক্রম এবং ফিল্টারের সাথে ক্রসওভার পর্যবেক্ষণ করে লং ও শর্ট করার সময় নির্ধারণ করা হয়:

-

দ্রুত লাইন মধ্যম লাইনকে উপরে ক্রস করলে বা মধ্যম লাইন ধীর লাইনকে উপরে ক্রস করলে লং সিগন্যাল ধরা হয়।

-

মধ্যম লাইন দ্রুত লাইনকে নিচে ক্রস করলে লং ক্লোজ করার সিগন্যাল ধরা হয়।

-

দ্রুত লাইন মধ্যম লাইনকে নিচে ক্রস করলে বা মধ্যম লাইন ধীর লাইনকে নিচে ক্রস করলে শর্ট সিগন্যাল ধরা হয়।

-

মধ্যম লাইন দ্রুত লাইনকে উপরে ক্রস করলে শর্ট ক্লোজ করার সিগন্যাল ধরা হয়।

৩. দ্রুত, মধ্যম ও ধীর লাইনের ক্রম অনুযায়ী ট্রেন্ডের দিক ও শক্তি নির্ধারণ করা হয় এবং মূভিং এভারেজের সাথে ফিল্টারের ক্রসওভার পর্যবেক্ষণ করে রিভার্সাল পয়েন্ট চিহ্নিত করা হয়। এর মাধ্যমে ট্রেন্ড ফলোয়িং ও রিভার্সাল ক্যাপচারের কার্যকর সমন্বয় সাধিত হয়।

সুবিধা বিশ্লেষণ

এই কৌশলটি ট্রেন্ড ফলোয়িং ও রিভার্সাল ট্রেডিংয়ের সুবিধাগুলো একত্রিত করে, যা বাজারের সুযোগগুলো সঠিকভাবে কাজে লাগাতে সহায়তা করে। প্রধান সুবিধাগুলো হলো:

১. একাধিক EMA মূভিং এভারেজ ব্যবহারের ফলে বিচারক্ষমতা শক্তিশালী হয় এবং ভুয়া সিগন্যাল কমে যায়।

২. লং ও শর্ট করার শর্ত নমনীয়ভাবে নির্ধারণ করা যায়, ফলে ট্রেডিং সুযোগ হাতছাড়া হওয়ার সম্ভাবনা কমে।

৩. স্বল্প ও দীর্ঘ সময়কালের মূভিং এভারেজের ত্রিমাত্রিক ব্যবহারের মাধ্যমে বিস্তৃত বিচারক্ষমতা অর্জিত হয়।

৪. কাস্টমাইজড টেক প্রফিট ও স্টপ লস শর্ত নির্ধারণ করা যায়, যা ঝুঁকি নিয়ন্ত্রণে কার্যকর।

প্যারামিটার অপ্টিমাইজেশনের মাধ্যমে এই কৌশলটি আরও বেশি পণ্যের সাথে খাপ খাইয়ে নিতে পারে এবং ব্যাকটেস্টিং এ শক্তিশালী লাভজনকতা ও স্থিতিশীলতা প্রদর্শন করে।

ঝুঁকি বিশ্লেষণ

এই কৌশলের প্রধান ঝুঁকিগুলো হলো:

১. একাধিক EMA মূভিং এভারেজের বিন্যাস ক্রম বিশৃঙ্খল হলে সিদ্ধান্ত নেওয়া কঠিন হয়ে পড়ে এবং ট্রেডিংয়ে দ্বিধা সৃষ্টি হতে পারে।

২. বাজারের অস্বাভাবিক ওঠানামার ভুয়া সিগন্যাল কার্যকরভাবে ফিল্টার করা সম্ভব হয় না, যেমন বড় ধরনের দোলাচলে ক্ষতি হতে পারে।

৩. প্যারামিটার সঠিকভাবে নির্ধারণ না করলে টেক প্রফিট ও স্টপ লস শর্ত অতিরিক্ত শিথিল বা কঠোর হয়ে যেতে পারে, যার ফলে লাভ হাতছাড়া হতে পারে বা অতিরিক্ত ক্ষতি হতে পারে।

প্যারামিটার অপ্টিমাইজেশন, স্টপ লস স্তর নির্ধারণ ও সতর্কতামূলক ট্রেডিংয়ের মাধ্যমে কৌশলটির স্থিতিশীলতা ও ঝুঁকি নিয়ন্ত্রণ আরও উন্নত করার পরামর্শ দেওয়া হচ্ছে।

অপ্টিমাইজেশন দিকনির্দেশনা

এই কৌশলের প্রধান অপ্টিমাইজেশন দিকনির্দেশনাগুলো হলো:

১. EMA মূভিং এভারেজের সময়কালের প্যারামিটার সমন্বয় করে আরও বেশি পণ্যের সাথে খাপ খাইয়ে নেওয়া।

২. আরও নির্ভুল বিচারের জন্য MACD, বোলিঞ্জার ব্যান্ড ইত্যাদির মতো অন্যান্য ইন্ডিকেটর যুক্ত করা।

৩. টেক প্রফিট ও স্টপ লসের অনুপাত অপ্টিমাইজ করে ঝুঁকি ও লাভের মধ্যে সর্বোত্তম ভারসাম্য অর্জন করা।

৪. নিচের দিকের ঝুঁকি আরও নিয়ন্ত্রণের জন্য ATR স্টপ লসের মতো অভিযোজিত স্টপ লস ব্যবস্থা যুক্ত করা।

বহুমুখী প্যারামিটার সমন্বয় ও ঝুঁকি নিয়ন্ত্রণ ব্যবস্থা অন্তর্ভুক্তির মাধ্যমে কৌশলটির স্থিতিশীলতা ও লাভজনকতা ক্রমাগত উন্নত করা যেতে পারে।

উপসংহার

এই ট্রাফিক লাইট ট্রেডিং কৌশলটি ট্রেন্ড ফলোয়িং ও রিভার্সাল বিচারকে একীভূত করে এবং ৪টি EMA মূভিং এভারেজের মাধ্যমে ট্রেডিং সিগন্যাল তৈরি করে। প্যারামিটার অপ্টিমাইজেশনের মাধ্যমে এটি আরও বেশি পণ্যের সাথে খাপ খাইয়ে নেয় এবং ব্যাকটেস্টিং এ শক্তিশালী লাভজনকতা প্রদর্শন করে। পরবর্তীতে আরও ঝুঁকি নিয়ন্ত্রণ ও বহুমুখী ইন্ডিকেটর অন্তর্ভুক্তির মাধ্যমে এটি একটি স্থিতিশীল ও দক্ষ কোয়ান্টিটেটিভ ট্রেডিং কৌশলে পরিণত হওয়ার সম্ভাবনা রাখে।

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © maxits

// 4HS Crypto Market Strategy- 1