স্তরভিত্তিক লাভ গ্রহণ স্লিপেজ কৌশল

সারসংক্ষেপ

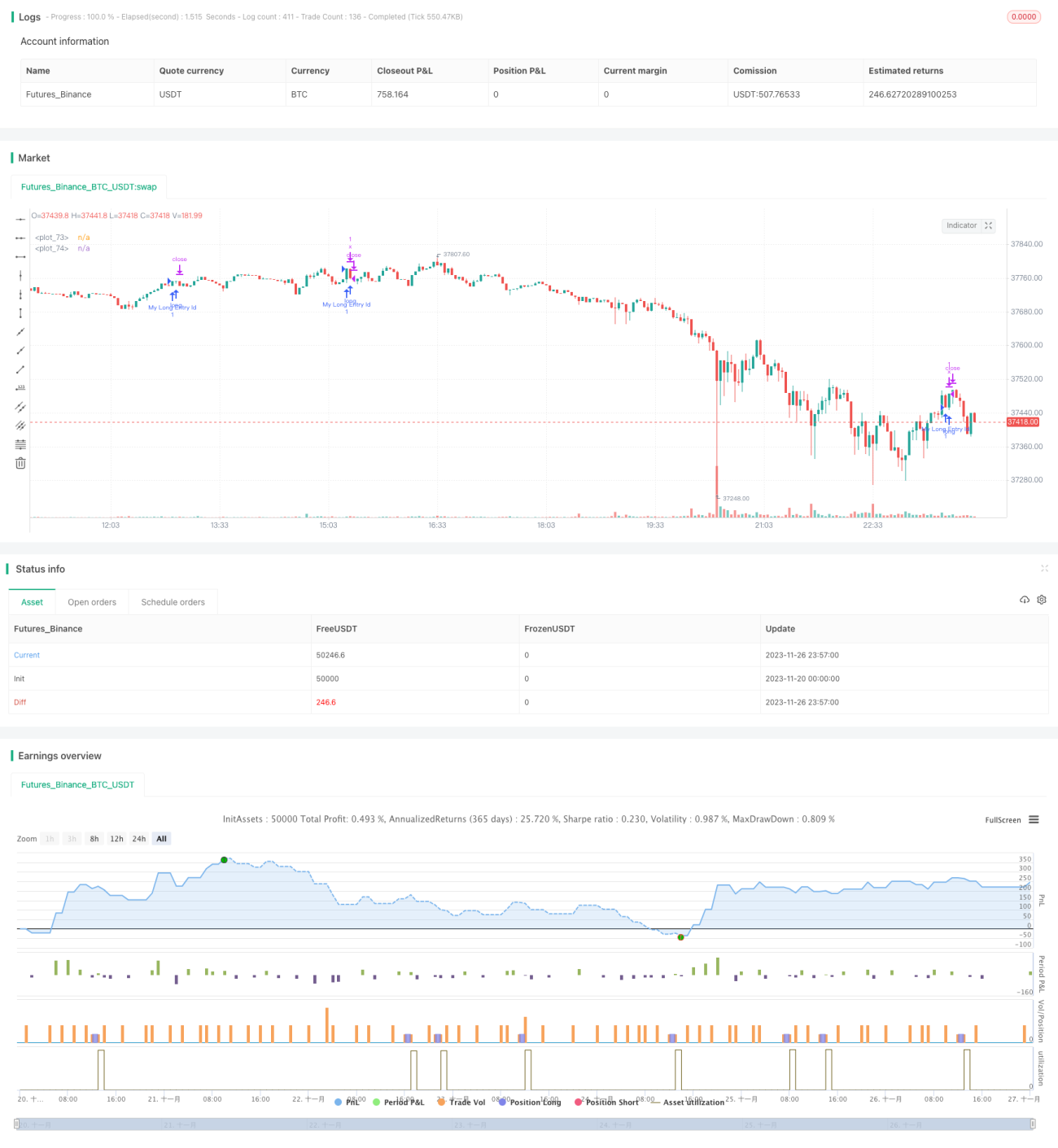

এই কৌশলটি একটি ধাপে ধাপে লাভ লক (stepwise profit-taking) এবং স্লিপেজ স্টপ লস (slippage stop-loss) একত্রিত একটি এক্সিট কৌশল। এটি প্রথম লাভের পয়েন্টে পৌঁছানোর পর স্টপ লসকে ব্রেকইভেন পয়েন্টে সরিয়ে নেয় এবং দ্বিতীয় লাভের পয়েন্টে পৌঁছানোর পর স্টপ লসকে প্রথম লাভের পয়েন্টে সরিয়ে নেয়, ফলে একটি ধাপে ধাপে স্টপ লস স্লিপেজ মেকানিজম তৈরি হয়। এটি আংশিক মুনাফা লক করার পাশাপাশি বড় মুনাফার জায়গা ধরে রাখতে সাহায্য করে।

কৌশলের মূলনীতি

এই কৌশলটি মূলত নিচের অংশগুলোর মাধ্যমে ধাপে ধাপে লাভ লক এবং স্লিপেজ বাস্তবায়ন করে:

- স্টপ লস পয়েন্ট এবং ৩টি লাভের পয়েন্ট নির্ধারণ।

- বর্তমান লাভের পয়েন্ট সংখ্যা এবং স্টপ লস মূল্য গণনার ফাংশন সংজ্ঞায়িত করা।

- লাভের পর্যায় নির্ধারণের ফাংশন সংজ্ঞায়িত করা।

- বিভিন্ন লাভের পর্যায়ে স্টপ লস মূল্য পরিবর্তন করে স্লিপেজ স্টপ লস বাস্তবায়ন।

নির্দিষ্টভাবে, এটি প্রথমে ১০০ পয়েন্টের স্টপ লস দূরত্ব এবং ১০০/২০০/৩০০ পয়েন্টের ৩টি লাভের দূরত্ব নির্ধারণ করে। তারপর বর্তমান মূল্য এবং খোলা মূল্যের ভিত্তিতে লাভের পয়েন্ট সংখ্যা গণনার ফাংশন curProfitInPts এবং পয়েন্ট দূরত্বের ভিত্তিতে স্টপ লস মূল্য গণনার ফাংশন calcStopLossPrice সংজ্ঞায়িত করে।

মূল লজিকটি getCurrentStage ফাংশনে, যা বর্তমানে পজিশন আছে কিনা এবং লাভের পয়েন্ট সংখ্যা কোনো লাভের পয়েন্ট অতিক্রম করেছে কিনা তা পরীক্ষা করে, অতিক্রম করলে পরবর্তী পর্যায়ে চলে যায়। উদাহরণস্বরূপ, ১০০ পয়েন্ট লাভের পর দ্বিতীয় পর্যায়ে, ২০০ পয়েন্ট লাভের পর তৃতীয় পর্যায়ে চলে যায়।

অবশেষে, পর্যায় অনুযায়ী স্টপ লস মূল্য পরিবর্তন করে স্লিপেজ স্টপ লস বাস্তবায়ন করা হয়। প্রথম পর্যায়ে স্টপ লস আসল সেটিংয়ে থাকে, দ্বিতীয় পর্যায়ে ব্রেকইভেনে সরানো হয়, তৃতীয় পর্যায়ে প্রথম লাভের পয়েন্টে সরানো হয়।

সুবিধা বিশ্লেষণ

এই ধাপে ধাপে লাভ লক এবং স্লিপেজ কৌশলের নিম্নলিখিত সুবিধাগুলো রয়েছে:

- আংশিক মুনাফা লক করার পাশাপাশি পরবর্তীতে বড় মুনাফার জায়গা ধরে রাখা যায়।

- স্লিপেজ স্টপ লস ব্যবহার করে মূল্য ট্র্যাক করা যায়, যা ড্রডাউন বা ক্ষতির সম্ভাবনা কমায়।

- একবারে একক লাভ লকের পরিবর্তে ধাপে ধাপে লাভ লক করায় ঝুঁকি নিয়ন্ত্রণ ভালো হয়।

- কৌশলটির লজিক সহজ ও বোধগম্য।

ঝুঁকি বিশ্লেষণ

এই কৌশলের কিছু ঝুঁকিও রয়েছে:

- ধাপে ধাপে লাভ লক করার ফলে সময়মতো লাভ লক না হওয়ার সম্ভাবনা থাকে, ভালো এক্সিট পয়েন্ট মিস হতে পারে। লাভের পয়েন্ট সংখ্যা সমন্বয় করে অপ্টিমাইজ করা যেতে পারে।

- স্লিপেজের পরিমাণ খুব বেশি হলে স্টপ লস অকালে ট্রিগার হতে পারে। বিভিন্ন স্লিপেজ পরিমাণ পরীক্ষা করা উচিত।

- স্টপ লস কাজ না করলে বড় ক্ষতির ঝুঁকি থাকে। নির্দিষ্ট পরিস্থিতিতে দ্রুত স্টপ লসের ব্যবস্থা বিবেচনা করা যেতে পারে।

অপ্টিমাইজেশনের দিকনির্দেশনা

কৌশলটিকে নিম্নলিখিত দিক থেকে অপ্টিমাইজ করা যেতে পারে:

- বিভিন্ন লাভ ও স্টপ লস দূরত্ব পরীক্ষা করে প্যারামিটার অপ্টিমাইজ করা।

- বিশেষ পরিস্থিতিতে দ্রুত স্টপ লস মেকানিজম বিবেচনা করা।

- টেকনিক্যাল ইন্ডিকেটরের সাথে মিলিয়ে লাভ ও স্টপ লস পয়েন্ট নির্ধারণ করা।

- স্লিপেজের পরিমাণ অপ্টিমাইজ করে লাভ ও স্টপ লসের মধ্যে ভারসাম্য আনা।

- 1